Commercialization Strategies for Micro LED Products by Chinese Companies

The Chinese display industry is accelerating its efforts to secure global leadership in the micro-LED market, which is seen as its next major growth area. An analysis of the moves made by Chinese companies at ICDT 2026 reveals that they are pursuing distinct mass-production strategies centered on two key areas: “ultra-large TVs” and “automotive displays.”

• BOE & Vistar: Leading the Ultra-Large and Premium Markets

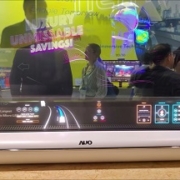

BOE and Vistar are prioritizing the commercial display and premium TV markets, focusing on the “ease of scaling up”—the greatest advantage of micro-LED technology. Vistar has swiftly launched a mass production system for large-sized micro-LEDs. By moving beyond technology demonstrations and entering a mass production phase that generates revenue, the company is establishing itself as a “first mover” in China. BOE demonstrated its leadership in ultra-large-screen technology by unveiling an 81-inch ultra-thin HDR TV at ICDT 2026, leveraging its accumulated COG (Chip on Glass) technology. By setting a new standard for the ultra-large, ultra-high-definition market—a segment where LCD and OLED struggle to compete—the company appears to be focusing on ensuring the stability of mass production for large-sized micro-LED panels.

