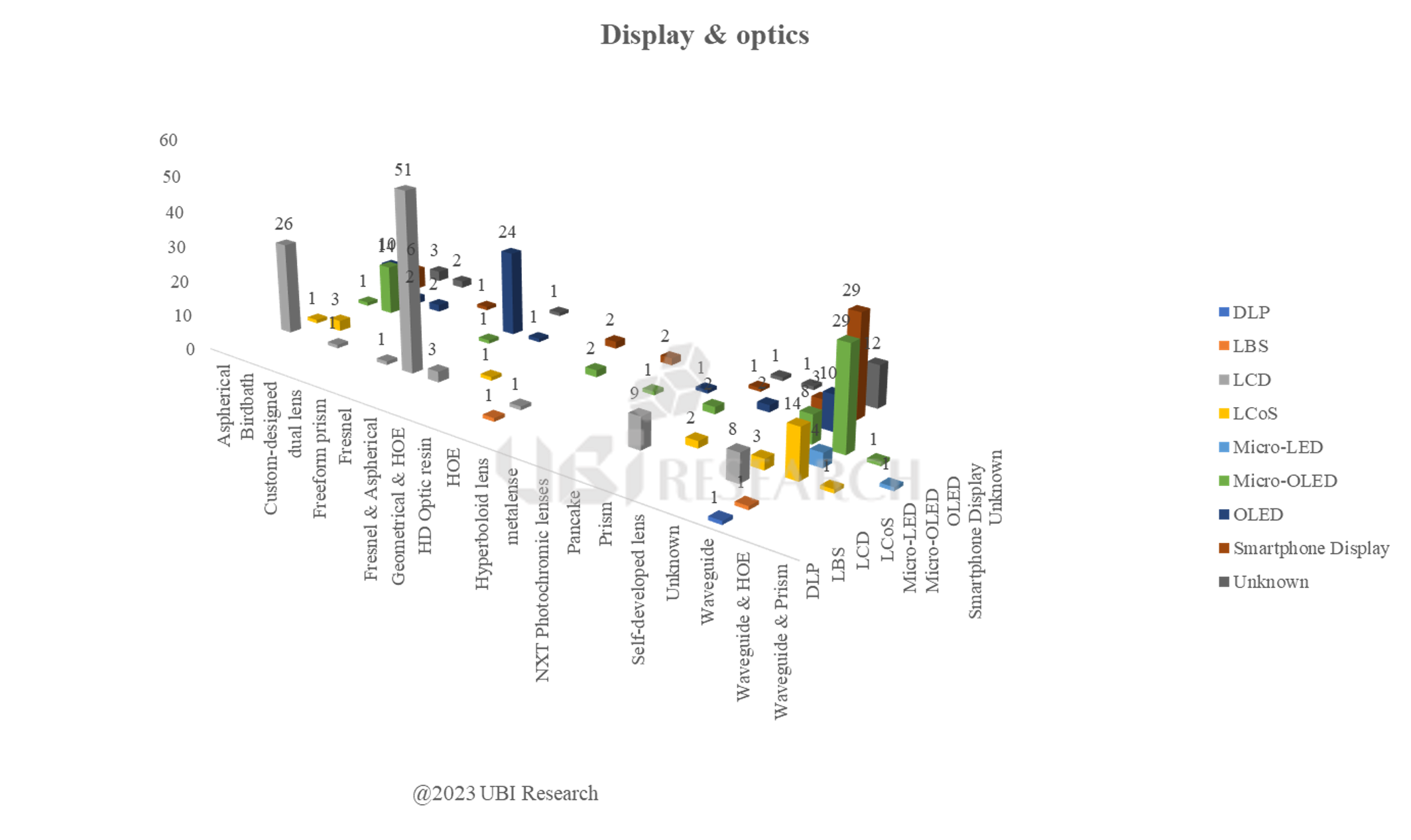

XR Headset Shipments Set to Top 10 Million in 2025… AR Expansion Drives OLEDoS Growth

UBI Research forecast trend for XR device (MR/VR and AR) shipments equipped with OLEDoS from 2025 to 2031 (Source: UBI Research)

The rapid expansion of the AI and XR device market has intensified competition in next-generation microdisplay technologies. According to a new report published by UBI Research titled ” XR Industry Trends and OLEDoS Display Technology & Industry Analysis” XR headset shipments are expected to exceed 10 million units by 2025. Notably, AR smart glasses alone saw over a 50% year-on-year increase in the first half of this year, clearly shifting the market’s center of gravity.

