At the ICDT 2026 Display Symposium, it was confirmed that Mini/Micro-LED technology is being commercialized alongside technological development by many companies.

High-quality, ultra-large micro-LED panels were exhibited, manufactured using tiling on glass substrates rather than COB substrates. Micro-LED panels utilizing glass substrates are gradually expanding their presence in the ultra-large premium TV market due to their narrow pitch. BOE exhibited an 81-inch (2K, P0.9) TV combining Micro-LED chips with a TFT substrate and plans to begin mass production this year. Visionox exhibited a 135-inch (4K, P0.7) product featuring a micro-LED panel manufactured on a TFT substrate developed by Vistar.

BOE’s 81-inch (2K, P0.9) Micro-LED TV on a TFT substrate, presented at ICDT 2026. (Source: UBI Research)

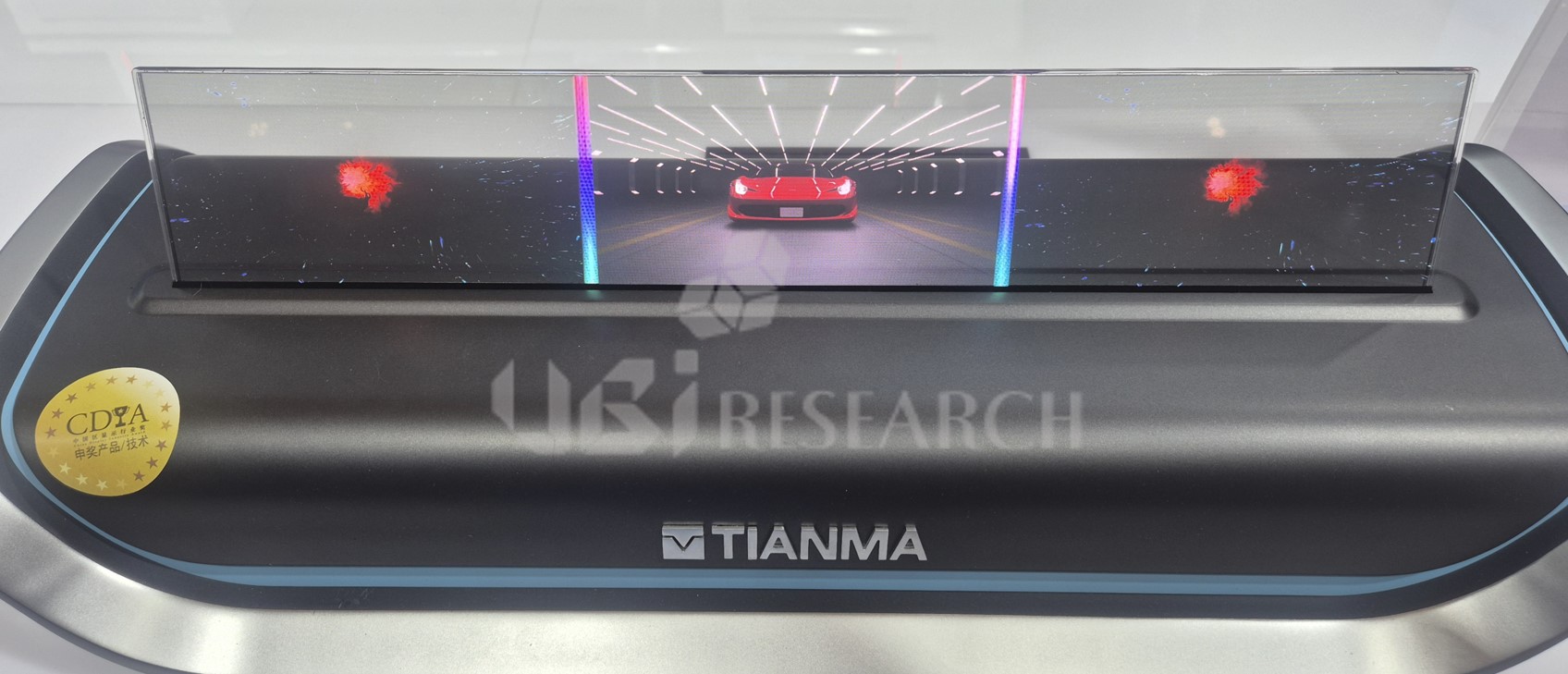

Expectations are growing for Micro-LEDs with high brightness and reliability as automotive displays. Tianma showcased 7-inch and 19-inch high-brightness (>5,000 nits) transparent Micro-LEDs for automotive applications. They feature a transmittance of 60%, a reflectance of less than 2.5%, and an outer border of less than 0.1 mm. While visibility has been enhanced by the high brightness, transmittance needs improvement for automotive applications. Currently undergoing evaluation by clients, their application in automobiles is anticipated.

Tianma’s 19-inch transparent ultra-high brightness Micro-LED. With 60% transmittance and over 5,000 nits of brightness, it is expected to be applied in automotive displays. (Source: UBI Research)

TCL CSOT also showcased a 14.3” ultra-high brightness (panel brightness: 45,000 nits) P-HUD Display and a 4.6” AR-HUD. Micro-LED transparent displays can enhance spatial transparency, technical appeal, and intuitive interaction, so a commercial market is expected to open within a few years.

TCL CSOT’s 14.3-inch ultra-high brightness P-HUD display. Achieving a panel luminance of 45,000 nits, it targets the automotive Micro-LED market. (Source: UBI Research)

Regarding AR devices using Micro-LEDs, TCL CSOT exhibited a 0.05-inch (5080 PPI) Green Mono display product and a 0.28” (5131 PPI) single-substrate Full Color device. At the Micro-LED Technology Forum, discussions focused on improving key core technologies—such as Epi Wafer, Micro-LED chip technology, Mass Transfer and Bonding, and Inspection and Repair—as well as strategies for reducing product costs to expand the Micro-LED product market. It was evident that comprehensive cooperation among material, component, equipment, and panel manufacturers is further necessary for the rapid market penetration of Micro-LED display products.

A report published by UBI Research summarized development cases and technical issues regarding companies developing Quantum Dot (QD) conversion single-chip full-color technology.

Namdeog Kim, Senior Analyst at UBI Research (ndkim@ubiresearch.com)

