Dual Axes of the 2025 OLED Market: Korea’s Premium Focus and China’s Expansion in Shipments

The OLED market in 2024 and 2025 witnessed marked changes in both the demand structure by application and the supply structure by panel manufacturer. The smartphone-centric demand base became more robust, while major Korean and Chinese panel manufacturers, leveraging their distinct strengths, expanded their market contributions, leading to continued diversification in the OLED industry.

By application, smartphones dominated the OLED market in 2024, accounting for 82% of total shipments, reaching 833.8 million units. Watches accounted for 119.7 million units (12%), while other product groups, including tablets, laptops, monitors, and TVs, remained small markets. This structure continued in 2025, with smartphone shipments increasing to 920.7 million units, representing 84% of the total. Watches remained relatively stable at 113.4 million units, and the share of other product groups remained largely unchanged.

OLED shipment share by application, 2024 (left) and 2025 (right) (Source: UBI Research)

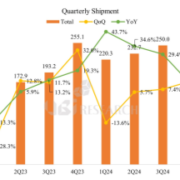

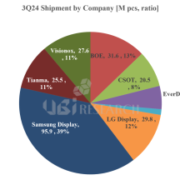

In 2024, the roles of Korea and China in OLED panel supply were clearly divided. Samsung Display maintained its position as the largest supplier with 410 million units (41%), while LG Display recorded 100 million units (11%). In the same year, Chinese panel makers continued their quantitative expansion, accounting for 48% of the total, with a combined shipment of 490 million units: BOE with 138 million units, Visionox with 114 million units, Tianma with 102 million units, CSOT with 83 million units, and EverDisplay with 43 million units.

This structure was further strengthened in 2025. Chinese panel makers, including BOE, Tianma, Visionox, CSOT, and EverDisplay, combined to ship 555 million units annually, accounting for over 51% of the global supply, emerging as a key player in the global supply chain. In the same year, Samsung Display maintained its technology-focused responsiveness, with shipments reaching 411 million units (37%), while LG Display reached 128 million units (12%).

The differences in sales strategies between the two countries were also clear. In 2024, Samsung Display solidified its premium-focused structure with $25.6 billion (57%), while LG Display also achieved $7 billion. Conversely, Chinese companies such as BOE, Visionox, and Tianma demonstrated a trend of expanding sales based on mass production. In 2025, LG Display grew significantly to $11.6 billion, and BOE’s shipments also expanded to $7.1 billion, further separating the two countries’ technology and production strategies.

In summary, the OLED market in 2025 saw a strengthened smartphone-centric demand structure, while Chinese companies accounted for over half of panel shipments, demonstrating a clear shift in regional composition. Korean companies maintained a sales structure centered on high-value-added products, while Chinese companies continued to expand their market presence based on increased shipments. UBI Research Executive Vice President Changwook Han said, “The 2025 OLED market is a period in which the supply structure by region and company is expanding simultaneously, with each company broadening its market response based on its product portfolio and technological capabilities.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Quarterly Small OLED Display Market Tracker Sample

Quarterly Small OLED Display Market Tracker Sample

Quarterly Medium & Large OLED Display Market Tracker Sample

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.