The global OLED emitting Materials market reaches USD 2.27 billion… Chinese suppliers begin a full-scale rise in market share

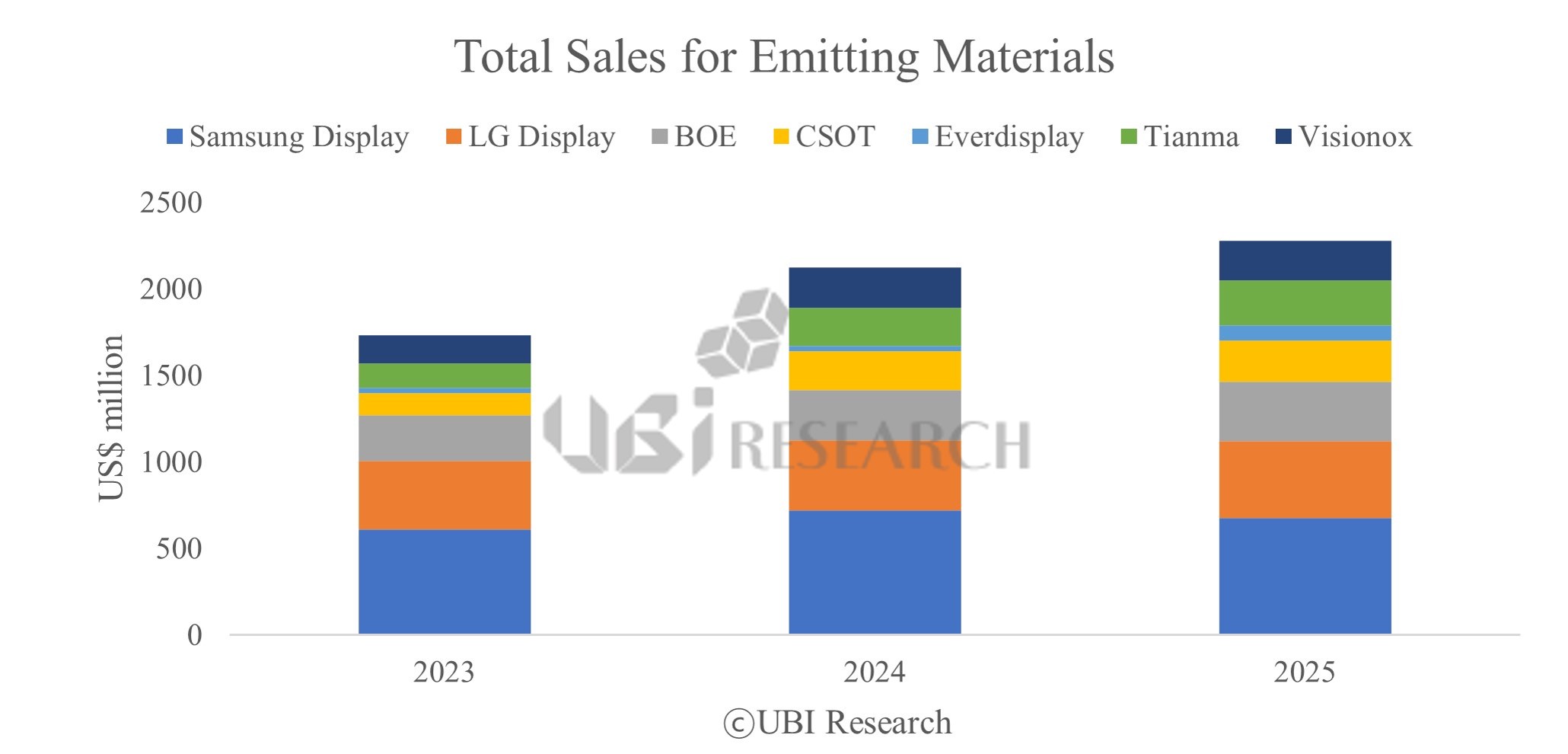

Trend of emitting material purchases by major OLED panel makers from 2023 to 2025. The total market reached $2.27 billion in 2025, with Chinese panel makers’ purchase volume surpassing Korea’s for the first time. (Source: UBI Research)

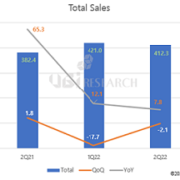

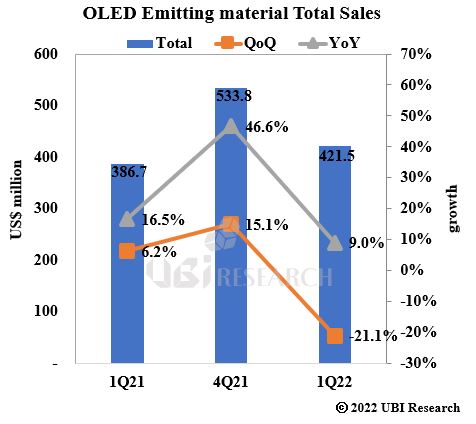

According to UBI Research’s recently published OLED Emitting Material Market Tracker, global revenues of OLED emitting Material suppliers totaled USD 2.27 billion in 2025, up 7.2% year-on-year.

From the third quarter—when mass production of OLED panels for Apple’s new products accelerated—Korean panel makers increased their purchases of emitting Materials. Purchases by Chinese panel makers also remained at a level similar to the previous quarter. As a result, the overall OLED emitting Materials market was larger in the second half than in the first half of the year.

By country, the share of emitting-material purchases by Korean OLED panel makers in 2025 was estimated at about 49.1%, and purchase spending by Chinese OLED panel makers surpassed that of Korean panel makers for the first time.

On the supplier side, revenue growth is becoming increasingly visible not only among Korean, U.S., and Japanese material companies, but also among Chinese OLED emitting Material vendors. UBI Research’s OLED Emitting Materials Market Tracker indicates that while established global suppliers such as UDC, LG Chem, and Samsung SDI continue to maintain high revenue levels, Chinese suppliers—including Beijing Summer Sprout, LTOM, Hyperions, and Jilin OLED—are rapidly expanding deliveries to new OLED panel makers, driving steep revenue increases.

In the mid to long term, the OLED emitting Materials market is expected to expand further. UBI Research forecasts continued growth of the global emitting Materials market, and expects revenue growth among Chinese suppliers—beyond the existing major global players—to accelerate even more.

However, it is expected to take additional time before new Chinese emitting-material suppliers begin supplying materials to Korean panel makers in earnest. In the near term, Chinese suppliers are likely to raise market share rapidly primarily through sales to Chinese panel makers.

Changho Noh, an analyst at UBI Research, commented: “The growth momentum of Chinese OLED emitting Material suppliers is clearly emerging as a threat to established global suppliers. However, for new suppliers to enter the supply chains of Korean panel makers, commercialization procedures such as quality validation, long-term reliability assessments, and customer qualification are essential. Therefore, a full-scale shift in a short period of time is likely to be limited.” He added, “For the time being, market share and revenues are highly likely to expand quickly, centered on supplies to domestic Chinese panel makers, and existing suppliers need to closely monitor the pace at which Chinese suppliers are spreading.”

Changho Noh, Senior Analyst at UBI Research (chnoh@ubiresearch.com)

Pre-register for Display Korea 2026

Pre-register for Display Korea 2026

OLED Emitting Material Market Tracker Sample

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.