101 inch Micro-LED Set BOM Cost Analysis For TVs

101 inch Micro-LED Set BOM Cost Analysis For TVs

Industry Trends and Technology of Micro-LED Displays for XR Report

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

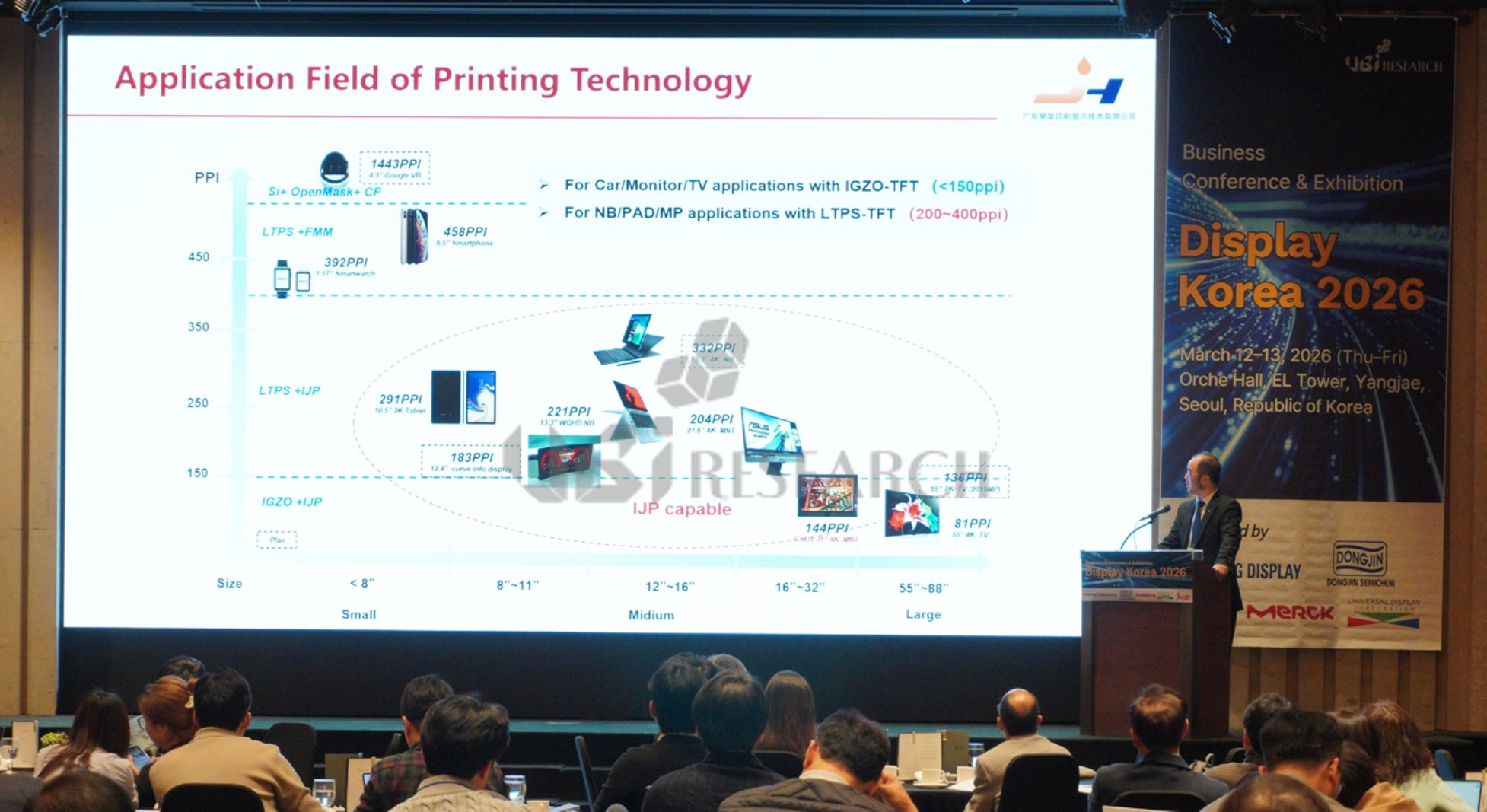

At the keynote session of Display Korea 2026, held on March 12–13 and organized by UBI Research, Fu Dong, General Manager of Guangdong Juhua Printed Display Technology (Juhua), delivered a presentation titled “Development of Printed Display Technology.” He introduced the current development status of inkjet OLED technology and outlined its pathway toward commercialization.

Fu Dong of Juhua introducing the application fields and industrialization direction of printed OLED technology during a keynote speech at ‘Display Korea 2026’ hosted by UBI Research. (Source: UBI Research)

Juhua, an affiliate of TCL CSOT, is a specialized R&D company focused on printed OLED technology. The company is actively advancing solution-processed OLED development while securing mass production capabilities. Centered in Guangzhou, Juhua is building both an R&D platform and an 8.6-generation production infrastructure, positioning itself to lead the commercialization of printed OLED.

Fu Dong emphasized that printed OLED represents a next-generation manufacturing technology capable of replacing conventional vacuum deposition processes. By depositing organic and inorganic materials in ink form, the process enables significant simplification and offers strong cost competitiveness, particularly for large-area applications.

In terms of technical achievements, he highlighted that a printing-based RGB architecture enables high-resolution implementation. Improvements in light efficiency and reductions in internal optical loss have enhanced power efficiency, while advancements in material performance have extended device lifetime.

TCL CSOT officially announced the mass production of printed OLED in 2024 and is establishing a production system based on its Guangzhou 8.6-generation line in 2025. This marks a clear transition of printed OLED from the R&D phase to early-stage mass production.

However, inkjet OLED still faces several technical challenges. These include film stability during ink deposition and drying, precision limitations in high-resolution patterning, the lifetime and efficiency of blue emitters, and achieving uniformity and yield in large-area processes. To address these issues, key approaches include improving printhead precision, advancing compensation algorithms, developing multi-component ink systems, introducing solution-processable blue materials, and adopting tandem structures. These are considered optimal strategies for simultaneously improving performance and ensuring production stability.

Since these challenges cannot be resolved through process innovation alone, they are expected to become critical factors determining future mass production competitiveness. Ultimately, the success of printed OLED will depend not merely on process simplification or cost reduction, but on the ability to translate these advantages into stable yield and product reliability.

As the 8.6-generation IT OLED market continues to expand, how TCL CSOT addresses these technical challenges will be a key point of industry attention.

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2026 Medium & Large Size OLED Display Annual Report

2026 Small OLED Display Annual Report

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

Huawei’s new foldable smartphone ‘Mate X7’, featuring foldable OLED panels from Chinese suppliers. (Source: GSMArena)

As China’s smartphone market grows rapidly, the panel supply chain is entering a full-scale expansion phase. Companies currently supplying foldable OLED panels to Chinese set makers include Samsung Display, BOE, TCL CSOT, Tianma, and Visionox, forming a competitive landscape between global and Chinese suppliers.

In terms of shipments, Chinese panel makers are showing steep growth in foldable OLED supply. Shipments increased from around 1.3 million units in 2021 to over 10 million units in 2025, representing a CAGR of more than 70%. This reflects not only the expansion of China’s foldable smartphone market but also the rapid rise in localization of panel supply.

By company, BOE leads not only in conventional smartphone OLED panels but also in foldable OLED shipments. BOE maintains market leadership by supplying panels to major brands such as Huawei, Oppo, and Vivo. However, after rising sharply through 2024, BOE’s shipments slightly declined in 2025.

TCL CSOT ranks second in foldable OLED supply, shipping more than 3 million units in 2025. Its key customers include Motorola, Xiaomi, and Honor.

Visionox also supplies foldable OLED panels mainly to Huawei and Honor, while Tianma began limited shipments in 2025, marking its formal entry into the market.

Overall, China’s foldable OLED market is transitioning from an early expansion phase to a stage characterized by intensified competition and customer diversification. Going forward, yield stabilization and cost competitiveness are expected to become critical factors shaping the market landscape.

Detailed information on the foldable OLED supply chain structure, panel makers’ development trends, and shipment volumes by company can be found in UBI Research’s China Trend Report.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

Pre-register for Display Korea 2026

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

OLED monitor market trends with over 50% growth expected in 2026, following a 64% surge in 2025. (Source: UBI Research)

Global OLED monitor shipments in 2025 are estimated at approximately 3.2 million units, marking a sharp year-on-year increase. According to UBI Research’s Medium & Large OLED Display Market Tracker, OLED monitor shipments in 2025 rose by about 64% from 1.95 million units in 2024. Growth of more than 50% is also expected in 2026, positioning OLED monitors as the fastest-growing application segment within the mid- to large-sized OLED industry.

This strong growth is closely linked to strategic shifts by panel makers. Samsung Display is focusing on expanding shipments of OLED panels for monitors—centered on its QD-OLED mass production lines—where unit prices and profitability are relatively higher than for TV panels. As adoption of QD-OLED expands across premium gaming monitors and creator-focused products, monitors are taking up an increasing share of Samsung Display’s mid- to large-sized OLED strategy.

LG Display is also maintaining its supply of WOLED TV panels while intensifying efforts to expand OLED monitor shipments. After beginning OLED monitor panel supply at around 100,000 units in 2023, LG Display increased shipments to roughly 200,000 units in 2024 and is estimated to have reached about 400,000 units in 2025. In 2026, shipments are expected to continue rising through new customer acquisitions and improved line utilization.

Behind the panel makers’ growing focus on OLED monitors rather than TVs are production efficiency and profitability considerations. On 8.5-generation glass substrates, TV panels typically achieve a utilization rate of around 60–70%, and even with MMG (Multi Model Glass) technology applied, utilization often remains near 80%. In contrast, monitor panels—based on IT-standard sizes such as 27-inch and 34-inch—can be laid out to achieve utilization rates exceeding 90%. Moreover, on a price-per-area basis, OLED monitor panels offer relatively higher profitability than TV panels, making them an attractive option in terms of both line efficiency and margins.

This trend is not limited to Korean manufacturers. Chinese panel makers are also accelerating their entry into the IT OLED market. BOE is gradually increasing shipments of IT OLED panels, while TCL CSOT is planning shipments of OLED monitor panels based on its in-house inkjet-printed OLED technology. Over the mid to long term, the entry of Chinese players is likely to enhance both price competitiveness and product diversity in the OLED monitor market.

Changwook Han, Vice President of UBI Research, commented, “In the mid- to large-sized OLED market, panel makers’ strategic focus is gradually shifting from TVs to monitors.” He added, “OLED monitors offer both high glass utilization and a relatively stable profit structure.” He further noted, “Not only Korean companies but also Chinese panel makers are actively entering the OLED monitor market with their own technologies, and the OLED monitor segment is expected to continue growing as applications expand across gaming, creator, and premium IT devices.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Quarterly Small OLED Display Market Tracker Sample

Quarterly Medium & Large OLED Display Market Tracker Sample

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

Samsung Galaxy A56 smartphone (Source: Samsung Electronics)

TCL CSOT successfully enters Samsung’s supply chain. (Source: TCL CSOT)

TCL CSOT has successfully supplied flexible OLED panels to Samsung Electronics smartphones for the first time.

According to industry sources, TCL CSOT has begun supplying flexible OLED panels for the Galaxy A57 model and produced approximately 400,000 panels by 2025. Full-scale mass production is expected to expand from 2026, centered on Galaxy A57-bound products.

Historically, the Galaxy A series mainly adopted rigid OLED panels, with Chinese panel makers such as BOE Technology Group having supplied panels in the past. However, as Chinese OLED suppliers streamlined their smartphone rigid OLED lines and Samsung Electronics shifted to single sourcing from Samsung Display for the Galaxy A series, rigid OLED panels for the A series were effectively supplied exclusively by Samsung Display for a period.