• TCL CSOT vs. Tianma: Strategic Market Approaches

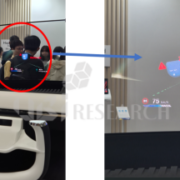

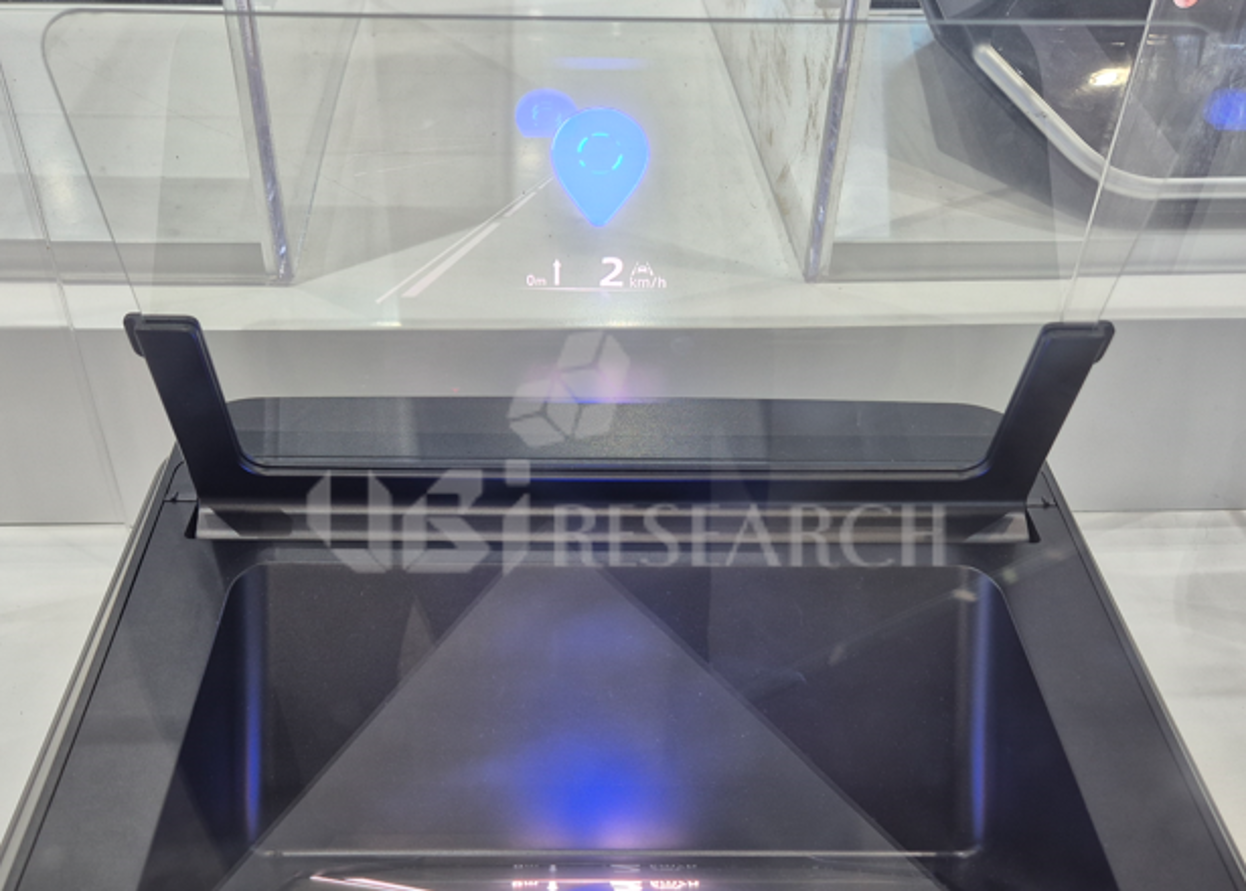

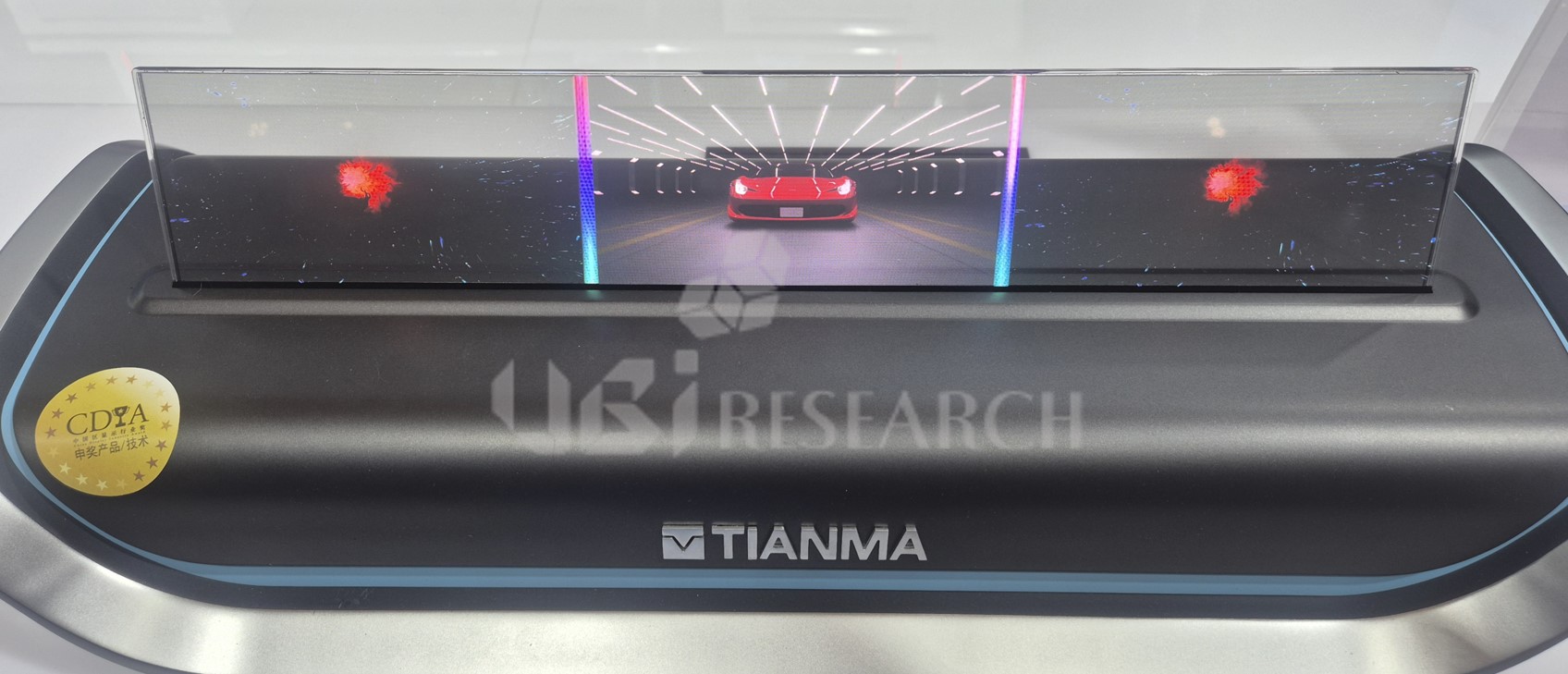

The two companies, which have recently been the most active in terms of investments and technology announcements, are pursuing distinctly different paths, ranging from investment structures to mass production goals. TCL CSOT has opted for a joint venture with Sanan, a company specializing in LED chips. By vertically integrating its supply chain—from chips to panels—it is diversifying technical risks and enhancing the precision of its verification processes. It is rigorously validating its technology on a 2.5G R&D line. At ICDT2026, the company is exhibiting a 14.3-inch ultra-high-brightness (panel brightness: 45,000 nits) P-HUD display and a 4.6-inch AR-HUD, and is developing technologies to prepare for the next-generation automotive display market. It is placing emphasis on “scalability,” which involves transitioning to large glass substrates after undergoing small-scale trial production. Another notable point is that, following SID2025, the company also exhibited additional monochrome 0.05-inch and single-chip full-color silicon-based 0.28-inch Micro LED products at ICDT2026. In the Micro LED sector, the company is pursuing two business lines: glass substrates and silicon substrates.

