Humanoid Display HMI: China Edition – Standards, Policy Framework, and Supply-Chain Roadmap

2025 was recorded as the “first year of humanoid robots,” as a large number of humanoid robots were unveiled, led by the United States and China. Moving beyond a phase in which global robotics companies were primarily validating technical feasibility, 2026 is expected to mark the year when humanoid robots enter a full-scale diffusion phase. As they are deployed into real operations across manufacturing, logistics, and service environments, the pace of adoption on industrial sites is accelerating further, driven by the combination of more advanced AI, localization of key components, and cost reductions. Humanoid robots are no longer a “technology to showcase,” but are increasingly being positioned as labor agents expected to deliver measurable outcomes.

China is at the forefront of this transition. Industrial clusters built around Jing-Jin-Ji, the Yangtze River Delta, and the Pearl River Delta have expanded in scale as supply-chain integration and internalization have rapidly progressed, spanning from core components to finished products. Recent assessments suggest that the total enterprise value of humanoid robot companies in China has exceeded RMB 200 billion, and analysts note that the market is moving into a scaling phase, with clearer stratification from leading players to startups. In particular, as on-site adoption shifts from “proof-of-concept demonstrations” to “repeated deployments,” the importance of mass-producible platforms, stable component sourcing, and standardized operational practices is rising in parallel.

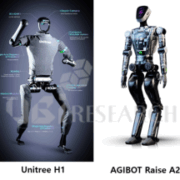

Two defining characteristics of China’s ecosystem are an “ecosystem that has built its own value chain from core components to final products,” and the “growing presence of smartphone OEMs.” Alongside established leaders such as UBTECH and Unitree, emerging challengers such as AgiBot have risen rapidly, broadening the competitive landscape. UBTECH focuses on factory and logistics scenarios centered on its industrial Walker series, while Unitree is expanding from research and education into industrial applications through lineups such as H1 and G1. AgiBot is strengthening its presence by emphasizing mass-production readiness and industrial deployment with product families such as Raise A1 and A2. Meanwhile, smartphone manufacturers such as Honor and Xiaomi are also increasing their visibility in robotics through external events and public initiatives. Leveraging capabilities accumulated in the smartphone industry—AI, cameras, sensors, user-experience (UX) design, and supply-chain operations—they are reinforcing strategies to elevate humanoid HMI (Human–Machine Interface) from a “function-centered” approach toward an “experience-centered” approach. As a result, China is forming a structure in which “industrial (safety, operations)” and “service (interaction, emotion)” directions develop in parallel.

Four major models leading the Chinese humanoid robot ecosystem. UBTECH, Unitree, and AgiBot focus on industrial deployment and mass production, while Xiaomi applies an emotional HMI.

This diffusion phase is being underpinned by China’s distinctive build-out of standards and policy frameworks. China’s Ministry of Industry and Information Technology (MIIT) has designated humanoid robots as a next-generation core product category and has promoted the construction of innovation systems and the upgrading of industry and supply chains through phased targets. In this context, the “Humanoid Robot and Embodied Intelligence Standardization Technical Committee,” launched at the end of 2025, clearly signals an intent to treat standards not merely as regulation, but as an “industrial scaling mechanism.” As concerns grow that insufficient safety requirements, testing and evaluation methods, interoperability, and application guidelines could undermine industry trust relative to the speed of technology and market expansion, standardization is emerging as essential infrastructure that enables field deployment and large-scale adoption. Especially once robots move beyond exhibitions and demonstrations to become operational assets, enterprise customers tend to demand alignment in certification, safety, maintenance, and operational procedures ahead of unit pricing.

From the perspective of “humanoid display HMI,” this standardization strategy is particularly important. In factories and logistics environments—the initial expansion stage for industrial humanoids—HMI prioritizes the “visibility of safety and operations” over emotional expression. Work modes, warning signals, entry into restricted zones, inspection status, and communication status must be immediately understandable to operators, and in environments where multiple robots are operated simultaneously, consistency in indication systems directly affects operational efficiency and safety levels. The fact that the standardization committee is pursuing an end-to-end standards system covering safety and applications suggests that HMI display, warning, and status-expression methods are increasingly likely to be brought into the scope of standardization. In other words, displays are not about creating a “pretty face,” but about providing a common language for managing robots as a system in real operations.

At present, China’s humanoid HMI adoption is evolving clearly in two directions depending on application scenarios. First, industrial function-and-safety HMI is spreading in forms that minimize displays or rely on ruggedized LED light bars and small panel modules to convey status information intuitively. This is a choice intended to reduce breakage risk and power consumption while still securing the minimum visibility required for on-site operations. In this domain, models such as UBTECH’s Walker series, Unitree’s H1 and G1, and AgiBot’s Raise A1 and A2 commonly prioritize “deployment-grade reliability” and “operational visibility,” showing a strong tendency to design HMI around safety and management efficiency. The core of HMI here is less about facial expression and more about clear work-status indication, immediacy of alerts, and consistent interfaces that reduce operator decision time.

By contrast, emotion-and-interaction HMI is evolving toward placing displays at the “front line of dialogue.” By using display modules on the face (head) or chest to enhance guidance and interaction, and by advancing emotion-driven expression based on facial cues, icons, and animations, companies aim to lower the barrier to human–robot communication. Xiaomi’s CyberOne is emblematic of this approach, applying a curved OLED in the facial area to visualize emotions and status. However, it is still too early to conclude that such emotion-centric HMI has become the standard across China’s humanoid landscape, and in the near term, function- and safety-oriented HMI centered on industrial sites is likely to remain the primary driver of diffusion. Moreover, even emotion-centric HMI ultimately must combine with sensors such as cameras and microphones to convey status, intent, and safety, suggesting that interfaces may converge toward designs that integrate both emotion and operations.

From a supply-chain perspective, China’s strengths lie in its deep display manufacturing base—such as BOE, Visionox, and Tianma—and its broad component ecosystem spanning modules, touch solutions, cover windows, and optical parts. The procurement structure for humanoid HMI components is less likely to be explained solely as panel shipments, and more likely to operate as a multi-layer supply chain linking panels, modules, system integration, and robot OEM/ODM players. In some applications, reuse of existing smartphone and tablet components and modules may also occur in parallel. Over the mid-to-long term, there is room for further advancement toward “integrated HMI modules” that combine cameras, sensors, and display functions. China’s capabilities in bulk procurement and manufacturing optimization can strengthen cost competitiveness of HMI components and become a structural factor influencing overall robot price competitiveness. Ultimately, China’s HMI competitiveness is likely to be defined not by the “panel” itself, but by system supply capabilities that encompass modularization, procurement, quality, and service.

In conclusion, China’s humanoid robot industry is clearly entering a phase of “diffusion and performance” starting in 2026. MIIT’s phased roadmap and the actions of the standardization committee can be read as a push to evolve humanoids from simple machines into an “industrial operating system.” In this process, display HMI is being redefined beyond a simple screen, emerging as a safety infrastructure that enables field deployment and a core interface that determines operational efficiency.

Changwook Han, Executive Vice President of UBI Research, said, “The essence of China’s humanoid competition is not only hardware performance, but whether companies can rapidly raise on-site operational efficiency by combining standardized interfaces with large-scale supply chains,” adding that “display HMI will function as a key lever that secures safety, trust, and productivity simultaneously in that process.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Pre-register for Display Korea 2026

Pre-register for Display Korea 2026

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.