With the decision to apply flexible OLED starting from the higher-tier Galaxy A57, Samsung Electronics is understood to have adopted TCL CSOT’s panels to reduce panel costs for the Galaxy A series.

In volume terms, however, the initial supply remains limited. TCL CSOT’s smartphone OLED shipments in 2025 are estimated at approximately 81 million units, meaning the 400,000 units for the Galaxy A57 account for only about 0.5% of its total shipments. The gap is even more pronounced when compared with the volume supplied by Samsung Display to the Galaxy A series.

Nevertheless, the achievement is viewed as notable given the symbolic significance of entering Samsung Electronics’ supply chain and the potential for future expansion in mid-range smartphone lineups.

Currently, Xiaomi is TCL CSOT’s largest customer, accounting for more than 50% of its smartphone panel shipments, followed by Vivo, Motorola, and Huawei.

Industry observers are closely watching whether the Galaxy A57 supply will serve as a catalyst for TCL CSOT to gradually expand its flexible OLED supply opportunities within Samsung Electronics’ mid-range smartphone lineup. While initial volumes are modest, securing Samsung Electronics as a customer is seen as a factor that could enhance TCL CSOT’s competitiveness in the smartphone OLED market over the longer term.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

On January 6, CES 2026 officially opened in Las Vegas, the United States. At this year’s exhibition, automotive displays clearly demonstrated their evolution beyond simple information panels into core interfaces that integrate and intelligently orchestrate the in-vehicle experience. Alongside advances in OLED, Micro LED, and Mini LED technologies, innovations in form factors, transparency, and AI-driven interaction converged to define the future direction of the smart cockpit.

Korean companies highlighted their technological competitiveness by focusing on ultra-large displays, form flexibility, and differentiated user experiences. LG Display redefined the vehicle interior as a continuous digital space by showcasing its pillar-to-pillar (P2P) OLED display extending from the driver’s side to the passenger side. The single-panel P2P OLED, reaching up to 51 inches, delivers high resolution and excellent touch sensitivity while addressing concerns over image quality degradation in large-format displays. LG Display also unveiled a sliding OLED concept that can retract into the dashboard, presenting a cockpit vision in which screen size and function adapt dynamically to driving conditions. In addition, automotive OLEDs incorporating under-display camera (UDC) technology and Dual View functionality emphasized a direction in which a single screen can provide different information simultaneously to the driver and the passenger.

LG Display’s Dual View technology providing different information to driver and co-driver, featured with UDC cluster. (Source: LGD)

LG Electronics showcased applications of transparent OLED based on LG Display’s panel technology, presenting the potential of “invisible interfaces” in automotive displays. Transparent OLED technology enables both open visibility and information display, demonstrating its potential expansion into future applications such as HUDs, panoramic displays, and in-vehicle and vehicle-to-outside communication.

LG Electronics’ Transparent OLED Windscreen and Side-Window solutions displaying info while maintaining openness. (Source: LGE)

Samsung Display also emphasized spatial efficiency and installation flexibility through layout-adaptive automotive OLED solutions. Its 18.1-inch “Flexible L” center information display can be bent into an L-shape to conform to dashboard structures, while the 13.8-inch passenger information display (PID) can be hidden beneath the dashboard when the seat is unoccupied, enhancing space utilization. Samsung Display further highlighted the integration of a robust OLED panel with a 500R curvature on a glass substrate, achieving both visual sophistication and ease of installation.

Chinese companies placed strong emphasis on ultra-large integrated displays and advanced HUD technologies, showcasing their system-level integration capabilities alongside aggressive performance specifications. BOE introduced its HERO 2.0 smart cockpit, emphasizing scenario-based in-vehicle experiences centered on displays. The Micro LED PHUD panoramic head-up display, delivering up to 50,000 nits of brightness, ensures high visibility even under strong ambient light and integrates AI-based voice and gesture recognition to further enhance cockpit intelligence. HERO 2.0, which also includes a 15.6-inch UB Cell central display, an AI audio system, and an integrated digital broadcasting function, clearly illustrates BOE’s strategy of transforming vehicles from transportation tools into living spaces. At the same time, BOE highlighted low-power IGZO oxide displays and carbon-reduction achievements, reinforcing its commitment to environmentally sustainable manufacturing.

BOE demonstrating the HERO 2.0 Smart Cockpit with a 50,000-nit Micro LED Panoramic HUD. (Source: BOE)

TCL CSOT made a strong impression with its 28-inch inkjet-printed OLED applied to a sliding center console and curved armrest, demonstrating notable innovation in form factor design. At its booth, TCL CSOT also conducted live demonstrations of a projection-based HUD (P-HUD). The HVA Ultra P-HUD projects information onto the vehicle’s front windshield using a multi-LCD projection structure, positioning itself as either a replacement for or a complement to conventional dashboard displays. This demonstrated TCL’s strategy of pursuing cockpit integration not only through large OLED panels but also through HUD solutions.

TCL CSOT’s Panoramic HUD solution projecting info on the windshield to replace dashboards. (Source: TCL CSOT)

Tianma presented a next-generation cockpit centered on a 49.6-inch C-shaped panoramic display positioned as an information hub, integrating the instrument cluster, center display, passenger display, and side-mirror areas into a single visual architecture. By leveraging more than 210,000 independent dimming units to achieve a 100,000:1 contrast ratio and suppressing reflectance to below 0.55 percent, Tianma emphasized both readability and safety in ultra-large displays. The company’s multi-screen ecosystem, including a 43.7-inch IRIS PHUD panoramic display, a flexible pull-out display, and a small OLED integrated into the steering wheel, highlighted its strengthening capabilities in system-level cockpit design. Visionox also showcased a dynamic bending display using dual flexible AMOLED panels, presenting an approach that simultaneously improves the stowability and visibility of large screens.

Tianma’s next-gen cockpit and Panoramic HUD system integrating instrument cluster and center display. (Source: Tianma)

Taiwanese companies pursued differentiation through transparent displays and system integration. AUO, through its subsidiary AUO Mobility Solutions, showcased transparent Micro LED displays, INVISY stealth displays, and an AI-based cockpit domain control platform, defining displays as core nodes connected to vehicle computing systems. The integration with a glass-substrate satellite antenna suggested a future in which automotive displays are directly linked to external networks. Innolux emphasized integrated cockpit solutions combining visual and audio technologies through collaboration with CARUX and Pioneer, and unveiled an ultra-high-brightness Micro LED HUD delivering 50,000 nits of direct brightness and 10,000 nits in reflected image brightness, highlighting stable HUD performance even under extreme conditions.

AUO’s Transparent Micro LED display presented as a key node connecting vehicles with external networks. (Source: AUO)

From the automaker perspective, the direction of change was equally clear. BMW presented a panoramic HUD concept for its next-generation iX3, proposing a future HUD architecture that utilizes the entire windshield as an information interface and emphasizing tighter integration between display technology and vehicle design.

BMW’s futuristic Panoramic HUD and iDrive system utilizing the entire windshield as an information interface. (Source: BMW)

Commenting on the automotive display trends observed at CES 2026, Changwook Han, Executive Vice President at UBI Research, stated, “Automotive displays have entered a phase of cockpit platform competition, where form factors, systems, AI, and content converge, rather than remaining a field of individual component competition.” He added, “The advancement toward ultra-large displays, transparency, and sophisticated HUDs will ultimately serve as key indicators of how deeply display makers can engage in shaping the user experience of automakers.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

Official logo of Xian Smart Materials (Source: Xian Smart Materials)

Chinese display materials supplier Xian Smart Material (思摩威) is rapidly increasing its supply share to major panel makers, centered on TFE (Thin Film Encapsulation) ink. Founded in 2017, the company has developed and manufactured TFE ink, low-temperature Over Coat (OC), organic insulating layers, and binders, and is understood to have invested RMB 350 million to build a new manufacturing plant.

Its flagship TFE ink is supplying approximately 70% of the volume for BOE’s B12 line, and pilot production is reportedly underway for BOE’s B7 line. In addition, Xian Smart Material supplies 100% of the volume for Visionox’s V2 and V3 lines, and is also estimated to have secured a 100% share for TCL CSOT starting in December 2025. As panel makers place greater emphasis on encapsulation-process stability and supply-chain optimization, the company’s strengthening line-level supply dominance has become a notable differentiator.

Meanwhile, the company is also expanding its customer base in low-temperature OC (Over Coat). Qualification evaluations are underway with BOE B7 and Tianma, increasing the likelihood of adoption in product categories where reliability under low-temperature operating conditions is critical. Given the narrow process window and stringent reliability requirements for low-temperature OC, the scope of adoption and supply volume will depend on the evaluation outcomes.

On the financial side, 2025 revenue is expected to reach approximately RMB 110 million. With capacity expansion investment and rising share among key customers, near-term growth is likely to be driven by increased shipments of TFE ink, while mid-term growth could be supported by portfolio expansion into low-temperature OC, organic insulating layers, and binders.