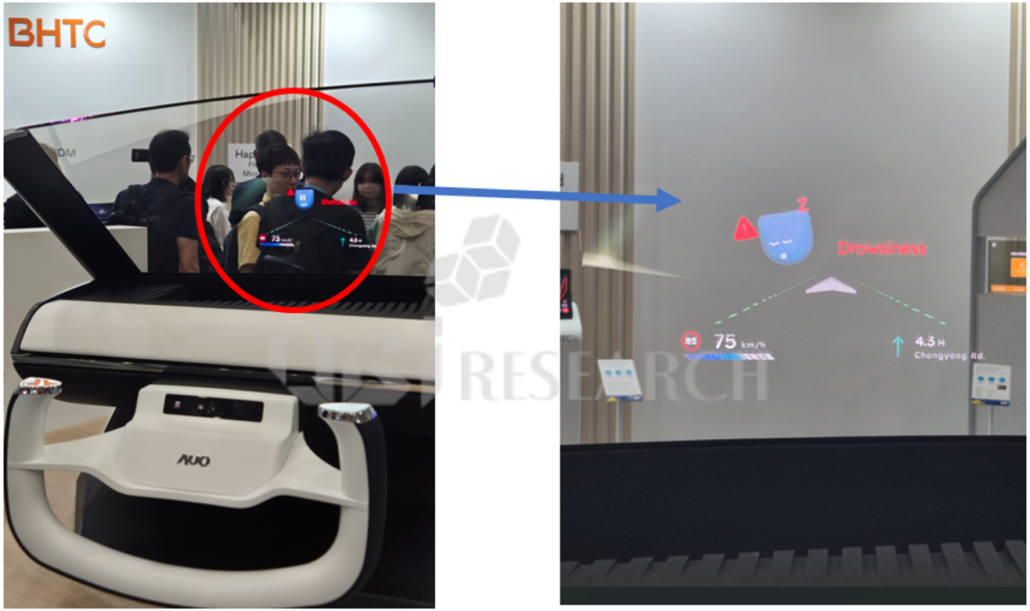

A 4.6-inch Micro-LED AR-HUD showcased at ICDT 2026. Boasting a perceived brightness of over 18,000 nits, it targets the next-generation automotive market as the world’s brightest display in its class. (Source: UBI Research)

