Samsung Display to Showcase AI-Era OLED at ‘CES 2026’

□ Proposing AI-Display convergence lifestyle with futuristic devices like ‘AI OLED Bot’

□ High-definition OLED for offices and homes… Infinite expansion of IT OLED in the AI era

□ “Thought it was a dashboard”… Imagined luxury car interiors realized with Samsung OLED

□ Bouncing basketballs on foldable panels and freezing them… Samsung OLED durability is fundamental

□ Wristwatch size, 3x pixels of 4K TV… Experience RGB OLEDoS image quality right before your eyes

Samsung Display will unveil a wide range of next-generation OLED products designed to multiply AI experiences at ‘CES 2026’. In a lifestyle exhibition where visitors can experience not only existing electronic devices but also new concept products never seen before, they can imagine AI enriched further by convergence with OLED.

Samsung Display announced on the 4th that it will hold an exhibition for customers under the theme ‘A New Era of Experience, Powered by AI & Display’ at ‘CES 2026’, held in Las Vegas, USA, from the 6th to the 9th (local time).

At this exhibition, Samsung Display will showcase various OLED concept products, such as the ‘AI OLED Bot’, which can serve as a platform for communication between humans and AI. The company will also present a blueprint for how Samsung’s OLED technology, embedded in various IT devices like tablets, laptops, and monitors, can create synergy with AI in everyday life.

In addition, Samsung Display plans to introduce various new solutions that can enhance the luxury of vehicle interiors based on OLED’s high design freedom, or Free-Form characteristics. The company has also prepared various attractions to verify the unrivaled durability of Samsung OLED, such as a robot shooting hoops at a basketball backboard attached with 18 foldable panels or displaying a display inside a refrigerator.

□ ‘OLED Face’ AI Robot Guides Classrooms… “AI Agents to Become More Powerful with OLED”

Samsung Display will exhibit various concept products, ‘Edge Devices’, which have not been disclosed until now, in the ‘AI Edge Vision Station’ space, introducing an AI lifestyle that is further amplified when OLED is integrated into AI devices.

The ‘AI OLED Bot’, equipped with a 13.4-inch OLED in place of a face, was developed as a small robot concept capable of freely moving around designated spaces and communicating with users based on AI. In this exhibition, it will be introduced as a robot teaching assistant supporting students at universities, guiding classroom locations, or providing information such as professor profiles. Since it is equipped with a display, students can easily inquire about assignment details or class cancellation plans and check answers even in class environments where voice commands and speaker usage are difficult. The advantage is that unlike LCDs, OLEDs can be freely designed in curved, spherical, or circular shapes, allowing manufacturers’ intentions or consumers’ tastes to be reflected in various ways, like a robot face.

Several speaker concept products capable of acting as assistants, such as AI-based music recommendations, will also be showcased. While existing Bluetooth speakers were used by connecting to separate smart devices, the exhibited speaker-type demo products allow users to receive music recommendations or make selections directly on the device while watching the display, and even create interior effects through images and videos. Among them, the ‘AI OLED Mood Lamp’, equipped with a 13.4-inch circular OLED, can create lighting with different atmospheres depending on the playing music, while the ‘AI OLED Cassette (1.5-inch circular OLED)’ and ‘AI OLED Turntable (13.4-inch circular OLED)’ embody analog sentiment in their appearance.

□ Office, Business Trip, Travel, Home ‘All OLED’… “Over 300 IT Products with Samsung OLED & QD-OLED”

