OLED Smartphone Panel Shipments to Reach 900 Million Units in 2025…Q4 Production Drives Annual Growth

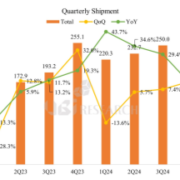

UBI Research forecast trend for quarterly OLED smartphone panel shipments and manufacturer share in 2025 (Source: UBI Research)

According to UBI Research’s quarterly publication, the OLED Display Market Tracker, OLED panel shipments for smartphones and foldable phones are expected to reach approximately 900 million units in 2025. By shipment share, Chinese panel makers are projected to account for about 48.8% of the annual total, nearly matching the level of Korean manufacturers. While shipment volumes between the two countries are similar, Korean companies maintain a revenue advantage due to their higher proportion of premium-tier orders for flagship models such as Apple’s iPhone and Samsung’s Galaxy.

In particular, Korean panel makers saw a significant surge in smartphone and foldable panel shipments in the fourth quarter, marking their strongest performance of the year. Panel supply expanded sharply from the third quarter with the launch of new Apple products, and shipments peaked as Samsung Electronics began full-scale production of Galaxy S26 series panels.

Samsung Display continued its solid growth into the fourth quarter, driven by increasing demand for panels for the iPhone 17 series and Samsung’s Galaxy S25 FE. With mass production for both the iPhone lineup and Galaxy S26 series in full swing, Samsung Display is expected to post its highest annual shipment volume to date. LG Display also achieved a strong rebound in the third quarter with shipments of roughly 20 million units, representing a sharp quarter-over-quarter increase, and its Q4 shipments are forecast to rise by an additional 20%.

Chinese panel makers showed quarterly fluctuations depending on demand conditions but maintained stable supply across major smartphone brands. BOE expanded its customer base by diversifying its supply portfolio from entry-level to upper-mid-range smartphone models. TCL CSOT and Visionox continued to grow shipments to both the domestic Chinese market and global brands, while Tianma focused on enhancing technological competitiveness by increasing the share of high value-added products such as LTPO.

In terms of set makers, Apple secured the largest volume of OLED panels, followed by Samsung Electronics, Xiaomi, Vivo, and Huawei. Executive Vice President Changwook Han of UBI Research commented, “As the industry enters the second-half peak season, Korean display manufacturers are showing clear improvements in both shipments and revenue. In particular, Samsung Display is expected to ship around 150 million panels in the fourth quarter driven by increased demand for iPhone panels.” He added, “Chinese panel makers are also maintaining stable momentum by adjusting their supply strategies in line with shifting market demand.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Quarterly Small OLED Display Market Tracker Sample

Quarterly Small OLED Display Market Tracker Sample

Quarterly Medium & Large OLED Display Market Tracker Sample

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.