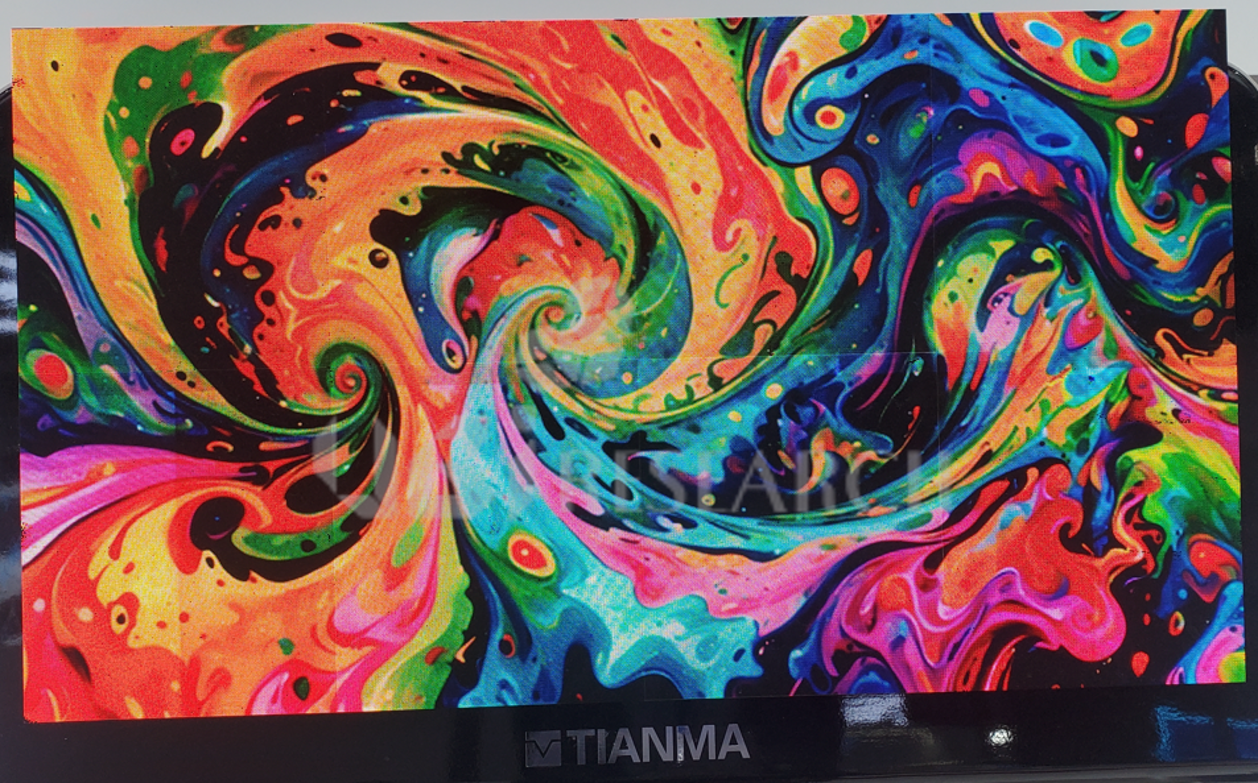

A 27-inch seamless tiling Micro-LED display revealed at ICDT 2026. Achieving a brightness of over 1,500 nits and a tiling gap of less than 20μm, it demonstrated its competitiveness in the commercial display market. (Source: UBI Research)

