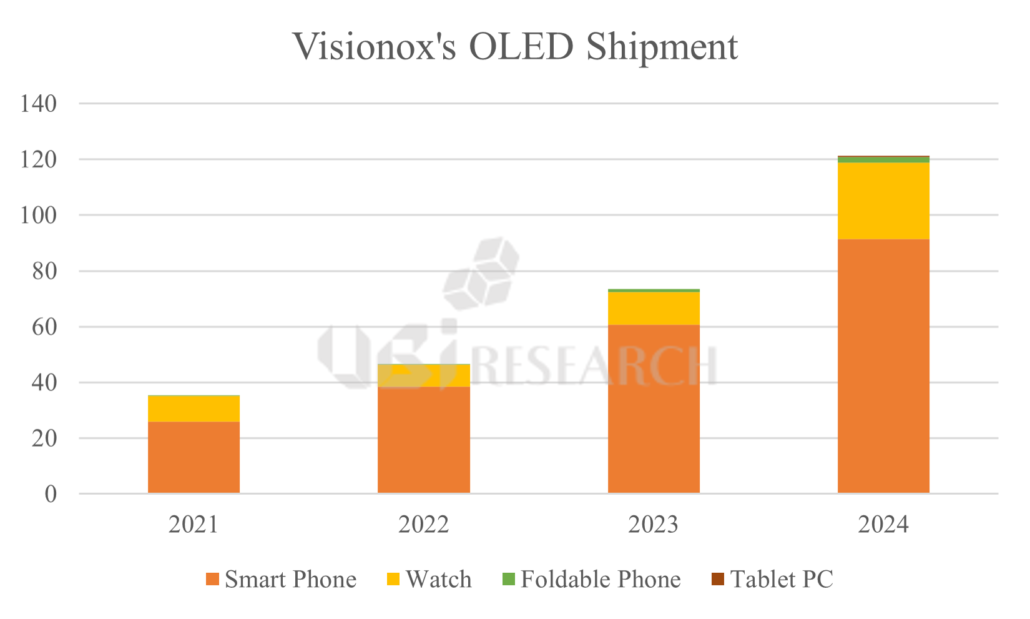

OLED panel for smartwatches using ViP deposition method unveiled by Visionox

Chinese display specialist Visionox showcased products manufactured using its ViP (Visionox Intelligent Pixelization) technology at the DIC 2025 (Display Innovation China) exhibition held in August 2025. ViP is Visionox’s next-generation core technology, enabling ultra-high resolution, improved device lifetime, and high brightness—representing performance enhancements across multiple dimensions.

At the exhibition, Visionox revealed that panels produced with the ViP method offer a resolution of up to 1700 ppi, an aperture ratio of 69%, a sixfold improvement in device lifetime, and four times higher brightness compared to conventional technologies. The company emphasized that this technology is widely applicable—from AR/VR microdisplays to smartphones, automotive displays, and large-sized TV panels.

A Visionox representative at the exhibition stated, “Among the panels produced using the ViP method on our V3 line, small-sized display panels such as those for smartwatches have achieved yields of over 90%. Yields for medium-sized displays, such as those for smartphones, have also reached around 60%.”

However, since the ViP deposition method is applied to 8.6-generation medium-to-large OLED production lines, the technical difficulty of yield improvement increases with larger substrate sizes. Therefore, further monitoring of yield stabilization will be necessary going forward.

The ViP deposition method is compatible with both regular and irregular panel structures, supports low minimum order quantities, and is compatible with pol-less and transparent display technologies. As such, it is considered well-suited for high-mix, low-volume production and customized display markets.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

At SID 2025, Samsung Display unveiled its Sensor OLED technology that enables both biometric authentication and cardiovascular data monitoring on a single OLED screen.

Source: Samsung Display, SID 2025 Digest (Paper 80-1)

Display technology is evolving yet again. They’ve gone beyond just displaying images to detecting and analyzing vital signs and even diagnosing your health. Samsung Display’s paper “Sensor OLED Display-Based Mobile Cardiovascular Health Monitor” (SID 2025 Digest, Paper 80-1), presented at SID 2025, symbolizes this change. The paper introduces Sensor OLED technology, which integrates organic photodiodes (OPDs) into OLED displays at high resolution and down to the pixel level, and demonstrates the potential for smartphones to evolve into cardiovascular disease monitors and digital treatment platforms.

