The Premium TV Market Enters the Era of Price Competition Between OLED and Mini LED

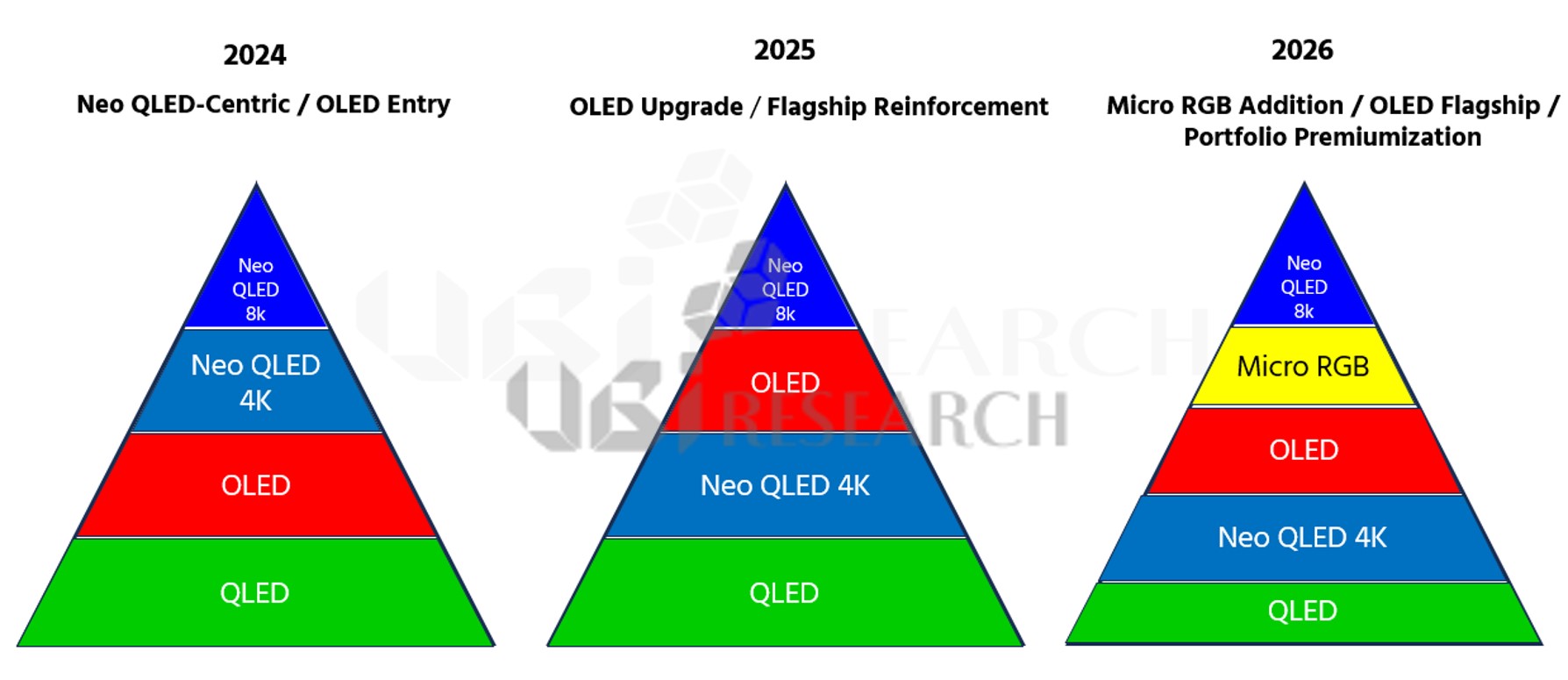

Samsung Electronics is accelerating its strategic transition by redefining OLED as the clear flagship axis in its TV portfolio. Until 2024, OLED was introduced only in limited lineups within a premium volume strategy centered on Neo QLED. However, in 2025, OLED was elevated to the upper-tier lineup, strengthening its role as a flagship. In 2026, while adding Micro RGB as an ultra-premium category, Samsung continues to position OLED as a core pillar. This shift indicates a clear transition from LCD-based advancement to a self-emissive display-centric strategy.