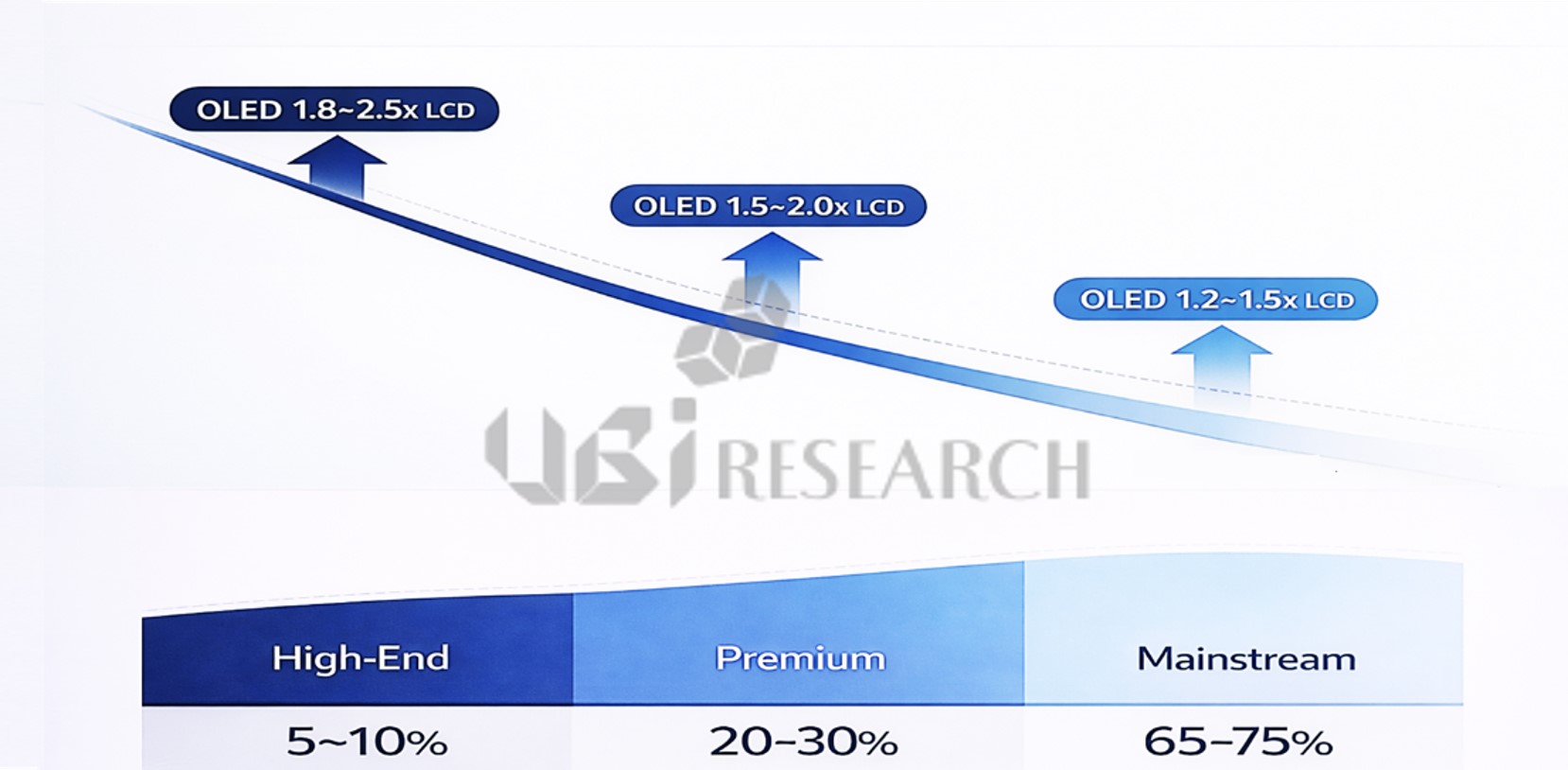

Samsung Display also provides opportunities to experience scenarios according to usage environments such as offices, business trip locations, and homes, demonstrating how OLED elevates the utility of AI. This setup emphasizes the recent ‘mainstream’ trend where OLED adoption is increasing across various consumers and all product groups.

In the exhibition space decorated with the theme of an architecture firm, visitors can verify Samsung OLED’s excellent color reproduction, dark area expression, brightness, and viewing angle strengths. In a digital design environment utilizing AI, employees share various blueprints, material drafts, and colors on the screen; here, OLED is the optimal display that reflects and delivers the designer’s conception and design without distortion.

Samsung Display also offers the optimal solution for AI laptops with light and slim designs that will increase work efficiency on business trips. The ‘UT One’ technology is a prime example. Unlike existing products that use two glass substrates, OLED with an ‘Ultra Thin (UT)’ structure applies a glass substrate at the bottom and an organic/inorganic thin film at the top, making it 30% thinner and 30% lighter. Furthermore, applying Oxide TFT technology allows flexible switching of refresh rates from 1Hz to 120Hz depending on the usage environment, effectively reducing power consumption and securing extra power for AI. In terms of image quality, UT One expresses deeper blacks as there is no air layer between glass substrates, satisfying 100% of both the DCI-P3 color gamut used in the film and game industries and the Adobe RGB color gamut, the standard for printing, photography, and professional output.

For the home, the company proposes scenarios where monitors and TVs act as AI hubs. QD-OLED monitors function as wall clocks or art frames through low-power technology-based AoD (Always On Display) functions, then support AI operations such as showing user health information or briefing today’s schedule in specific situations. QD-OLED, which boasts excellent color reproduction and wide viewing angles, has the strength of providing optimal image quality regardless of viewing position.

The ’26 model TV QD-OLED, unveiled for the first time at this exhibition, supports 4,500 nits brightness, a first for self-emissive displays, based on organic material optimization. QD-OLED, which configures peak brightness by combining the brightness of each RGB, has higher color reproduction and perceived brightness compared to competing products of the same luminance, enabling further enhancement of image quality improvement technologies utilizing AI.