Traditionally, measuring biometric data has required the use of separate wearable devices or standalone sensors, but Sensor OLED is designed to simultaneously collect high-resolution image sensing and photoplethysmography (PPG) signals on the display itself, enabling fast and precise measurement of a variety of vital signs with the simple act of placing a finger on the smartphone display. It can simultaneously measure PPG signals from the left and right fingers and compare the features of the pulse waveforms to screen for cardiovascular disease with 90% accuracy, according to the paper. This method achieves similar levels of accuracy to Doppler or sphygmomanometers used in healthcare organizations but offers greater convenience in that it does not require a hospital visit or wearing any equipment.

The paper specifically focuses on the cuffless blood pressure measurement algorithm, which compares a single-point method that utilizes PPG signals from a single finger to a dual-point method that analyzes signals from both fingers together, demonstrating that both accuracy and reliability can be achieved. In a clinical trial involving 120 people and a four-week follow-up, medical device-level accuracy was achieved, and the signal loss rate was significantly reduced. As such, sensor OLED-based smartphones are expanding into mobile healthcare platforms that can analyze blood pressure, heart rate, stress, respiration rate, and even vascular structure and blood flow.

The best feature of sensor OLEDs is the interactive sensing experience. While measuring vital signs, the signal quality can be checked in real time, and users can adjust finger position or pressure on the screen to improve data accuracy. The paper defines this as ‘User Interactive Sensing’ and emphasizes its potential to evolve into a device-based solution that can replace existing complex biofeedback devices. High-resolution image-based blood flow analysis also makes it possible to visualize and measure the structure and flow of blood vessels in the finger. This technology paves the way for smartphones to replace existing hospital Doppler machines.

As such, sensor OLEDs are gaining traction as a key platform for next-generation smartphones and wearable devices because they can integrate displays and sensors into a single device, dramatically improving measurement performance while reducing the thickness and complexity of the device. In particular, its convergence with artificial intelligence (AI) and Internet of Things (IoT) technologies can be linked to a variety of digital therapeutics (DTx) services, including personalized health monitoring, early disease prediction, and telemedicine.

In the paper, the research team said that the technology is not just a technical experiment but has achieved medical device-level reliability in real-world clinical environments and has the potential for commercialization through large-scale clinical validation. This is expected to enable basic health care in areas where it is difficult to visit a hospital or where medical infrastructure is lacking.

Changho Noh, Analyst at UBI Research (chnoh@ubiresearch.com)

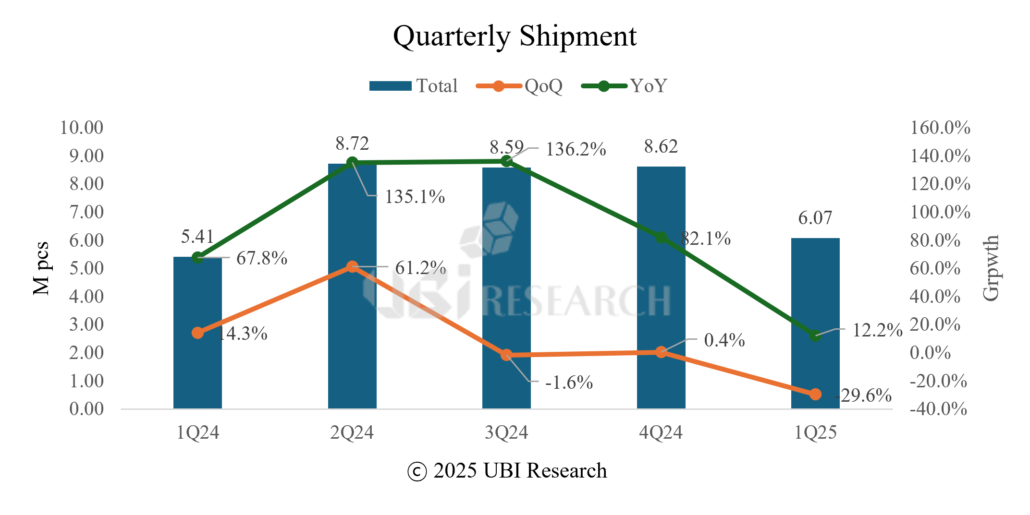

Samsung Display’s OLED panel shipments from 1Q24 to 2Q25

Samsung Display saw a significant increase in Mid-large area OLED panel shipments during the second quarter. According to UBI Research’s quarterly publication, OLED Display Market Tracker, the company shipped a total of 4.9 million large-area OLED panels in Q2 2025, marking a 58.2% rise from 3.1 million units in the first quarter.

