Apple Maintains No.1 Position in Smartphone OLED Panel Purchases for Five Consecutive Years… Chinese Vendors Accelerate Catch-Up

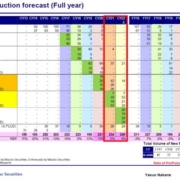

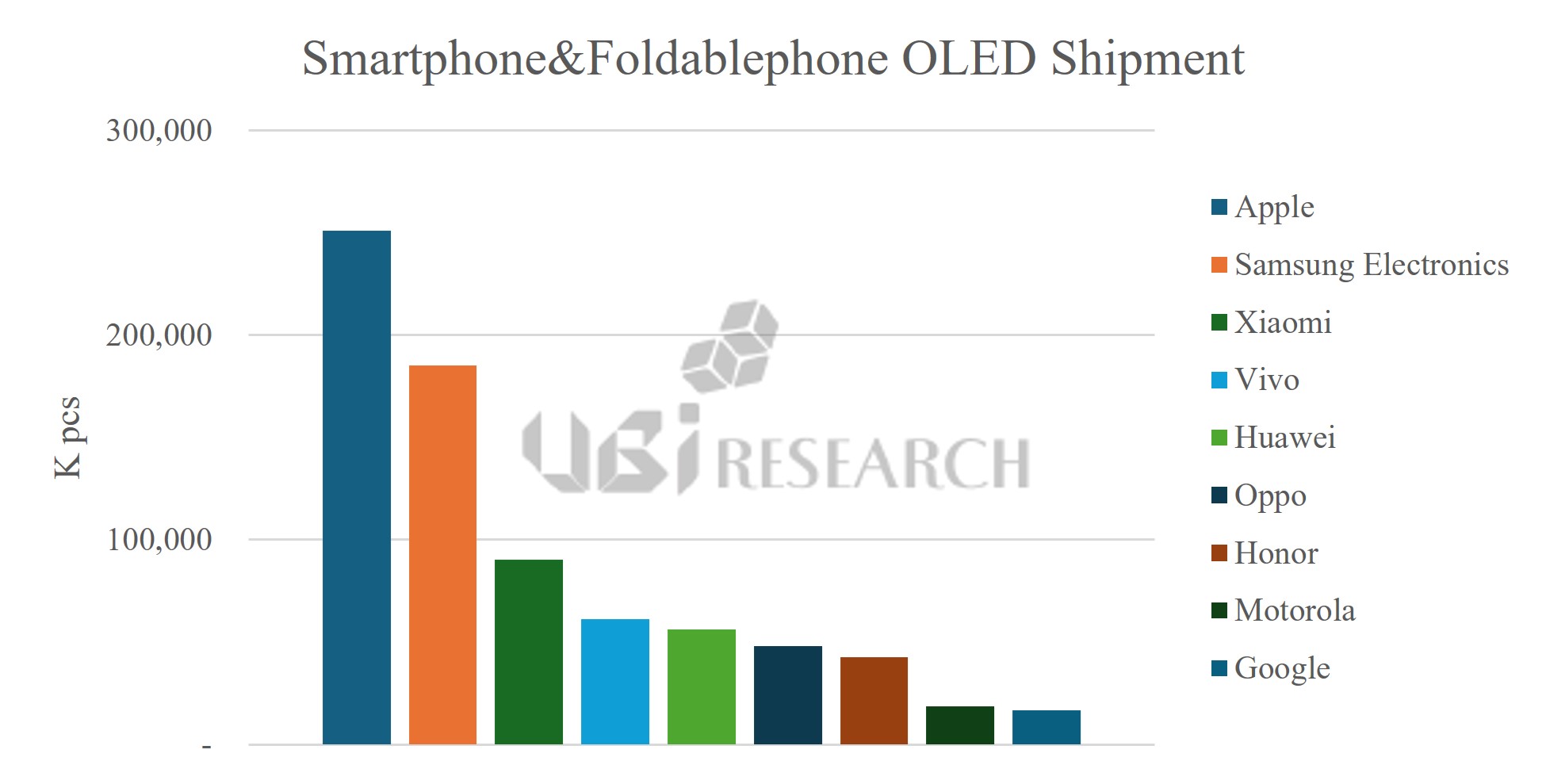

Smartphone and foldable OLED shipments by major brands. Apple leads the market with over 250 million units, followed by Samsung Electronics and Xiaomi. (Source: UBI Research)

According to UBI Research’s recently published “2026 Small OLED Display Annual Report,” Apple ranked first among smartphone OEMs in OLED panel procurement, securing over 250 million smartphone OLED panels and maintaining the top position for five consecutive years. Samsung Electronics followed, with Chinese vendors such as Xiaomi, Vivo, and Huawei trailing behind.

Apple’s procurement of smartphone OLED panels began to increase significantly starting with the iPhone 12 series in 2020. As OLED adoption expanded to include standard iPhone models, Apple received more than 100 million OLED panels in 2020 from the iPhone 12 series alone, which was launched in the second half of the year. In 2021, when both existing and new models adopted OLED, procurement volume increased by 72% year-on-year, making Apple the largest buyer of OLED panels among smartphone OEMs.

Since then, Apple has maintained its position as the largest purchaser of smartphone OLED panels from 2021 through 2025. UBI Research forecasts that Apple is likely to retain its leading position in OLED panel procurement until Samsung Electronics significantly expands OLED adoption in its entry-level smartphone lineup.

Excluding Apple and Samsung Electronics, Xiaomi is identified as the largest OLED panel purchaser among Chinese OEMs. As Chinese panel makers continue to expand supply in line with OEM demand and panel prices steadily decline, the transition to OLED in China’s mid- to low-end smartphone market is expected to accelerate further.

Changwook Han, Vice President of UBI Research, stated, “Following Apple and Samsung Electronics, Chinese smartphone vendors such as Xiaomi, Huawei, Oppo, and Vivo are rapidly increasing OLED adoption, which is becoming a key driver of market growth. Although there may be temporary fluctuations due to component supply issues, OLED adoption is quickly expanding into mid- and low-end models. As a result, the overall smartphone OLED market is expected to maintain steady growth in the mid- to long-term.”

The “2026 Small OLED Display Annual Report” by UBI Research provides comprehensive insights into the small OLED industry, including supply chain relationships between OEMs and panel makers, market share by company, yearly market trends, and future outlook. The report is available on the UBI Research website.

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2026 Small OLED Display Annual Report

2026 Small OLED Display Annual Report

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

China Trends Report Inquiry

China Trends Report Inquiry