A Samsung Display representative explained, “Samsung OLED and QD-OLED are being widely adopted not only for gamers and experts but also for general office and home use, proving to be the optimized technology for the AI era,” adding, “Actually, the number of tablet, laptop, and monitor products launched last year equipped with Samsung Display panels exceeded 300, a more than threefold increase compared to three years ago.”

□ “Thought it was a dashboard, but it’s a display”… Imagined Vehicle Interiors Completed with Samsung OLED

The newly designed ‘Digital Cockpit’ demo product offers a time to imagine future autonomous vehicles armed with advanced displays of various designs and form factors.

In the center fascia between the driver and passenger seats, the CID (Center Information Display) ‘Flexible L’ with a design that naturally connects to the front dashboard is exhibited. The screen size has increased to 18.1 inches compared to the 14.4 inches shown in previous exhibitions, enhancing aesthetic and functional completeness. The Flexible L, which bends flexibly in an alphabet ‘L’ shape, not only accentuates the vehicle interior but also supports intuitive operation of functions frequently used by drivers, such as the climate control system.

The 13.8-inch PID (Passenger Information Display) is a product designed for the passenger to enjoy content; it is a solution that can be hidden under the dashboard when the driver is alone, expanding the vehicle’s internal space and enhancing interior aesthetics. In addition, products that increase interior luxury, such as a curved cluster realizing 500R curvature despite being a Rigid OLED using a hard glass substrate, and a 30-inch RSE (Rear Seat Entertainment) with a 32:9 wide aspect ratio mounted on the rear seat ceiling, are exhibited in large numbers.

The OLED Tail Lamp, designed by combining a 34-inch wide display and an 8-inch display, is the highlight of the new digital cockpit design. Based on the strength of OLED, which has excellent visibility even under sunlight (external light), it can convey visual information related to driving, such as traffic conditions ahead and vehicle status, to the vehicle behind, in addition to the turn signal function of existing tail lamps. For example, when an accident situation is detected ahead, it can display the text ‘Accident Ahead’ to send a warning message.

Visitors inspired by Samsung Display’s various form factor products can also design future vehicle interiors directly through AI. By using a tablet PC provided in the booth to select colors and themes, sketch the desired display shape, and then use the generative editing function, visitors can complete their own vehicle interior design equipped with Samsung OLED.

□ Throwing Basketballs at Foldables and Dropping Steel Balls… Attractions Including In-Fridge Displays

Samsung Display has also prepared various attractions where visitors can feel the durability of OLED.

In the ‘Robot Basketball’ zone, 18 foldable panels are attached to the goal backboard to display target images, and a robot arm continuously throws basketballs at the target to conduct a foldable panel impact test. An exhibition comparing durability with competing products by dropping steel balls on foldable panels from a height of about 30cm is also prepared. Samsung foldable OLED is expected to prove its durability by operating stably without screen distortion or structural damage even under impacts from basketballs and steel balls.

In particular, automotive displays requiring high reliability are exhibited inside a refrigerator to prove ultimate image quality that remains unaffected even in extreme environments. OLED, which reacts instantly to electrical signals, has a response speed of 0.2 milliseconds (ms, 1ms is 1/1000th of a second) even in severe cold environments of -20 degrees Celsius, showing little difference from room temperature, whereas Liquid Crystal Displays (LCD), where liquid crystals must physically rotate, slow down to a response speed of 200ms. This results in a time gap capable of traveling a distance of about 2.8m when driving at 100km/h. This means OLED can assist the driver’s driving more stably.

Meanwhile, Samsung Display will also showcase various ultra-high-resolution micro-displays for Extended Reality (XR) devices. In particular, a headset demo product equipped with RGB OLEDoS will be exhibited for the first time. The screen size is 1.4 inches, similar to a wristwatch dial, but the pixel density reaches 5,000 PPI (Pixels Per Inch), meaning the number of pixels approaches three times that of a 4K TV. While previous exhibitions mainly introduced OLEDoS products by embedding panels in walls or boxes, this year, visitors can experience the superior image quality of RGB OLEDoS more vividly through a headset demo product optimized for enjoying immersive content.

OLEDoS (OLED on Silicon) is a display that implements pixel sizes at the level of tens of micrometers (㎛) by depositing organic materials on a silicon wafer. Among them, the RGB method OLEDoS deposits red, green, and blue OLEDs individually to implement colors without a separate color filter, offering a wide color gamut and no color shift even at various viewing angles.

2026 Medium & Large Size OLED Display Annual Report

2026 Medium & Large Size OLED Display Annual Report

China Trends Report Inquiry

China Trends Report Inquiry