Additional SCM-related insights on the Chinese display industry can be found in UBI Research’s China trends report.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

Micro-LED, the pinnacle of “self-emissive” display technology where each pixel generates its own light, is finally shedding its laboratory skin and attempting to enter the living room. At the forefront is TCL CSOT, which has thrown down a bold technical roadmap in a market once considered the exclusive domain of Samsung Electronics. We analyze their three-stage evolution—from CES 2025 through the recent DTC 2025 to the upcoming CES 2026—through the lens of display engineering.

1. [CES 2025] The 10,000-Nit Shock: Pushing the Limits of Inorganic Elements

At CES 2025, TCL CSOT’s 163-inch Micro-LED TV, the ‘X11H Max’, injected significant technical tension into the industry. It wasn’t just about the size; the device achieved a staggering peak brightness of 10,000 nits by individually controlling approximately 24.88 million inorganic RGB chips at the pixel level. This was a landmark event that redefined the standards of “super-gap” picture quality, using the durability of inorganic materials to directly overcome the brightness degradation and burn-in issues inherent in organic-based OLEDs.

TCL’s 163-inch Micro-LED TV ‘X11H Max’ achieving 10,000 nits brightness, surpassing the limits of inorganic devices. (Source: TCL CSOT)

2. [DTC 2025] Technical Maturity in Driving Algorithms and Grayscale Expression

The key takeaway from DTC 2025 (TCL Global Display Tech Ecosystem Conference) was the “evolution of internal substance.” TCL addressed the chronic challenge of Micro-LEDs—color distortion in low-light areas—through its proprietary ‘Hybrid PWM+PAM Driving Architecture.’ This method, which sophisticatedly combines Pulse Amplitude Modulation (PAM) and Pulse Width Modulation (PWM), achieved a 24-bit color depth. It demonstrated technical maturity by perfectly resolving the shapes of objects even in pitch-black darkness through 16.77 million steps of grayscale.

A 219-inch ultra-large Micro-LED display supporting 98% DCI-P3 color gamut and 120Hz refresh rate. (Source: TCL CSOT)

3. [CES 2026 Outlook] Crushing the “100 Million Won” Wall via Mass Transfer Innovation

At the upcoming CES 2026, TCL is expected to move beyond technical posturing and place a practical bet on “price destruction.” Experts predict that TCL will drastically lower the production cost of 100-inch+ models by significantly increasing the yield of the Mass Transfer process—the method of moving millions of microscopic chips onto a substrate. In particular, process efficiency linked with Inkjet Printing (IJP) technology is projected to be the detonator that pulls down Micro-LED TV prices, once exceeding hundreds of thousands of dollars, to the tens of thousands range (approx. 50–80 million KRW).

While past Micro-LEDs were merely “expensive display pieces densely packed with small LEDs,” today’s TCL CSOT is attempting to democratize “nanosecond-level response speeds” and “infinite contrast ratios” by perfectly grafting semiconductor micro-processes onto displays. CES 2026 will serve as the “technological singularity” where Micro-LED moves beyond being a luxury for the ultra-wealthy to become the new standard for premium home appliances.

Joohan Kim, Senior Analyst at UBI Research (joohanus@ubiresearch.com)

2025 Micro-LED Display Industry and Technology Trends Report

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

UBI Research forecast trend for quarterly OLED smartphone panel shipments and manufacturer share in 2025 (Source: UBI Research)

According to UBI Research’s quarterly publication, the OLED Display Market Tracker, OLED panel shipments for smartphones and foldable phones are expected to reach approximately 900 million units in 2025. By shipment share, Chinese panel makers are projected to account for about 48.8% of the annual total, nearly matching the level of Korean manufacturers. While shipment volumes between the two countries are similar, Korean companies maintain a revenue advantage due to their higher proportion of premium-tier orders for flagship models such as Apple’s iPhone and Samsung’s Galaxy.

In particular, Korean panel makers saw a significant surge in smartphone and foldable panel shipments in the fourth quarter, marking their strongest performance of the year. Panel supply expanded sharply from the third quarter with the launch of new Apple products, and shipments peaked as Samsung Electronics began full-scale production of Galaxy S26 series panels.

Samsung Display continued its solid growth into the fourth quarter, driven by increasing demand for panels for the iPhone 17 series and Samsung’s Galaxy S25 FE. With mass production for both the iPhone lineup and Galaxy S26 series in full swing, Samsung Display is expected to post its highest annual shipment volume to date. LG Display also achieved a strong rebound in the third quarter with shipments of roughly 20 million units, representing a sharp quarter-over-quarter increase, and its Q4 shipments are forecast to rise by an additional 20%.

Chinese panel makers showed quarterly fluctuations depending on demand conditions but maintained stable supply across major smartphone brands. BOE expanded its customer base by diversifying its supply portfolio from entry-level to upper-mid-range smartphone models. TCL CSOT and Visionox continued to grow shipments to both the domestic Chinese market and global brands, while Tianma focused on enhancing technological competitiveness by increasing the share of high value-added products such as LTPO.

In terms of set makers, Apple secured the largest volume of OLED panels, followed by Samsung Electronics, Xiaomi, Vivo, and Huawei. Executive Vice President Changwook Han of UBI Research commented, “As the industry enters the second-half peak season, Korean display manufacturers are showing clear improvements in both shipments and revenue. In particular, Samsung Display is expected to ship around 150 million panels in the fourth quarter driven by increased demand for iPhone panels.” He added, “Chinese panel makers are also maintaining stable momentum by adjusting their supply strategies in line with shifting market demand.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Quarterly Small OLED Display Market Tracker Sample

Quarterly Medium & Large OLED Display Market Tracker Sample

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

Demonstration of TCL CSOT’s IJP OLED monitor panel (Source: TCL CSOT)

TCL CSOT’s T8 project, the world’s first Gen 8.6 inkjet printing (IJP) OLED mass-production line, has officially entered the equipment-ordering phase. Following a series of IJP OLED and oxide TFT roadmap disclosures at DTIC 2025 that demonstrated the company’s technical readiness, the project is now showing visible progress on the investment timeline as well.

According to industry sources, orders for core T8 equipment, including inkjet printing systems and deposition tools, are scheduled to begin in December 2024. Inkjet printing, the central platform of the T8 process, determines panel quality, yield, and material utilization; the tool alone is said to account for more than half of the total investment. CSOT is currently engaged in detailed price and specification negotiations with major tool suppliers, while aiming to complete all remaining equipment orders by February 2025. However, with key tool prices trending higher than initially expected, the pace of early investment execution may be adjusted.

CSOT plans to bring in the first batch of equipment for the T8 line in October 2026, though there is a high likelihood that actual delivery could slip toward the end of 2026. Several tool categories still require mass-production-level validation, and negotiations with the inkjet equipment supplier may take longer than anticipated. Even so, the company is maintaining its official target of beginning mass production in the fourth quarter of 2027. Internally, CSOT is said to be preparing mitigation measures to ensure that a 2–3 month delay in tool delivery does not materially impact the overall project schedule.

The strategic significance of the T8 project extends well beyond the addition of a new production line. Inkjet-printed OLED structurally overcomes the process constraints of the conventional FMM (Fine Metal Mask) approach for large-size panels, offering advantages such as material utilization above 90 percent, elimination of large-mask issues, and strong scalability toward high resolution. T8 is designed as a multi-product platform spanning 14–17-inch notebooks, 27–32-inch monitors, and 65–77-inch TVs. Once mass production stabilizes, the T8 line is expected to reshape price-competition dynamics across the IT, monitor, and TV markets.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

TCL CSOT is further solidifying its presence in the next-generation near-field display market and driving changes in the AR and VR ecosystem. Unveiled at the 2025 Global Display Ecology Conference, the two latest micro-displays – a silicon-based Micro LED that delivers ultra-high resolution and a glass-based Real RGB OLED that achieves high PPI – target key requirements for the development of AR and VR devices, respectively. This announcement is particularly noteworthy because TCL CSOT has achieved breakthroughs in both silicon-based and glass-based technologies, creating a significant shift in the technological landscape of the micro-display market.

The most noteworthy product is a 0.28-inch full-color silicon-based Micro LED micro-display. This product delivers full color with high color accuracy on a single chip, and with an ultra-high pixel density of 1280 x 720 and 5,131 PPI, it achieves a “retina-level clarity.” The high-density structure, which makes pixel particles completely imperceptible on small screens, offers significant advantages, particularly in devices with extremely close eye-to-screen distances, such as AR glasses. Furthermore, the silicon-based self-luminous structure facilitates high brightness and a high contrast ratio, enabling a clear image even in small displays prone to brightness loss. Combining Micro LED’s high-efficiency light-emitting characteristics with ultra-high brightness, its ability to maintain clarity even outdoors or in high-light environments is considered a clear competitive advantage over existing OLED-based micro displays.