By product category, OLED panel shipments for notebooks reached 2.5 million units, representing the largest share and more than double the volume of the previous quarter. UBI Research forecasts continued growth in notebook OLED shipments in the second half of the year, with total shipments in 2025 expected to reach around 10 million units. Furthermore, starting in 2026, Samsung Display is set to supply 2-stack tandem OLED panels for Apple’s MacBook Pro series, which is projected to drive notebook OLED shipments to over 15 million units annually.

OLED panel shipments for monitors also showed solid growth. Q2 shipments were estimated at 700,000 units, up approximately 44% from the first quarter. The annual shipment volume for 2025 is projected to reach about 2.5 million units.

In addition to notebooks and monitors, shipments of OLED panels for automotive displays, tablet PCs, and TVs remained similar to Q1 levels, with slight increases observed.

Chang Wook Han, Executive Vice President of UBI Research, commented, “Samsung Display experienced a temporary decline in shipments during Q1 due to reduced demand for tablet PC and notebook panels, but recovered to typical levels in Q2. From Q3 onward, panel shipments for the new iPad Pro models and notebook panels for DHL are expected to increase, further boosting Samsung Display’s shipment volume in the third and fourth quarters.”

Samsung Display is actively strengthening its presence in the large-area OLED market, accelerating business expansion across various sectors including notebooks, monitors, tablets, and automotive applications. Industry observers expect this trend to become a key growth driver for the overall OLED market.

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Chinese display maker BOE has reportedly cleared Apple’s qualification (Qual) process for producing OLED panels for the iPhone 17 Pro. Industry insiders had initially predicted that BOE would struggle to obtain approval for the premium model’s panels within this year, but the faster-than-expected qualification suggests the company is strengthening its readiness for Apple’s 2025 lineup.

While BOE has received panel-level qualification, it has yet to pass the module qualification stage. Nevertheless, the company is expected to begin risk production of iPhone 17 Pro panels as early as August. These early batches are believed to be for verification or initial delivery purposes.

With this additional qualification, BOE’s total shipment forecast for iPhone OLED panels in 2025 has been revised upward from 40 million units to approximately 45 million units, reflecting the newly approved volume for the iPhone 17 Pro.

BOE is currently operating its B11 facility in Mianyang, Sichuan Province, as a dedicated OLED production line for iPhones. The company has configured six module lines in total: two lines for iPhone 14 and 16e, two for iPhone 16, and two verification lines for the iPhone 17 Pro. Given the high complexity and stringent quality standards required for the Pro model, securing stable yield rates will be a key challenge moving forward.

Clearing this qualification marks a significant step for BOE toward entering Apple’s premium lineup in earnest. It also adds competitive pressure to the current iPhone OLED panel supply structure, which is largely dominated by Samsung Display and LG Display. However, since BOE has not yet secured module-level qualification, additional verification and technical stabilization will be necessary before full-scale deliveries can begin.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

As digitalization accelerates in the automotive industry, the sophistication of in-vehicle displays is accelerating. OLED displays, in particular, are rapidly being adopted, particularly in premium vehicles, due to their superior image quality and flexible design possibilities.

The first automotive application of OLED displays was the instrument clusters of the 2016 Audi TT RS and Q7. These vehicles featured OLED panels supplied by Samsung Display, leading to the early commercialization of digital clusters. Following this, the 2017 Cadillac Escala concept car featured LG Display’s curved OLED display in its instrument cluster, demonstrating the potential of OLED in luxury vehicles.

OLEDs were first commercialized in the central information display (CID) with the 2021 Mercedes-Benz S-Class. This vehicle features a 12.8-inch vertical OLED touchscreen, which integrates with haptic feedback and Mercedes-Benz’s next-generation infotainment system, MBUX 2nd Generation, significantly enhancing the passenger experience. The 2022 EQS and EQS SUV will then see the introduction of the ‘MBUX Hyperscreen’, which integrates a 17.7-inch central OLED and a 12.3-inch passenger OLED under a curved glass panel.