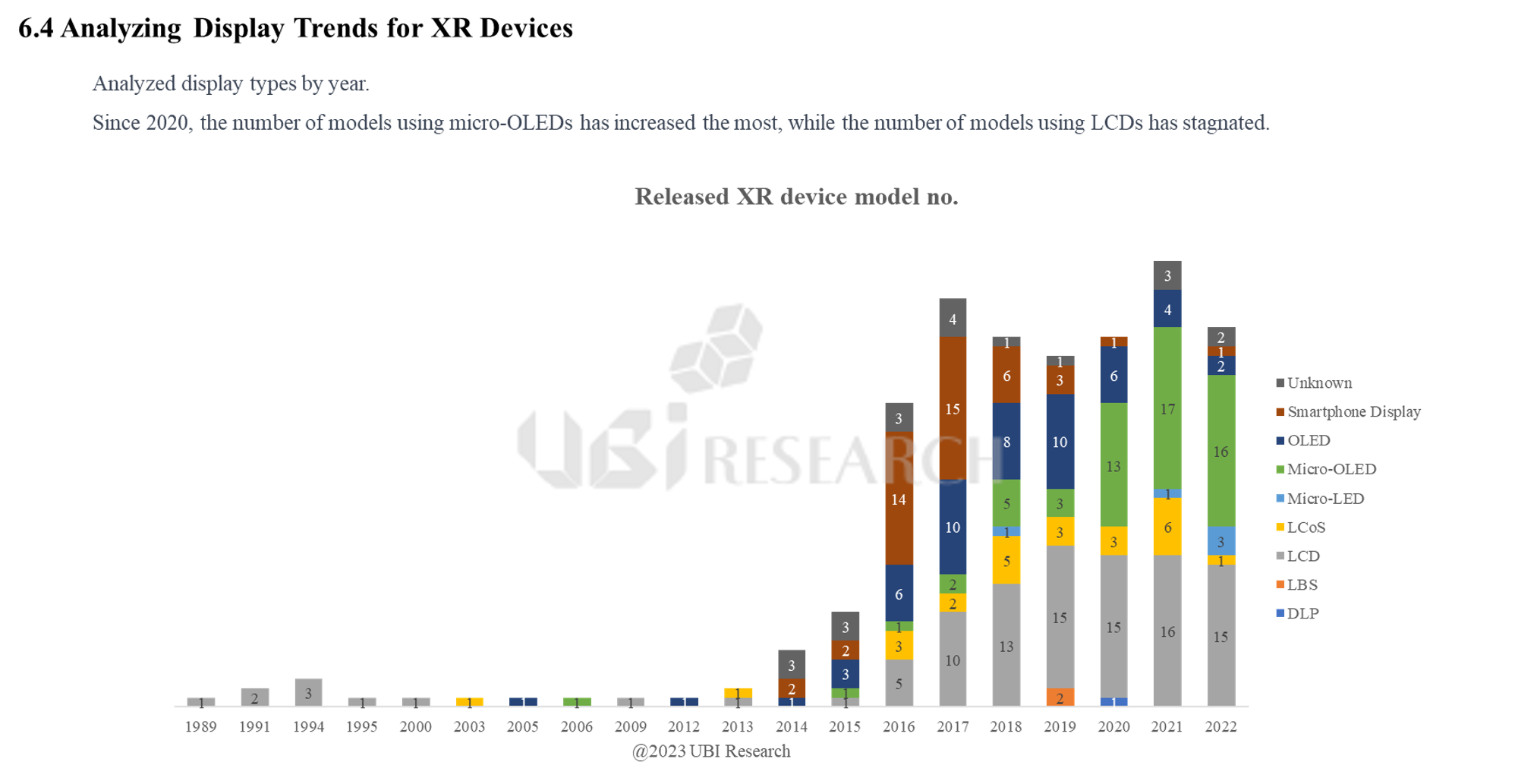

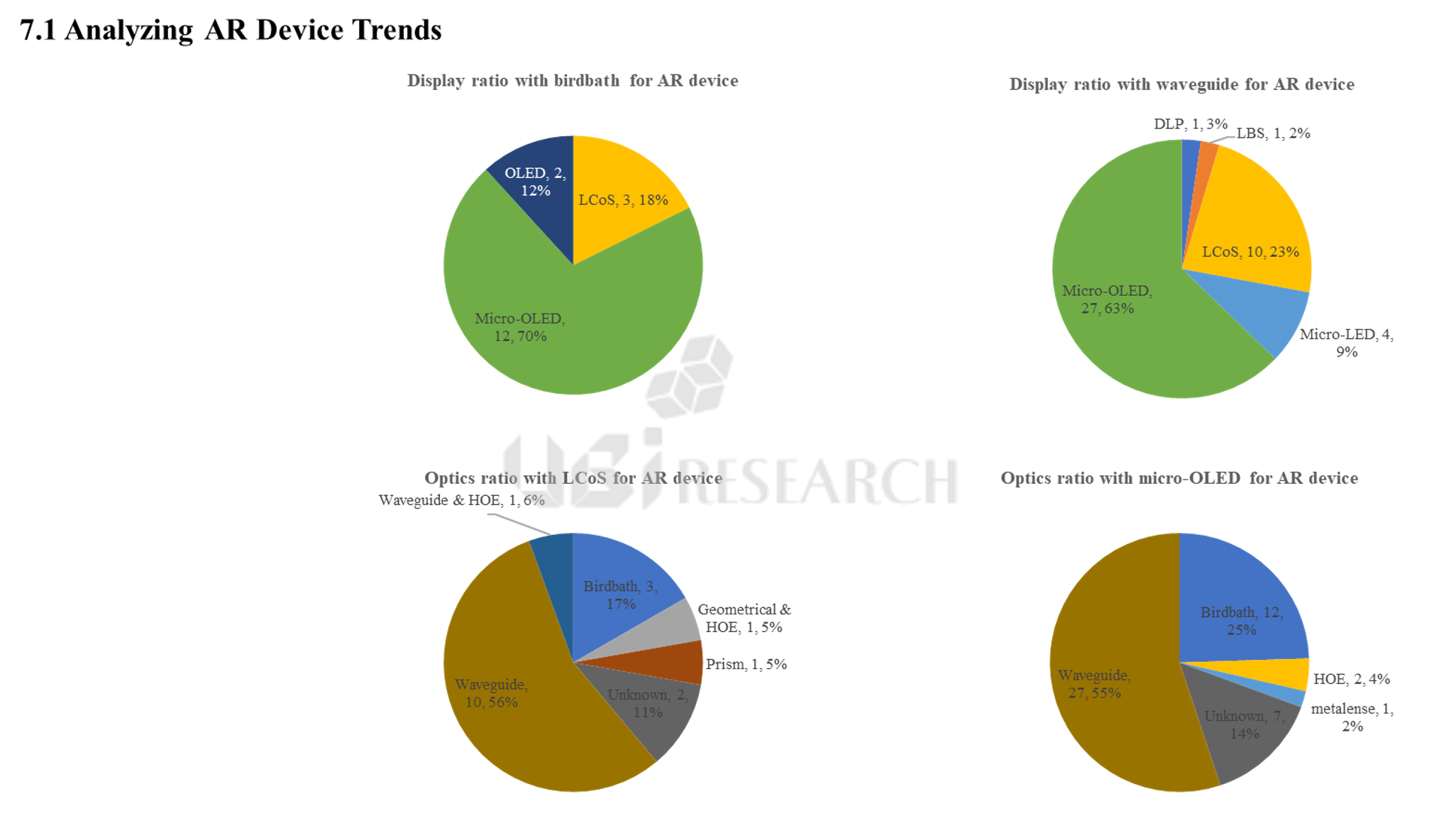

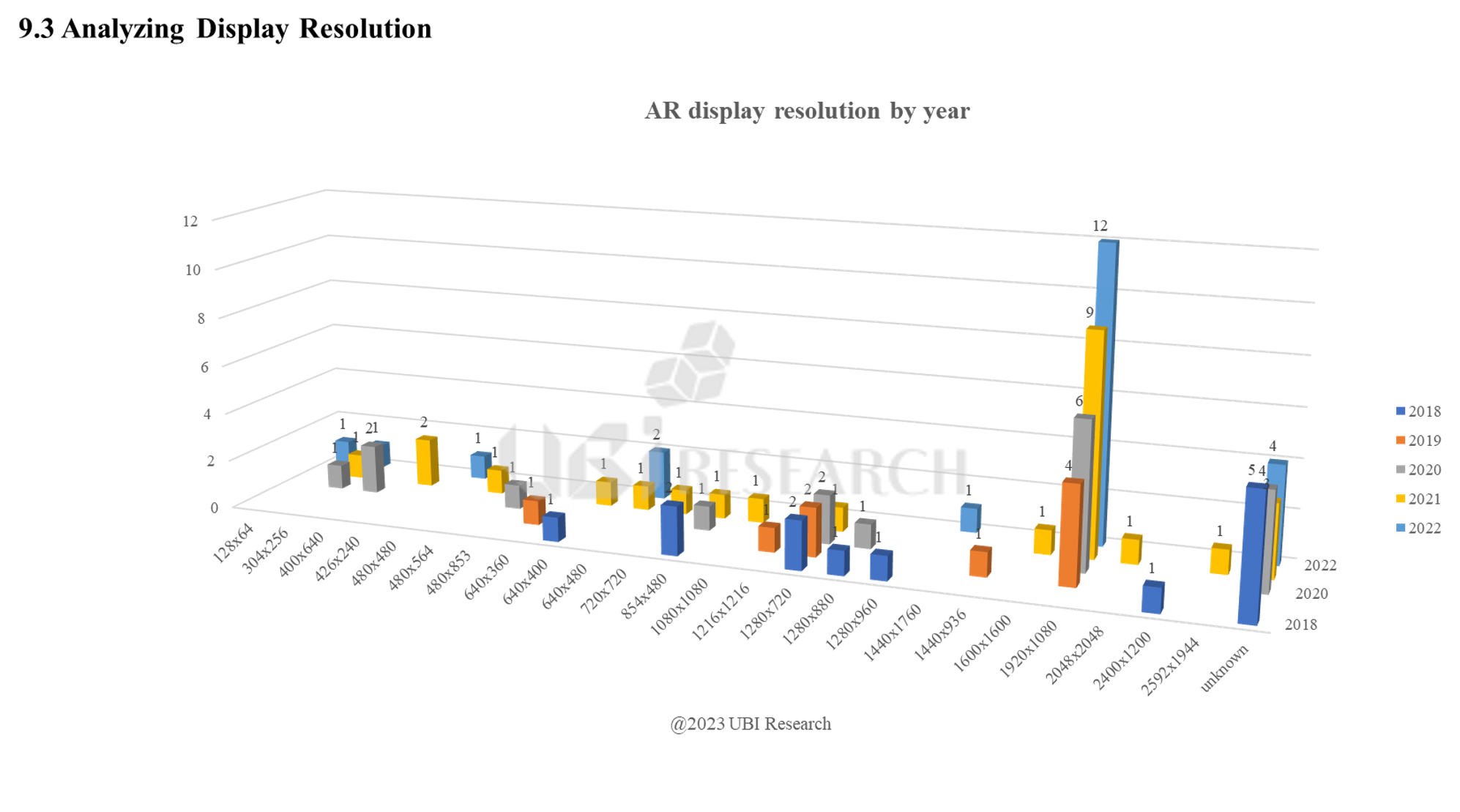

The AR market is diversifying, expanding its application range from AI glasses focused on information display to business-use AR glasses and content-viewing devices. In the consumer AI glasses market, primarily focused on information display, monochrome displays with resolutions around 640 x 480 (VGA) and microdisplays under 0.3 inches are commonly used, with LCoS and micro LED competing for position. Workplace AR glasses require resolutions of 1280×720 (HD) or higher, while content-viewing AR demands resolutions of 1920×1080 (FHD) or higher. As industry’s expansion focus shifts from VR to AR, the demand for simultaneously meeting ultra-high resolution, high