TCL CSOT 0.28-inch 5,131 PPI Micro-LED display (Source: TCL CSOT)

TCL CSOT’s proprietary quantum dot-based color conversion material is also significant. Combining a single blue Micro LED with a quantum dot color conversion layer, rather than individual RGB chips, for full-color implementation offers significant technological value in terms of simplified manufacturing processes, stable yields, and improved color reproducibility. In particular, managing luminous efficiency and color uniformity is crucial for AR displays, which are undergoing extreme miniaturization. TCL CSOT’s material technology is believed to have significantly addressed these limitations. This high-efficiency material-based approach demonstrates the potential for improved cost structure in future mass production and is a key step toward resolving the color process challenges that have hindered the commercialization of Micro LED AR devices.

On another front, the 2.56-inch glass-based Real RGB OLED is noteworthy. VR and MR displays have relied on silicon-based OLEDs to achieve high PPI, but their high manufacturing costs have limited their adoption in mainstream products. TCL CSOT’s achievement of over 1,500 PPI on a glass substrate goes beyond simple high-resolution performance and signals a potential shift in the VR and MR market structure itself. Adopting a Real RGB pixel structure ensures color accuracy and color coordinate stability, while specifications like a refresh rate of over 120Hz and a contrast ratio of 1,000,000:1 fully meet the demands of high-end VR and MR devices.

TCL CSOT 2.56-inch glass-based Real RGB OLED display (Source: TCL CSOT)

Global big tech companies, in particular, are embracing this same technological trend. Apple, following the launch of its “Vision Pro” in 2024, which uses silicon-based OLEDoS, is reportedly preparing a glass-based MR display for its next entry-level model to reduce costs. This demonstrates a growing shift in the high-resolution VR and MR market, moving away from a silicon-based, single-resolution strategy and toward diversifying substrate structures based on application and price range. The attention given to TCL CSOT’s glass-based, high-PPI OLED is aligned with this industry shift. Glass substrates, with their high cost competitiveness, play a crucial role in popularizing VR and MR. Their ability to lower price barriers while maintaining high resolution is likely to impact the entire global supply chain.

TCL CSOT’s technological advancements in both silicon-based Micro LED and glass-based OLED demonstrate the growing emphasis on high-density, low-power, and high-brightness requirements for future AR and VR devices. Micro LEDs, with their high brightness, peak performance, low power consumption, and long lifespan, are particularly suited for ultra-compact and lightweight devices centered around AR glasses. OLEDs, with their wide color gamut and high-quality image quality, enhance the immersive experience of VR and MR headsets. As the complementary nature of these two technologies becomes more evident, the micro-display market, which had stagnated in recent years, is rapidly expanding again.

UBI Research Executive Vice President Changwook Han commented on this technology announcement, saying, “Micro LED and high-resolution OLED are key technologies that determine the completeness and user experience of AR and MR devices.” He added, “Micro LED, in particular, is at a critical turning point that will accelerate the commercialization of AR glasses in terms of brightness, power, and lifespan. The proliferation of glass-based, high-PPI OLEDs will lower the cost barriers in the VR and MR markets, rapidly accelerating the expansion of mass-market models.” He summarized the future direction of the micro-display ecosystem as “lightweight, low power, and high definition,” predicting that companies that comprehensively optimize not only technology but also optics, materials, and actuator quality will secure future competitiveness.

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2025 Micro-LED Display Industry and Technology Trends Report

EU PFAS REACH restriction proposal timeline

China’s display panel industry is accelerating its transition to PFAS-free production in response to the European Union’s (EU) strengthened regulations on PFAS (Per- and Polyfluoroalkyl Substances, persistent harmful chemicals). The EU’s REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) PFAS substance restriction regulation is based on an initial proposal submitted in January 2023 by five member states: Denmark, Germany, the Netherlands, Norway, and Sweden. Following a public consultation from March to September 2023, which gathered over 5,600 comments, an updated Background Document was published on August 20, 2025.

This regulation proposes restriction options due to the environmental and health hazards posed by PFAS’s persistence, mobility, and bioaccumulation. Concentration limits were set at 25 ppb for individual PFAS, 250 ppb for group totals, and 50 ppm for all PFAS (including polymers). The Commission will publish the amended REACH regulation in December 2025. Following deliberation by the Parliament and Council, full implementation will commence in 2027. Essential use exemptions (e.g., medical devices, safety-related applications) will undergo strict scrutiny and will only be permitted when no alternatives exist. Penalties, determined by member state laws, include administrative and criminal sanctions, posing a significant risk of export bans for violations. This regulation forms part of the EU’s ‘Chemical Strategy for Sustainability’ (2020), aiming for an 80% phase-out of PFAS by 2030.

These regulations are expected to directly impact OLED and LCD processes in the display industry (cleaning agents, coating agents, etc.), prompting major Chinese companies to reassess supply chains and develop alternatives. For the display industry, developing PFAS-free alternatives (such as silicon-based coatings) for OLED deposition and cleaning processes is a key challenge. China’s display industry, with its high export share to the EU, is expected to face impacts across its entire supply chain.

BOE is reevaluating key materials for its European exports—including photoresist (PR), polarizers, and cleaning solutions—to comply with EU REACH standards. It has requested suppliers like Japan’s JSR and Shin-Etsu Chemical to switch to non-fluorinated alternatives and is testing silicon-based coatings on a pilot line at its Hefei plant. Considering the EU market’s 22% share of its total sales, non-compliance by 2026 could risk halting exports. BOE is concurrently improving its AMOLED processes, primarily at its Chongqing and Hefei plants, while constructing an 8.6-generation AMOLED line (B16) with a target lighting-up date of late 2025. The LCD product line, with its lower process complexity, plans to prioritize the transition to PFAS-free materials by 2027. Notably, for Apple supply, PFAS-free materials are scheduled for application starting with the iPhone 18 series. BOE is evaluating PFAS-free options from Rouxian (柔显) and Mitsubishi Chemical to replace the Black PDL (Pixel Definition Layer) material. Black PDL is a core material in the Pol-less OLED structure, contributing to reduced device thickness and improved efficiency.

TCL CSOT is enhancing its process to minimize PFAS usage by leveraging inkjet printing (IJP) technology. Its 8.6-generation OLED factory, which broke ground in Guangzhou in November 2025, applies IJP to directly print RGB materials without fluorine-based vapor deposition processes, expecting a 20% cost reduction and improved energy efficiency. TCL CSOT highlighted the potential for minimizing PFAS use, reducing costs by 20%, and improving energy efficiency at SID Display Week 2025.

Visionox is reducing PFAS dependency with its FMM-free ‘ViP (Visionox intelligent Pixelization)’ technology. This photolithography-based pixel patterning reduces PFAS exposure during cleaning and coating steps. Construction of its Hefei 8.6-generation OLED factory commenced in late February 2025.

China’s Ministry of Industry and Information Technology (MIIT) set a 70% domestic substitution rate target for PFAS alternatives by 2026 in its ‘PFAS Usage Restriction Roadmap’ announced in December 2024, while expanding R&D subsidies for companies like BOE and TCL CSOT. This represents national-level support linked to semiconductor and display self-sufficiency policies, bolstering China’s OLED shipment expansion. The MIIT roadmap prioritizes banning specific PFAS like PFHxA and PFOA, similar to the EU REACH regulation, aiming for full implementation by 2027.

Changho Noh, Senior Analyst at UBI Research (chnoh@ubiresearch.com)

TCL CSOT Inkjet OLED Presentation Slide at K-Display 2025 (Source: TCL CSOT)

TCL CSOT officially announced the commencement of construction for its 8.6-generation printed OLED display panel production line (T8 Project) in Guangzhou Province on October 21, 2025. This starts approximately one month ahead of the original schedule, with a total investment of 29.5 billion yuan (approximately 5.4 trillion won). This project represents the world’s first 8-generation printed OLED line, targeting the mid-sized application market for notebooks, monitors, and automotive displays. It is planned to have a production capacity of 45K sheets per month (based on 2290mm x 2620mm substrates). TCL CSOT is investing in the T8 line on the site adjacent to the existing Guangzhou T9 line. The T8 site was originally planned for conversion into a solar project, but that plan has been put on hold, and its use as an OLED production line site has been confirmed. This T8 line investment will proceed in two phases, with the first line being invested initially. Phase 1 will have a monthly substrate input capacity of 15K. Equipment installation is targeted for September 2026, with trial mass production scheduled for June 2027.

In response to the rapid growth of the mid-sized OLED market, major display companies are accelerating investments in 8.6-generation lines. TCL CSOT has chosen a differentiated approach with printed OLED, focusing on cost competitiveness and technological innovation. TCL CSOT’s printed OLED technology achieves material utilization exceeding 90%, significantly surpassing the 30% rate of vapor deposition methods, and reduces manufacturing costs by over 20%. This cost advantage is interpreted as a strategy to seize the ‘leadership in the mid-to-low-end market’ and popularize OLED. Furthermore, as the Chinese government tends to strictly review investment approvals for existing technologies like FMM, companies like Visionox (ViP) and TCL CSOT (inkjet) are proceeding with investments by applying new technologies.