Samsung’s TV technology portfolio shift. Moving from a Neo QLED-centric strategy in 2024, OLED is elevated in 2025, and Micro RGB is added to the top tier in 2026, marking a transition toward self-emissive displays. (Source: UBI Research)

The pricing structure is also changing rapidly. OLED TVs have historically maintained a price premium of around 30–40% over Mini LED TVs, but this gap is expected to narrow significantly with LG Display’s SE OLED strategy gaining traction. If SE OLED TV prices for 65-inch models are formed at around $1,300, the gap with Mini LED TVs from TCL and Hisense (approximately $1,100–$1,200) could shrink to just 5–10%. As a result, the premium TV market is moving from a technology-driven competition—“OLED vs. Mini LED”—to a direct head-to-head battle where price differences are minimal from the consumer’s perspective.

In this context, the adoption of LG Display’s SE OLED panels by major set makers such as LG Electronics, Samsung Electronics, and Panasonic is particularly significant. It suggests that OLED is no longer confined to brand-specific differentiation but is evolving into a broader industry platform across the premium TV segment. Samsung, in particular, is maintaining its QD-OLED strategy while simultaneously expanding its OLED positioning to support market growth. Consequently, OLED is transitioning from an ultra-premium niche into the mainstream premium segment.

Meanwhile, the Mini LED camp remains highly competitive. Chinese manufacturers such as TCL and Hisense are aggressively expanding their presence in the premium segment by leveraging high brightness, larger screen sizes, and strong price competitiveness. As a result, the market is shifting from a simple competition in display performance to a more complex battle involving price-to-performance, brand positioning, and perceived consumer value. As the price gap narrows to single digits, OLED’s advantages in contrast and design will compete directly with Mini LED’s strengths in brightness and affordability.