Mercedes-Benz S-Class (12.8-inch OLED CID)

MBUX Hyperscreen (17.7-inch OLED CID, 12.3-inch OLED CDD)

Amidst this trend, LG Display was the first company to establish a mass production system for automotive OLEDs, steadily supplying OLED panels to various brands, including Mercedes-Benz. Notably, LGD has established itself as a key partner for Mercedes-Benz, leading the premium display market for its electric vehicle lineup, including the EQS and EQE.

Meanwhile, Samsung Display is actively expanding its supply of next-generation automotive OLED panels. Specifically, it plans to supply a 48-inch “pillar-to-pillar” OLED display for the 2028 Mercedes-Maybach S-Class, as well as future CLA, SL, and electric vehicle lineups. This display, with its integrated structure spanning the entire front of the vehicle, is attracting attention for its ability to deliver both immersive and design perfection.

Despite the high cost and limited supplier base compared to LCD, OLED is becoming a key element in providing differentiated user experiences and strengthening brand identity for luxury brands such as Mercedes-Benz, BMW, Genesis, Lucid, and BYD. “Automotive OLED panel shipments are expected to reach approximately 3 million units in 2025, and by 2030, they are expected to exceed 6 million units, accounting for 14.4% of the total automotive display market in terms of value,” said Changwook Han, Executive Vice President of UBI Research. “This demonstrates that in-car displays are evolving beyond a simple means of conveying information to become the center of UX that provides emotion and immersion.”

Changwook HAN, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report

2025 Automotive Display Technology and Industry Trends Analysis Report

Westlake Smokey Mountain Technology (WSMT), headquartered in Hangzhou, China, has recently successfully attracted a pre-series A investment of approximately RMB 100 million (approximately US$14 million). The investment was made by Shenzhen Capital Group (SCGC), Ivy Capital, Moganshan Fund, Lenovo Capital & Incubator Group, and others, suggesting that WSMT has entered into full-scale preparations for Micro-LED mass production.

WSMT is a company developing Micro-LEDs with a vertically stacked structure of RGB elements based on technology from Westlake University (Westlake University). Unlike the conventional RGB separated structure, this technology vertically stacks red (R), green (G), and blue (B) LEDs on a single chip, fundamentally solving the problem of pixel alignment accuracy, and is regarded as an advantageous structure for realizing high-resolution small displays.

The company is currently building an epi-wafer production line for Micro-LEDs in Huzhou, Zhejiang Province, which is expected to be in production by the end of 2025.WSMT emphasizes that this technology will enable ultra-high resolution of over 5,000dpi, a lifetime of over 100,000 hours, low power (<50mW, 10K nits standard) The company emphasizes that this technology can be used not only for microdisplays for AR/VR, but also for scalability of large-area displays of 8 inches or larger.

At the same time, Jade Bird Display (JBD), located in Shenzhen, China, also started sample shipments of its “Phoenix series” of RGB vertically stacked micro-LED microdisplays. ㎛JBD also plans to mass produce 0.3-inch, 4K resolution products by the end of 2025.

JBD has until recently secured tens of millions of dollars in funding through the A4 strategic investment round and A3 round, with major global companies such as Alibaba, Samsung, BYD, and Geely as major investors. In particular, JBD is working with BYD on the joint development of Micro-LED displays for vehicles. Currently, JBD is operating a $92 million mass production line in Hefei with a total capacity of 120 million 0.13-inch panels per year.

WSMT and JBD are both developing Micro-LED technology based on the vertically stacked RGB structure, but WSMT, as a research-oriented startup, is emphasizing the perfection of the technology and the potential for large-area deployment, while JBD is securing an advantage in terms of commercialization and speed of market entry.

The competition between WSMT and JBD is part of China’s strategy to secure technology leadership in the global MicroLED ecosystem. The competition between WSMT and JBD can be interpreted as part of China’s strategy to secure technology leadership in the global MicroLED ecosystem, and is expected to influence the strategic choices of Apple, Meta, Samsung Electronics, and others in the future.