According to UBI Research’s analysis, printed OLED still faces technical challenges.

TCL Huaxing’s move toward printing technology is interpreted as an attempt to position itself as an ‘innovative force leading the market’ by targeting the mid-sized OLED market with new technology, rather than directly challenging deposition market giants like Samsung Display and BOE.

Printed OLEDs are expected to significantly lower the barrier to entry for the IT OLED market (notebooks, monitors, etc.) through groundbreaking cost reductions, thereby expanding the market pie. However, concerns also persist about whether the brightness and lifespan challenges inherent to the printing process can meet the stringent quality standards of large IT products. Attention is focused on whether TCL CSOT can successfully overcome these technical hurdles and become a game-changer in the mid-sized OLED market by 2027 through its ‘technology-cost-scale’ trinity strategy.

Changho Noh, Senior Analyst at UBI Research (chnoh@ubiresearch.com)

Xiaomi 17 Pro Max unveiled with TCL CSOT Real RGB OLED panel (Source: Xiaomi)

On September 25th, Xiaomi unveiled three new smartphones, the Xiaomi 17 Series (Regular, Pro, and Pro Max). TCL CSOT has announced that it will exclusively supply all displays (front + back) of the Xiaomi 17 Pro and 17 Pro Max. The Pro Max’s main display is a 6.9-inch 1200×2608 high-resolution LTPO AMOLED panel with a 120Hz refresh rate and 3,500 nits of brightness. The rear is also a 2.9-inch LTPO AMOLED with a resolution of 596×976.

TCL CSOT has been working on developing a Real RGB structure using inkjet printing technology for a long time, so some speculated that the Xiaomi 17 Pro Max would also feature this technology. However, the Real RGB structure is actually realized through a Fine Metal Mask (FMM) process. This means that each pixel is composed of independent red, green, and blue subpixels, resulting in excellent clarity and accurate colors without any loss of resolution.

The diamond pixel structure, which Samsung Display primarily uses, has the advantages of higher luminous efficiency, more resistance to burn-in, and higher perceived resolution while reducing the number of physical pixels, which is advantageous for cost-effective high-resolution implementation. It also has strong patent protection, which has acted as a barrier to entry for other companies. However, it has been pointed out that the diamond pixel structure does not have the same number of R, G, and B subpixels, which can cause slight readability degradation or color bleeding, especially in small text or complex graphics.

TCL CSOT’s Real RGB structure appears to be a strategic move to improve visual quality, including color accuracy and text readability, and to avoid Samsung patents. TCL CSOT’s continued investment in inkjet printing Real RGB technology, while supplying FMM-based Real RGB for major products like the Xiaomi 17 Pro Max, suggests that TCL CSOT is actively exploring both technological paths. While inkjet printing has potential for large OLEDs and cost-effectiveness in the long term, there are still challenges to overcome, including technical difficulties, mass production, and reliability, before it can be applied to small, high-resolution products.

TCL CSOT’s new panel features a C10 set, the latest emissive layer stack structure, to improve luminescence efficiency and stability. A particularly noteworthy point is that among the core light-emitting materials, Lumilan’s material was applied instead of the DuPont product previously used for the Red Host. Founded in 2017, Lumilan is a Chinese company specializing in OLED materials, backed by China’s Jizhi Technology and Xiaomi Changjiang Industrial Fund. With a factory in Ningbo, Zhejiang Province, the company has been focusing on the R&D, production and sales of OLED emitting materials, and has strengthened its strategic partnership with Xiaomi, including the establishment of a joint research center in 2022. The Xiaomi 17 Pro Max application is the fruit of that cooperation. The replacement of one of the main core luminescent materials with a Chinese company’s product heralds a new change in the supply chain of the global display industry.

Changho Noh, Senior Analyst at UBI Research (chnoh@ubiresearch.com)

OLED emitting material market share trends by nation (Source: UBI Research)

According to the Q3 Emitting Material Market Tracker recently published by UBI Research, Korean panel makers maintained their lead over Chinese competitors in total OLED emitting material purchases in the first half of 2025. Korean panel makers purchased approximately 36.7 tons, accounting for 59.9% of the total, while Chinese panel makers purchased 24.6 tons, representing 40.1%. By quarter, Korea recorded 18.6 tons versus China’s 12.8 tons in Q1 2025, and 18.1 tons versus 11.8 tons in Q2, continuing a stable lead.

While Korea continues to dominate the overall OLED emitting material market, the smartphone segment shows a different trend. Since 2025, Chinese panel makers have consistently exceeded 50% market share on a quarterly basis, surpassing Korea in the first-half total as well. This indicates that although Korea remains ahead in the overall OLED emitting material market, China’s share is steadily expanding in smartphones, a core application segment. Backed by its strong domestic demand, China has rapidly increased shipments, suggesting that the balance between the two countries is gradually shifting in the medium to long term.

By company, Samsung Display accounted for about 40% of the total OLED emitting material purchases, maintaining the largest share, followed by LG Display, BOE, and Tianma. In contrast, in the smartphone OLED emitting material market, BOE closely followed Samsung Display, with Tianma, TCL CSOT, and LG Display trailing behind. Thus, while Korean panel makers still demonstrate clear strength in the overall market, Chinese panel makers are making notable strides in the smartphone sector.

UBI Research analyst Noh Chang-ho stated, “Although Korea has been overtaken by China in the smartphone OLED emitting material market, Samsung Display and LG Display remain ahead in the overall OLED market, supplying IT panels, QD-OLED, and WOLED,” adding, “However, as Chinese panel makers expand shipments of smartphones and foldables, along with increasing IT OLED production, the gap between Korea and China in the emitting material market is narrowing rapidly.”

Changho Noh, Senior Analyst at UBI Research (chnoh@ubiresearch.com)

TCL CSOT’s latest inkjet OLED technology presentation at K-Display 2025 (Source: TCL CSOT)

At the business forum of K-Display 2025, held from August 6-9, China’s TCL CSOT said it will announce its investment plans for an eighth-generation inkjet OLED production line. The project, dubbed the “T8 Project,” is planned to begin trial production in June 2027, with equipment delivery targeted for September 2026. The initial production capacity is expected to be 15,000 sheets per month in the first phase. The investment is seen as a significant move to challenge the dominant position of South Korean companies in the large OLED panel market.

The Inkjet Printing method adopted by TCL CSOT has a number of advantages over the Vacuum Deposition method currently used for large OLED production.

One of the main technical challenges with inkjet OLEDs has been the lifetime of blue OLEDs, but TCL CSOT has made significant improvements. The company says its blue lifetime, which was just 40 hours in 2020, is now 400 hours, a tenfold improvement. In addition, the resolution has exceeded 350 PPI, which can meet the needs of high-performance tablets and laptops; the aperture ratio has been increased to three times that of conventional FMM (Fine Metal Mask) OLEDs to reduce power consumption; and the size of blue subpixels has been reduced to be similar to red and green, improving display quality.

Meanwhile, the printing equipment for the 8th generation OLED inkjet line is likely to come from Panasonic Production Engineering. Panasonic Production Engineering announced at SID 2025 that it has developed an 8.5-generation machine with a 1 pL (picoliter) inkjet head and 350 ppi resolution. The machine achieved an accuracy of 4.6 µm, exceeding the target accuracy of 5.8 µm, demonstrating the possibility of stable mass production of large substrates. The expected equipment configuration will consist of a Hole Injection Layer, Hole Transport Layer, and printing equipment for RGB pixel printing, as well as equipment for tandem OLEDs. Panasonic’s equipment enables the production of high-resolution displays through high-frequency jetting (20 kHz) and droplet volume control as fine as 1.0 pL, which are key technologies for improving the productivity of the inkjet process. The company also reports that production stability is enhanced through a sophisticated system that compensates for thermal deformation and micro-alignment errors.

Inkjet OLED technology still has many challenges to overcome. While current technology has improved device lifetime, there is ongoing debate about whether it has achieved sufficient lifetime for commercialization. There are also limitations that make it difficult to implement tandem structures for high brightness and low power consumption. These challenges are directly related to the yield of the production line and require continuous technology development for successful mass production of inkjet. Nevertheless, TCL CSOT’s technological advancements show that inkjet OLEDs are getting closer to reality.

If TCL CSOT’s eighth-generation inkjet OLED investment materializes, it will pose a direct challenge to the mid- to large-sized OLED market dominated by South Korea’s Samsung Display and LG Display. Currently, these two companies rely on a costly vacuum deposition process, which keeps OLED TV prices high. Mass production using inkjet technology can bring cost competitiveness, which will significantly reduce the price of OLED TVs and increase market penetration. Furthermore, the technology is expected to impact not only the TV market, but also the laptop, tablets, and professional monitor markets. Inkjet technology can become an important steppingstone for China’s display industry to secure technological leadership in the OLED field, following LCD.