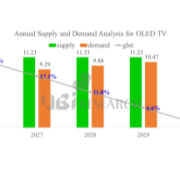

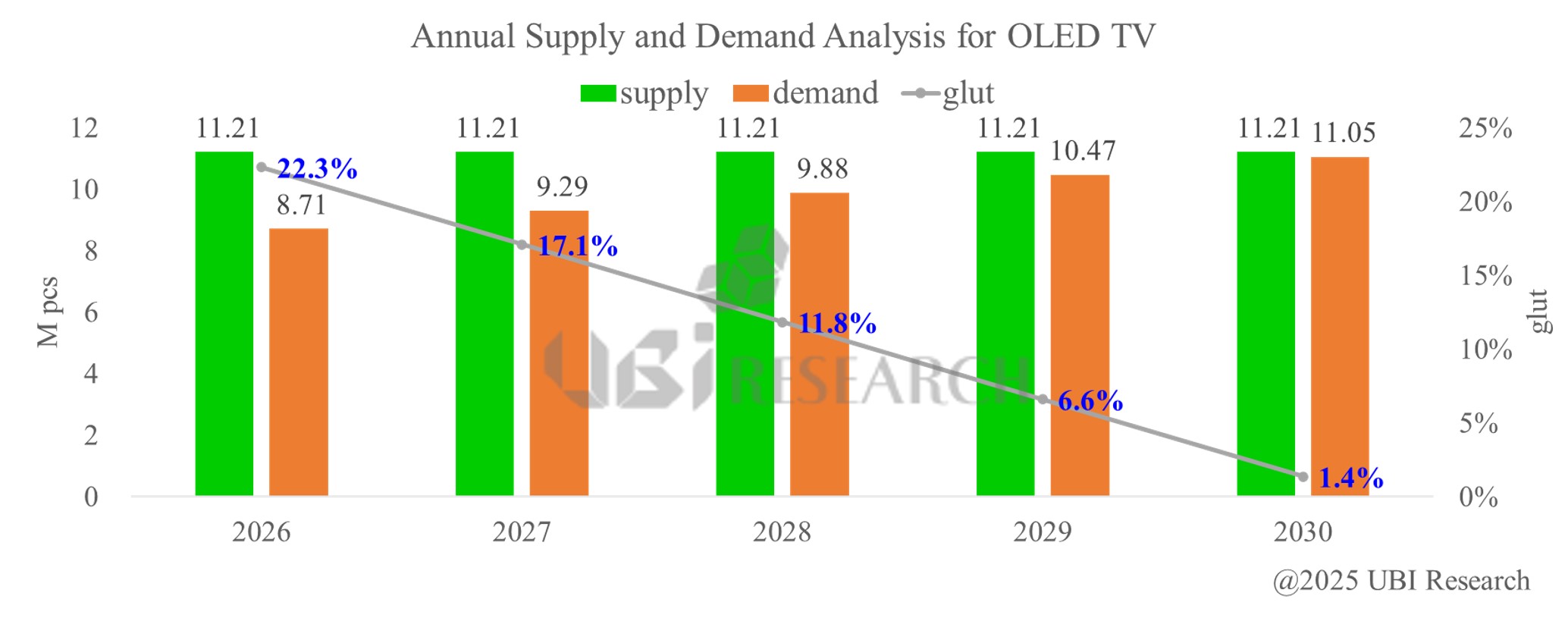

On the supply side, the need for additional investment is becoming increasingly evident. As OLED TV shipments continue to grow and more production capacity is allocated to OLED monitors on the same lines, available capacity is tightening rapidly. According to the data, supply headroom is projected to decline from 22.3% in 2026 to 17.1% in 2027, 11.8% in 2028, 6.6% in 2029, and just 1.4% by 2030. This suggests that supply capacity will be nearly fully utilized around 2030, highlighting the necessity of preemptive capacity expansion to sustain the growth of the OLED TV market.

Annual supply and demand analysis for OLED TV. Due to rising demand and expanded production of monitor OLEDs, the supply glut is forecast to drop sharply from 22.3% in 2026 to just 1.4% by 2030. (Source: UBI Research)

Changwook Han, Executive Vice President at UBI Research, stated, “The premium TV market is shifting beyond a technology competition between OLED and Mini LED into a price-driven competition, with cost reduction through SE OLED emerging as a key driver for market expansion.” He added, “As adoption by major set makers increases while supply headroom tightens, the competitiveness of OLED will increasingly depend on price stabilization and the timely expansion of production capacity.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