brightness, and lightweight requirements has grown significantly. Consequently, OLEDoS is evaluated as the fastest-growing display technology within the XR ecosystem.

Global manufacturers are also accelerating OLEDoS development and supply chain expansion. Samsung Display joined the OLEDoS market, previously led by Sony, BOE, and Seeya, by supplying OLEDoS panels for Samsung Electronics’ Galaxy XR, released in October 2025, following Sony. In China, companies like BOE, Seeya, and SIDTEK have commenced mass production of 12-inch OLEDoS panels, marking the most notable shift in the supply chain. Chinese firms are strengthening their in-house capabilities in core processes such as high-resolution patterning, Si-backplane design, and tandem OLED structures, suggesting their global supply share will rapidly expand in the future.

UBI Research analyst Changho Noh predicted, “The OLEDoS market is projected to grow from approximately $285 million in 2025 to $840 million by 2031, driven by supply chain expansion and diverse demand bases.”

He further analyzed, “Shipments of OLEDoS-equipped XR devices are expected to increase from 1.2 million units in 2025 to 8.86 million units by 2031, with AR devices anticipated to account for approximately 90% of total OLEDoS shipments by 2031.”

Changho Noh, Senior Analyst at UBI Research (chnoh@ubiresearch.com)

XR Industry Trends and OLEDoS Display Technology & Industry Analysis Report

XR Industry Trends and OLEDoS Display Technology & Industry Analysis Report

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.