Changho Noh, Senior Analyst at UBI Research (chnoh@ubiresearch.com)

As in-vehicle display technologies continue to evolve rapidly, the head-up display (HUD), which projects various types of information into the driver’s forward field of view, is becoming an essential interface in modern vehicles. Recently, Panoramic HUDs (PHUDs) capable of displaying not only speed and navigation data but also augmented reality (AR) content have emerged, showcasing significant technological advancement. At the core of this evolution is Micro-LED technology, which is gaining traction as the key enabler of PHUDs.

PHUDs project information across the entire or a substantial portion of the windshield, requiring a wide field of view, high resolution, and high brightness. Currently, the most commercially viable implementation is the black strip reflection method. This approach utilizes the lower black band area of the windshield as a reflective surface, allowing for a simpler optical system and lower production costs—making it an attractive option for many automakers. However, to avoid obstructing the driver’s view, the image projection height is limited, typically restricted to a narrow vertical range of approximately 3 to 6 cm.

BMW Panoramic Vision

For a more immersive and premium experience, some high-end vehicles adopt a transparent reflection method. This involves embedding multilayer optical films or applying special structures within the windshield, allowing images to be reflected even in transparent areas without the need for a black band. While this method offers advantages in immersion and design, it poses significant challenges in optical complexity, higher costs, and low reflectivity—necessitating the use of ultra-bright displays.

Micro-LED provides a compelling solution to these structural and technological challenges. Thanks to its self-emissive pixel structure, Micro-LED can achieve brightness levels exceeding 1,000 nits, with ultra-high brightness capabilities reaching 30,000 to 50,000 nits—all while maintaining excellent power efficiency.

At SID 2025, major display companies such as AUO, BOE, and CSOT unveiled a range of Micro-LED-based PHUD prototypes. BOE showcased a 6.2-inch Micro-LED HUD with sub-0.2mm pixel pitch and 30,000 nits peak brightness (15,000 nits perceived brightness). CSOT presented a large 14.3-inch PHUD featuring 45,000 nits peak brightness (12,000 nits perceived brightness) and a wide viewing angle, while AUO demonstrated a 13-inch high-brightness PHUD with 12,000 nits of perceived brightness.

AUO 13” PHUD (12,000nits)

BOE 6.2” PHUD (15,000nits)

TCL CSOT 14.3” PHUD (12,000nits)

Micro-LED is not merely enhancing display performance—it is fundamentally transforming the structure and implementation of Panoramic HUDs. It overcomes the limitations of restricted reflection areas, enables the projection of high-brightness, high-resolution images onto various curved windshields, and meets the demands for transparency and design flexibility. As the commercialization of PHUDs becomes a reality, Micro-LED stands at the center of this transformation. The future of automotive vision and interface will unfold on Micro-LED.

Changwook HAN, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report

Plans for 8.6G OLED Line Construction by Panel Makers

Monthly Production Capacity of 45K; Equipment Installation Targeted for End of 2026

According to UBI Research’s China Market Trend Report, Chinese display company TCL CSOT (China Star Optoelectronics Technology) is planning to construct a new 8.6-generation (2290x2620mm) OLED line at the T8 site near its existing T9 OLED line in Guangzhou. This investment will be based on inkjet printing technology, with a Step 1 investment fund scale of approximately RMB 20 billion (approximately KRW 3.8 trillion).

The T8 site was initially intended to be converted for a solar project, but that plan has been put on hold, and the site will now be used for its originally planned OLED production line. The T8 project is designed to consist of two 8.6G OLED lines with a total monthly production capacity of 45,000 substrates (45K), and the initial investment will be made for one line.

The investment schedule for the T8 line includes an official announcement in July 2025, groundbreaking in October, and the start of equipment installation by the end of 2026. The general manager of the project has been appointed as Linpei (林佩), and the core inkjet process technology is being led by a Korean expert.

Inkjet printing technology is known for its approximately 30% lower equipment investment cost compared to the traditional mask-based deposition method. For example, Samsung Display is investing around KRW 4 trillion to build an 8.6-generation OLED line for IT applications (15K per month) at its A6 site in Asan, Chungcheongnam-do, based on the conventional deposition process. In contrast, TCL CSOT plans to adopt inkjet printing technology to secure a monthly production capacity of 45K at the 8.6-generation level, with an initial investment of RMB 20 billion.

Han Changwook, Executive Vice President of UBI Research, commented, “Inkjet OLED still faces technological challenges in brightness, lifespan, large-area uniformity, and yield. Nevertheless, China is positioning this differentiated technology from traditional deposition as a next-generation growth driver and, under strategic government support, is preparing for full-scale mass production. Through investments in inkjet technology by TCL CSOT and ViP (Visionox intelligent Pixelization) by Visionox, China is pushing ahead with the first mass production of large-area OLEDs, aiming to secure technological leadership.”

As demand for IT displays is expected to grow, it remains to be seen whether the commercialization of inkjet technology in large-area OLEDs will determine future market leadership.

Changwook HAN, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Huawei’s MateBook Fold

The foldable device market is rapidly expanding beyond smartphones into medium-to-large display segments such as tablets and laptops. Recently, Amazon and Huawei have begun developing and releasing foldable tablet and laptop products, marking a significant step in market expansion. Apple is also reportedly preparing to launch a foldable tablet PC after 2027.

Amazon is currently developing an 11.3-inch foldable tablet PC, with the display panel being supplied from BOE’s B12 production line. The first samples are scheduled for delivery in Q1 2026, with mass production set to begin in April of the same year. The planned production volume is approximately 1 million units, and the cover window will use Ultra Thin Glass (UTG).

Meanwhile, on May 19, Huawei officially launched its first foldable laptop, the MateBook Fold. The device features an 18-inch display when unfolded and functions as a 13-inch device when folded. It offers a 3.3K resolution and a 4:3 aspect ratio. The weight is 1.16 kg, and the thickness when unfolded is only 7.3 mm. The display is supplied by Chinese OLED panel maker TCL CSOT and adopts LTPO and tandem structures, achieving about 30% power consumption reduction compared to previous models. The folding radius is 1.5 mm based on Token UTG, significantly enhancing durability. In fact, its shock resistance is reported to be improved by approximately 200%.

Apple is also developing a foldable tablet and is expected to launch the product as early as 2027 or as late as 2028. Samsung Display is anticipated to be the initial supplier of panels for Apple’s foldable tablet PC. Industry watchers believe Apple’s entry will serve as a catalyst for growth in the medium-to-large foldable display market.

While foldable devices have traditionally been limited to smartphones, they are now expanding into tablets and laptops, creating new demand. This shift is accelerating the evolution of related display technologies and component ecosystems.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

This year, companies are engaged in intense competition to develop Micro-LED HUD products for automotive use at display exhibitions such as CES, Touch Taiwan, and SID. Major panel manufacturers such as AUO and Innolux in Taiwan, and BOE, TCL CSOT, and Tianma in China have unveiled a host of new products. These companies are the main suppliers of LCD HUD products.

AUO exhibited a 13-inch micro LED AR HUD, while Innolux’s CarUX implemented a HUD on the windshield using a 9.6-inch Micro-LED reflective display solution with 9.6-inch Micro- LED.

AUO 13” AR HUD

BOE showcased two HUD display solutions at SID. One is a 6.2-inch (624×360) RGB Micro-LED HUD, and the other is a monochrome Micro-LED HUD achieving up to 300,000 nits. TCL CSOT unveiled a 14.3-inch (1700 x 650) Micro-LED PHUD, while Tianma showcased an 8-inch (1204×608) HUD.

BOE 6.2” HUD

TCL 14.3” HUD

Tianma 8” HUD

These products achieve high resolution and high contrast ratios based on the advantages of Micro-LEDs, offering differentiation and the potential to replace existing LCOS products. As a result, panel manufacturers are engaging in intense competition to secure a technological lead in the market.

According to UBI Research’s “2025 Automotive Display Technology and Industry Trend Analysis Report,” this year’s vehicle display shipments are expected to exceed 240 million units, with Mini-LED and OLED panels gradually increasing. As competing technologies, companies are actively developing differentiated technologies applied to Micro-LED HUD products.

In summary, automotive displays are one of the key areas of the future display market. As the importance of displays has grown as a key differentiating factor in smart cars, the automotive display market will become an essential competitive arena for panel manufacturers. In other words, with the smart evolution of vehicles, HUDs will become mainstream, and companies will need to respond and compete accordingly.

Namdeog Kim, Senior Analyst at UBI Research(ndkim@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report

Over the past few years, we have analyzed trends in micro-LED technology and products. Along with the advancement of mini-LED backlight technology, micro-LED has emerged as the next-generation display technology, and interest is growing in when micro-LED will enter the mainstream market. Major display companies and research institutions in countries such as China, Taiwan, South Korea, the United States, and Europe have been accelerating technology development and product commercialization through years of investment, achieving a significant transition from the laboratory stage to mass production. However, the market share of micro-LED in the overall display market remains low, and the pace of commercialization as a mainstream product is still slow.