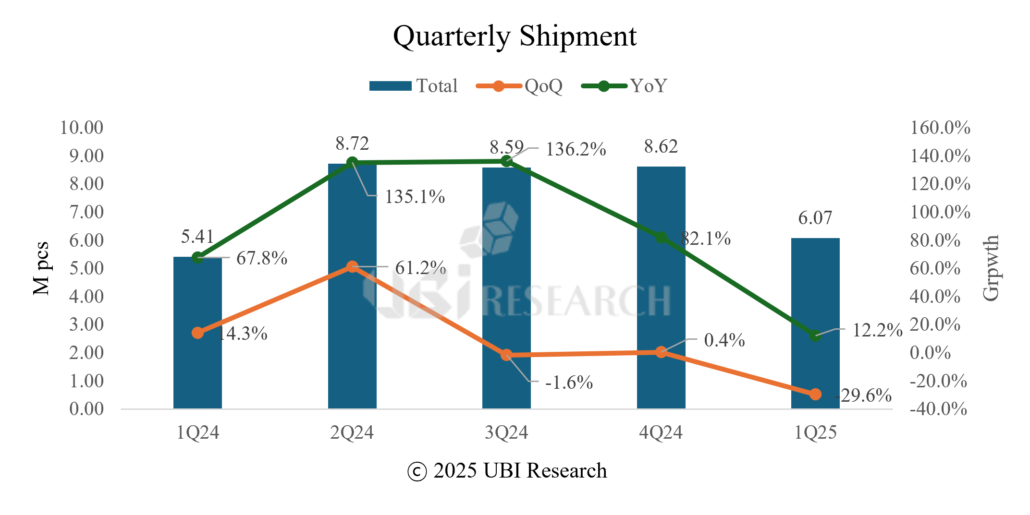

Quarterly Small OLED Display Market Tracker Sample

Quarterly Small OLED Display Market Tracker Sample

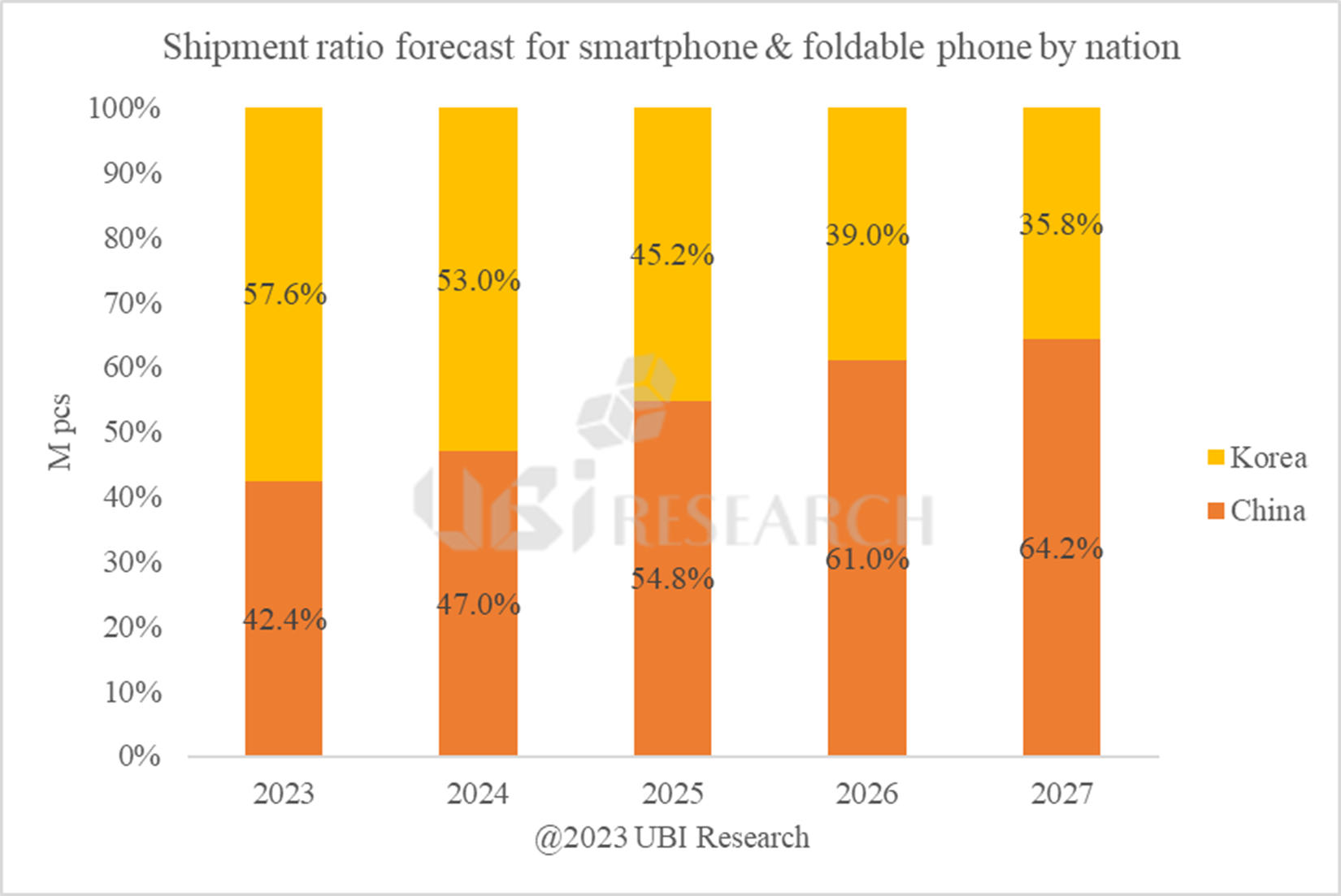