Joohan Kim, Analyst at UBI Research (joohanus@ubiresearch.com)

Flex Magic Pixel™ at MWC (Mobile World Congress) 2024

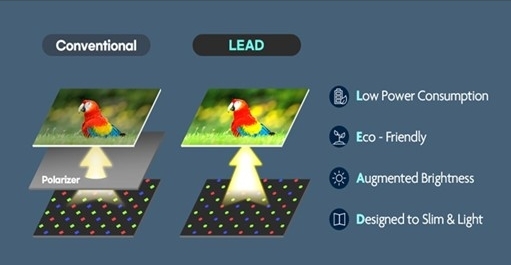

Samsung Display is expected to introduce Flex Magic Pixel™, a revolutionary viewing angle adjustment technology, to its next flagship smart device, bringing a new level of user privacy experience. Through synergies with Samsung Display’s core OLED technology, CoE (Color filter on Encapsulation), this technology is expected to secure even stronger competitiveness.

‘Flex Magic Pixel’ first garnered significant attention from the industry at the MWC (Mobile World Congress) 2024 exhibition. This proprietary Samsung Display technology combines artificial intelligence (AI) to dynamically control the display’s viewing angle. When a user runs sensitive applications like banking apps, the AI recognizes this and automatically adjusts the screen to be clearly visible only from a direct frontal view. From side angles, the screen appears blurry or invisible, effectively preventing the leakage of personal information.

Traditional privacy films, attached to the display, typically suffer from reduced screen brightness and degraded picture quality. Their fixed viewing angles also limit user convenience, and their thickness can restrict design flexibility. ‘Flex Magic Pixel,’ however, fundamentally resolves these issues. ‘Flex Magic Pixel’ is not merely a film technology that blocks light from certain angles, but a sophisticated technology that controls the viewing angle through precise manipulation of individual OLED pixels. This ensures users can experience top-tier picture quality while their privacy remains protected.

Furthermore, ‘Flex Magic Pixel’ maximizes its synergy when combined with Samsung Display’s OLED CoE technology. CoE technology removes the conventional polarizer from OLED panels and directly forms a color filter on the encapsulation layer. This dramatically reduces display thickness and enhances light transmittance, delivering exceptional brightness and superior power efficiency.

The high brightness and flexibility achieved with CoE technology are expected to have a positive impact on the functionality of Flex Magic Pixel. The high-bright screen based on CoE compensates for the slight light loss that may occur when Flex Magic Pixel is activated, enabling perfect privacy protection even in next-generation form factors such as foldable and rollable devices.

The combination of Flex Magic Pixel and CoE technology enables users to use smart devices with confidence anytime, anywhere, while providing overwhelming picture quality and design flexibility, and is expected to be expanded to next-generation displays such as automotive displays and IT devices.

The future application of ‘Flex Magic Pixel’ will once again demonstrate Samsung Display’s technology leadership in satisfying user convenience and security at the same time and is expected to set a new direction for the future display market.

Changho Noh, Analyst at UBI Research (chnoh@ubiresearch.com)

HKC, one of China’s leading display panel manufacturers, is accelerating its transition into the small- and medium-sized OLED market. Moving beyond its traditional focus on large-sized LCDs, the company is now expanding into flexible OLED panels for smartphones and IT devices, while also actively investing in next-generation maskless OLED fabrication technologies.

HKC plans to begin trial production of smartphone OLED panels at its H6 facility in July 2025. The Phase 1 line has been built using secondhand 5.5-generation equipment previously owned by Royole, and features a hybrid structure that applies flexible encapsulation on glass substrates. The TFT backplane has a monthly capacity of 4,000 substrates, and the evaporation process follows a quarter-cut method.

In Phase 2, HKC is incorporating 4.5-generation EVEN equipment transferred from Japan’s Sharp, which is expected to be restored and operational by April 2026. The company also owns a dedicated OLED R&D line, currently undergoing restoration, with completion targeted for September 2025.

Notably, HKC is planning to build a dedicated G6 (6th-generation) OLED mass production line based on eLEAP technology. While Kunshan was initially considered as the investment site, current indications suggest the project will likely shift to Mianyang in Sichuan Province, due to changing policy dynamics and stronger local government partnerships. HKC is currently seeking regulatory approval from the Chinese government for its G6 OLED line based on eLEAP technology. While FMM (Fine Metal Mask) processing is also being considered as an option, it is understood that approval for FMM is highly unlikely due to regulatory constraints. The production line is expected to incorporate secondhand equipment from Japan Display Inc. (JDI), with potential for accompanying technical support.

This strategy signals a broader shift in China’s OLED industry, moving beyond simple production scale-ups to focus on achieving global competitiveness in advanced manufacturing technologies.