Samsung Electronics has been leading the way in next-generation display technology with its giant micro-LED TV, ‘The Wall,’ for several years now. Now, with price competitiveness and production efficiency improvements, the company is at a point where it needs to expand into the consumer market in earnest.

Taiwan’s AUO recently showcased automotive micro-LED displays and mirror displays at CES and Touch Taiwan, focusing on targeting the B2B market. The company aims to begin mass production of its 4.5-generation micro-LED production line this year. PlayNitride is preparing to mass produce panels for smartwatches and AR glasses based on its high-brightness, high-resolution technology.

Chinese companies BOE, TCL CSOT, and Tianma are expanding their demonstrations and investments in micro-LED panels and are leading the way in preparations for mass production. BOE’s subsidiary HC SEMITEK is promoting the construction of a micro-LED Epi wafer manufacturing, chip production, and packaging base in Zhuhai City, and at the end of last year, it announced the start of production of a 6-inch substrate micro-LED mass production line. TCL CSOT is preparing to enter the TV and automotive display markets through a joint research institute established with Sanan in 2020 and a joint venture, Extremely Display, to develop and commercialize products. Tianma completed its TFT-based micro-LED production line in December last year and is ready to begin small-scale shipments in phases starting this year. In addition to leading in mass production speed, the company is also accelerating technological advancements such as improving yield rates for 6-inch wafer Micro LED, enhancing laser transfer efficiency, and refining precise tiling bonding. This has been confirmed through the company’s efforts to showcase technological improvements and strengthened productization at technology exhibitions.

At the international business conference ‘OLED & XR KOREA 2025’ hosted by UBI Research, presentations on Micro-LED technology and market trends were provided for TV/large-screen displays, AR, smartwatches, and automotive displays.

According to UBI Research’s analysis, the Micro-LED consumer market is expected to be driven by TVs and AR glasses by 2027, with smartwatches and automotive displays gaining market share by 2028. It is predicted that Micro-LED will break into the mainstream market around 2028, moving beyond premium product segments.

More detailed information and technical analysis will be provided in a report to be published by UBI Research at a later date.

Nam Deog Kim, UBI Research Analyst(ndkim@ubiresearch.com)

Micro-LED Display Technologies for XR Applications Report Sample

‘1Q25 Small OLED Display Market Track’

According to UBI Research’s ‘1Q25 Small OLED Display Market Track’, which includes application performance and outlook for smartphones, foldable phones, smartwatches, etc., small OLED shipments in 2024 are expected to reach 980 million units, an increase of approximately 200 million units from 773 million units in 2023. The small OLED market is expected to exceed 1 billion units in 2025.

Looking at the 2024 performance, most panel manufacturers in Korea and China saw an increase in shipments of 40 to 50 million units, and in particular, Chinese panel manufacturers TCL CSOT, Tianma, Visionox, and Everdisplay saw shipments increase by more than 50% compared to 2023. BOE, China’s largest panel manufacturer, saw its panel shipments increase by only about 8% due to temporary production suspensions caused by disruptions in iPhone supplies throughout the year.

Not only Chinese panel makers, but also Korean panel makers have seen a significant increase in shipments. As rigid OLED panels began to be applied to Samsung Electronics’ Galaxy A series, Samsung Display’s shipments are expected to surge from 320 million units in 2023 to 380 million units in 2024. LG Display’s smartphone OLED shipments also increased from 52 million units in 2023 to 68 million units in 2024 as its supply of panels for iPhones expanded.

With Chinese panel makers’ shipments steadily increasing, and Samsung Display’s rigid OLED shipments and LG Display’s iPhone panel shipments also increasing, small OLED shipments in 2025 are expected to easily exceed 1 billion units.

“OLEDs are being widely applied to lower-end models of Samsung Electronics’ Galaxy A series and low-cost models from Chinese set manufacturers, and BOE and Visionox’s new 8.6G lines are also designed to produce panels for smartphones, so small-sized OLED shipments are expected to continue to rise for the time being,” said Han Chang-wook, Vice President of UBI Research.

Chang Wook HAN, VP/Analyst, UBI Research(cwhan@ubiresearch.com)

We will introduce the contents of the “2025 Automotive Display Technology and Industry Trends Analysis Report” published by UBI Research in February 2025 as a series. As the first series, we will introduce Panoramic-HUD, which is included in the report.

Generally, automotive head up displays are projected on the windshield, the windshield of a car, and the driver can see a virtual image generated several meters away. Unlike general HUDs, Panoramic HUDs directly reflect the image projected from the display onto a black film coated on the lower surface of the windshield, but they are classified as HUDs because they allow the driver to maintain a head-up view while driving.

Panoramic HUDs are implemented using a direct image method, so their design is simple and the system cost is low. This reduces manufacturing costs while enabling the digital experience of premium vehicles. In addition, P-HUDs have the advantage of being able to use polarized sunglasses that prevent glare because they reflect p-polarization. Therefore, it is expected that panoramic HUDs will enter the market before AR-HUDs become widespread. At this year’s CES, several companies announced Panoramic HUDs, reminiscent of the P-HUD competition arena. BMW calls its panoramic HUD “Panoramic Vision” and announced that it will be installed in the Neue Klass model to be released from 2025. It uses TFT-LCD and has a brightness of about 5,000nits, but higher brightness is needed to improve outdoor visibility, and for this purpose, it is working closely with e-LEAD, a Taiwanese company that manufactures black films.

(Source: BMW)

BOE introduced a P-HUD with a brightness of 5,000nits (normal) / 7,000nits (10% peak) by applying a 44.8-inch oxide TFT-LCD panel and 2,850 zone local dimming, and polarized sunglasses can be used because the P-polarization reflectance is 25%.

TCL-CSOT introduced a P-HUD with a brightness of 11,000 nit by applying three 11.98-inch TFT-LCD panels and 384 zone local dimming.

CarUX, a subsidiary established by Innolux in 2019, introduced a 48-inch P-HUD and boasted a high brightness of 14,000 nit by using a micro-LED panel.

Hyundai Mobis introduced a transparent P-HUD with a transmittance of 95% by introducing holographic technology from Zeiss in Germany, and plans to mass produce it in 2027. Continental also introduced the “Scenic View HUD,” a panoramic HUD with three TFT-LCD panels and local dimming, in 2023, and plans to release it in 2026.

Since the P-HUD is located in the vent, heating, ventilation, and air conditioning hardware must be rearranged, and heat dissipation issues must be resolved, so there are many issues to be resolved in addition to the display, so it took a long time, but 2025 is expected to be the first year of the P-HUD release.

This report covers the overall trends of vehicle display technology, including HUD, as well as the status of display development and vehicle application by finished vehicles, electrical equipment manufacturers, and panel manufacturers. If you are involved in the automobile and display industries, now is an important time to analyze market trends and prepare future strategies. We hope that you will gain insight one step ahead through this report so that you can understand the future trends of the vehicle display market in advance and proactively respond to industry changes.

UBI Research Chang Wook HAN Analyst(cwhan@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report Sample

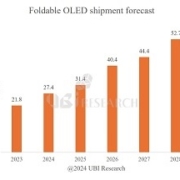

Foldable OLED shipment forecast

According to the ‘2024 Small OLED Display Annual Report’ recently published by UBI Research, OLED shipments for foldable phones are expected to increase from 27.4 million units in 2024 to 52.7 million units in 2028.

According to the report, Samsung Display’s OLED shipments for foldable phones in 2023 will be 13.4 million units, a 6.3% increase from 12.6 million units in 2022. Also, among Chinese panel makers, BOE shipped 6.2 million units of OLED for foldable phones, more than three times the 1.9 million units in 2022, while TCL CSOT and Visionox each shipped 1.1 million units of OLED for foldable phones.

Although there is fierce pursuit by Chinese companies, Samsung Display is expected to still take the lead in the foldable phone market. Samsung Electronics, to which Samsung Display supplies panels, is expected to expand the models of the Galaxy Fold series scheduled to be released this year, and Samsung Display’s foldable phone panels are expected to be applied first to Apple’s foldable iPhone to be released in the future. Based on such technological prowess and competitiveness, Samsung Display’s dominance in the foldable phone market is expected to continue for the time being.

Foldable OLED shipment ratio forecast

According to the ‘2023 Small OLED Display Annual Report’ recently published by UBI Research, Samsung Display’s OLED shipments for foldable phones are expected to reach 50.9 million units in 2027 with an average annual growth rate of 28.1% from 18.9 million units in 2023.

According to the report, Samsung Display’s foldable OLED shipments in 2022 were analyzed to be 12.6 million units, accounting for 85.1% of global foldable OLED shipments in 2022. BOE, TCL CSOT, and Visionox mass-produced some foldable OLEDs, but Samsung Display led the foldable OLED market.

It is expected that Samsung Display will continue to dominate the foldable OLED market in the future. It seems difficult for TCL CSOT and Visionox to record annual shipments of more than 1 million units by 2027, and unless LG Display also secures a customer, the time for mass production of foldable phone panels is unclear.