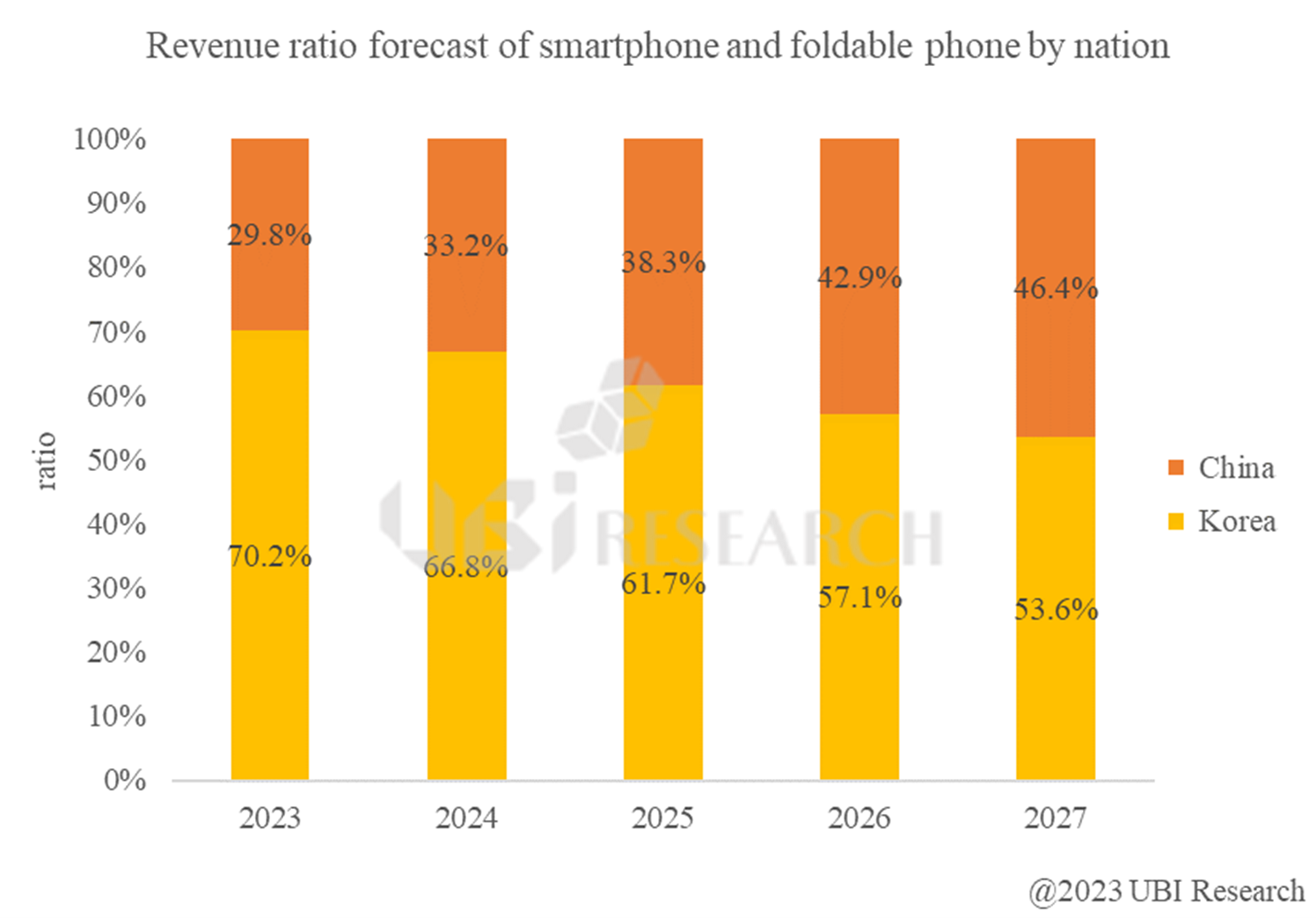

Quarterly Medium & Large OLED Display Market Tracker Sample

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.