A parallel effort is underway at Visionox, which is building a G8.6 OLED line (V5) in Hefei. There, the company is developing and preparing to mass-produce OLED panels using ViP (Visionox Intelligent Pixelization), a maskless pixel formation technology based on photolithography and patents from Japan’s SEL. This approach avoids the resolution and yield limitations associated with traditional FMM processes.

HKC’s eLEAP investment aligns with this broader maskless OLED trend. Developed by JDI, eLEAP technology enables precision pixel formation without metal masks, offering advantages in aperture ratio and panel longevity. HKC signed an MOU with JDI in 2023 for joint development of eLEAP-based OLEDs. Although the companies later scaled back plans for a joint OLED fab, technical collaboration is understood to be ongoing.

The parallel efforts of HKC with eLEAP and Visionox with ViP demonstrate China’s intent to lead not only in OLED manufacturing capacity, but also in core next-generation fabrication technologies. This shift underscores the nation’s strategic ambition for technological self-reliance and global leadership in OLED production—an ambition likely to reshape the future of the small- and medium-sized OLED industry.

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

OLED Layer Structure Comparison: FMM vs. ViP (Source: Visionox)

The key infrastructure processes for Visionox’s V5 project in China are progressing smoothly, signaling the full-scale preparation for next-generation OLED production. In parallel, Visionox has made a significant leap in securing core technological capabilities by signing a strategic patent license agreement with Japan’s Semiconductor Energy Laboratory (SEL).

The V5 line, currently under construction by Visionox in Hefei, Anhui Province, aims to move away from the conventional FMM (Fine Metal Mask) process and focuses on the production of mask-less OLED panels. To that end, the company is advancing its ViP (Visionox Intelligent Pixelization) technology—recently rebranded as mask-less OLED—as a next-generation high-resolution OLED manufacturing method.

Recently, Visionox successfully completed the roofing work for the V5 plant, wrapping up groundwork for major equipment installation. Core production equipment, including OLED deposition systems, has been ordered from AKT, a subsidiary of Applied Materials. Orders for additional essential equipment—such as exposure systems (Nikon), ion implanters (Nissin), and Excimer Laser Annealing tools—are also underway. The technical committee’s review for final investment approval of the V5 line shows positive progress.

In the meantime, Visionox has entered into a licensing agreement with SEL for core OLED-related patents. SEL holds a large number of fundamental patents related to LTPS (Low-Temperature Polycrystalline Silicon), oxide TFTs, and OLED driving technologies. The company is developing a lithography-based OLED process called metal maskless lithography (MML). Through this agreement, Visionox aims to reduce global patent risks and strengthen its technological competitiveness in mask-less OLED technologies and high-resolution panel design. Visionox’s mask-less OLED process is based on Applied Materials’ OLED Max (photolithography) technology. Unlike SEL’s approach, which performs cathode processing after the lithography step, OLED Max conducts lithography after forming both the cathode and encapsulation layers. Although SEL’s method may lead to shorter OLED material lifespan, it offers an advantage in improving process yield. The partnership with SEL is expected to become a major milestone in Visionox’s push toward commercialization of next-generation OLED technology.

With progress in the V5 project and expanding global technological partnerships, Visionox plans to continue reinforcing its leadership in the global OLED market through initiatives such as establishing a national-level R&D institute in Kunshan, diversifying AMOLED applications, and improving asset efficiency for sustainable, technology-driven growth.

Changho Noh, Analyst at UBI Research (chnoh@ubiresearch.com)

– OLED shipments expected to rise by approx. 70% in Q3 with the mass production of iPhone 17 series

2025 Panel Shipment Share For Apple

LG Display is poised for a rebound in earnings in the second half of the year as it ramps up OLED panel shipments for iPhones and iPads. According to market research firm UBI Research, Apple’s new iPhone 17 series and iPad Pro models entered full-scale mass production in July, leading to a projected sharp increase in LG Display’s OLED panel shipments in Q3.

UBI Research reports that LG Display accounted for 21.3% of iPhone panel shipments in Q2, falling behind China’s BOE for the first time, which recorded a 22.7% share. Samsung Display remained the leader, commanding 56% of shipments for iPhones.

Currently, LG Display supplies small- and mid-sized OLED panels exclusively to Apple, primarily focusing on LTPO panels used in the iPhone Pro lineup. These panels are priced higher than the LTPS panels supplied by BOE for the standard iPhone models, which means LG Display still leads in revenue terms despite lower shipment volumes.