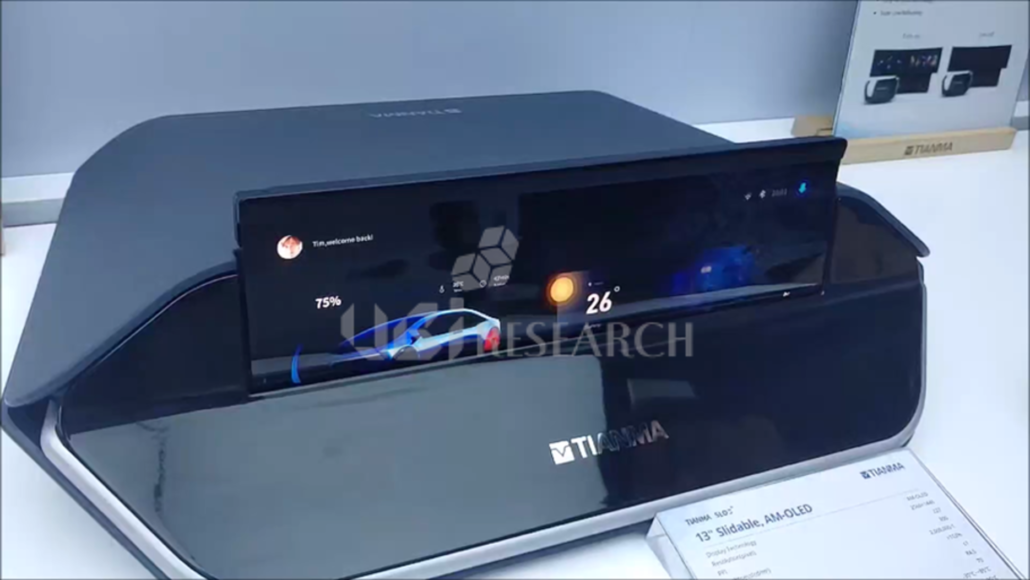

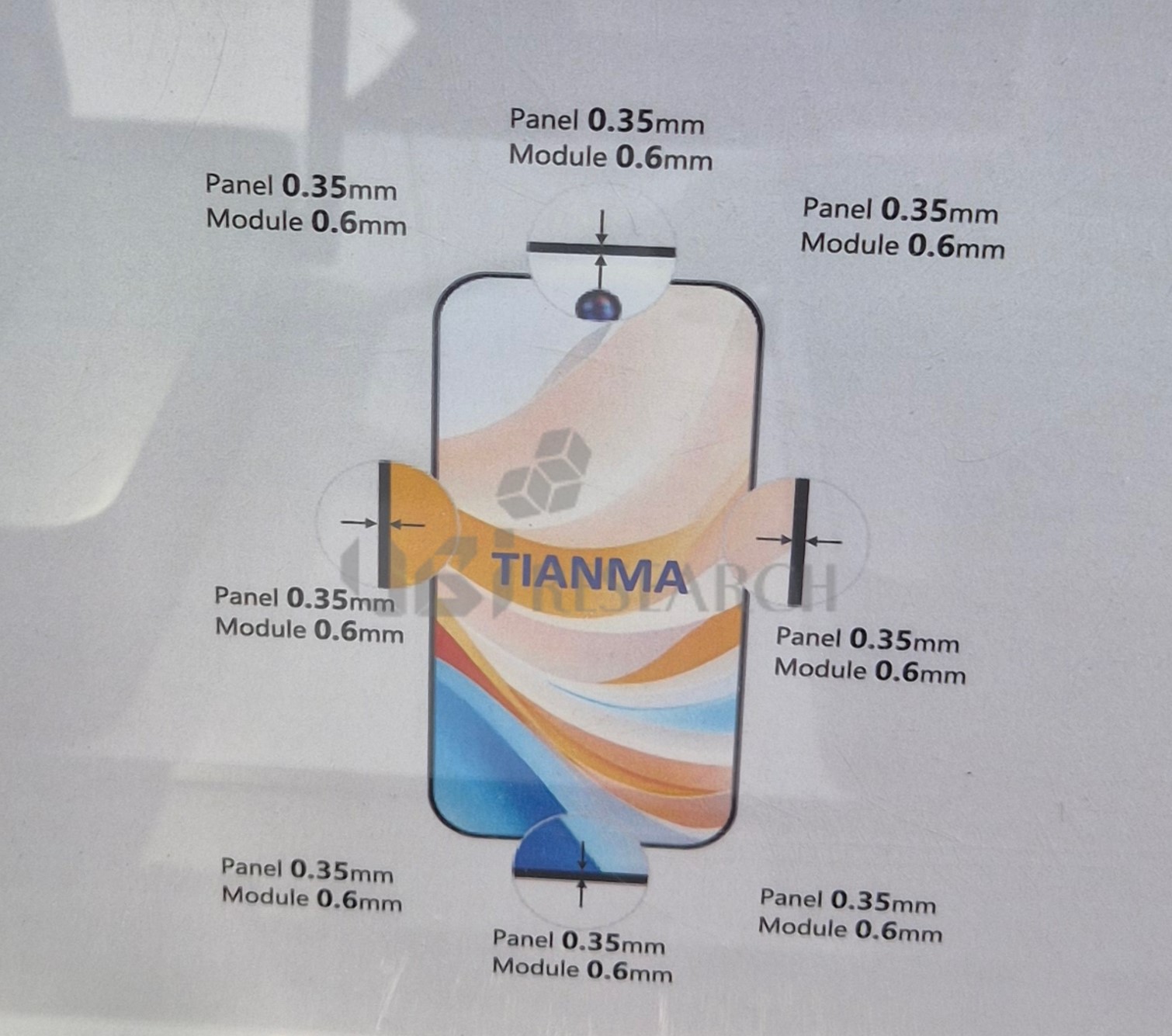

In contrast, Tianma has built a dedicated 3.5G production line using 100% internal capital. This approach is characterized by reduced reliance on external partners and the creation of an independent technology ecosystem, which has accelerated decision-making. The company is pursuing immediate commercialization alongside technology validation. Its strategy is to quickly supply products to high-margin, standardized markets—such as automotive HUDs and commercial displays—via its 3.5G line to secure market share early on.

Chinese companies appear to be moving beyond the technology development phase and entering a competition centered on “who can first meet customer requirements in terms of yield and unit price.” This is because, in the early market, the first company to supply products to customers gains a significant first-mover advantage. Since Micro-LED manufacturing technology has not yet fully matured, the results of trial production, yield rates, and the speed at which productivity is secured this year and next are expected to be a turning point that determines the future direction of the Micro-LED display market. UBI Research has published a Micro-LED report analyzing the technological trends of products developed by Micro-LED-related companies in China and Taiwan, and continues to conduct ongoing analysis and updates.

Namdeog Kim, Senior Analyst at UBI Research (ndkim@ubiresearch.com)

101 inch Micro-LED Set BOM Cost Analysis For TVs

101 inch Micro-LED Set BOM Cost Analysis For TVs

Industry Trends and Technology of Micro-LED Displays for XR Report

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

China Trends Report Inquiry

China Trends Report Inquiry