The Q2 decline in LG Display’s shipments is seen as a temporary setback. Since Apple’s new iPhone series typically enters mass production in July each year, shipments are expected to surge starting in Q3. In fact, LG Display’s iPhone panel shipments are forecasted to reach around 18.5 million units in Q3—a 70% increase from Q2—and exceed 25 million units in Q4.

In addition to iPhones, shipments for iPad panels are also expected to rebound in Q3. Production of new iPad Pro models, which had sluggish sales last year due to high retail prices, began in July. As a result, iPad OLED panel shipments are expected to double from 800,000 units in Q2 to 1.6 million units in Q3.

Changwook Han, Executive Vice President of UBI Research, stated, “With both the iPhone 17 series and the new OLED iPad Pro models entering mass production in July, LG Display’s performance is set to show a clear recovery starting in the third quarter.” He added, “On an annual basis, LG Display is expected to secure over 30% of total iPhone OLED panel shipments in 2025.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

![]()

On June 26, 2025, Micro-OLED specialist Seeya Technology (希显科技) submitted its application for listing on the STAR Market (科创板) of the Shanghai Stock Exchange. Through this IPO, the company aims to raise approximately 2.015 billion RMB (about KRW 380 billion), with the funds primarily allocated to expanding production capacity and strengthening R&D.

Seeya currently operates with a monthly production capacity of 9,000 sheets (based on 12-inch wafers) and began equipment installation for Phase 2 in May 2025, which will add another 9K to its capacity. Depending on market conditions, Phase 3 investment is also planned, and once all phases are completed, the company is expected to reach a total monthly capacity of 27K.

The IPO process began at the end of 2024 and has recently completed all major pre-listing procedures. If all goes smoothly, Seeya is expected to complete its listing by 2026. The company is already supplying mass-produced products to key customers such as Xiaomi, DJI, XREAL, and Thunderbird (雷鸟科技). It is currently competing with BOE to secure Meta’s business, and has also established a strategic partnership with Apple.

With this IPO, Seeya is expected to further strengthen its position within China’s Micro-OLED industry and expand its influence in the global XR and AR device markets.

Detailed information on the current status of China’s Micro-OLED industry, including Seeya Technology, can be found in UBI Research’s China Trends Report.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

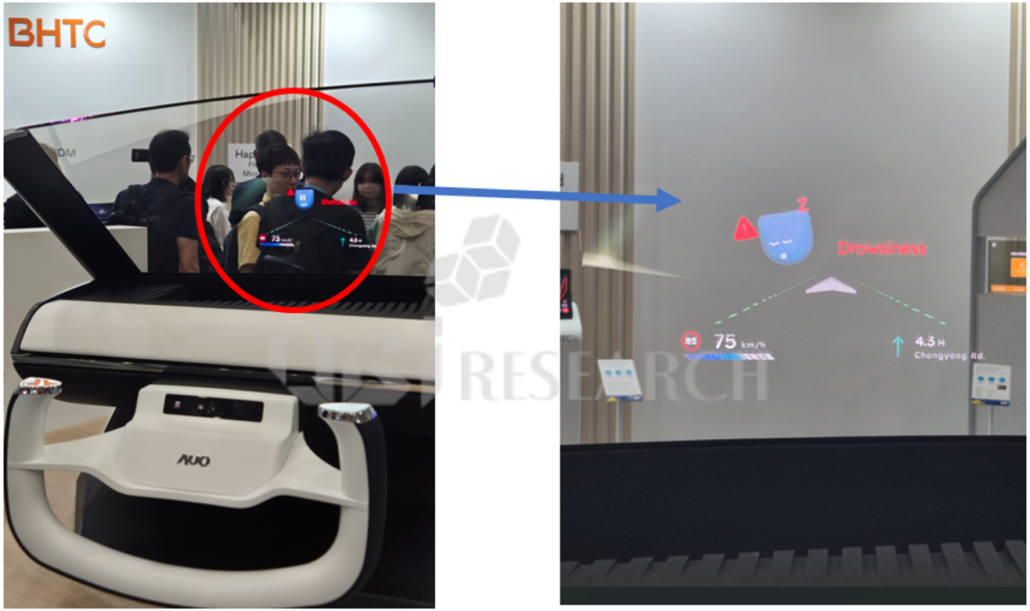

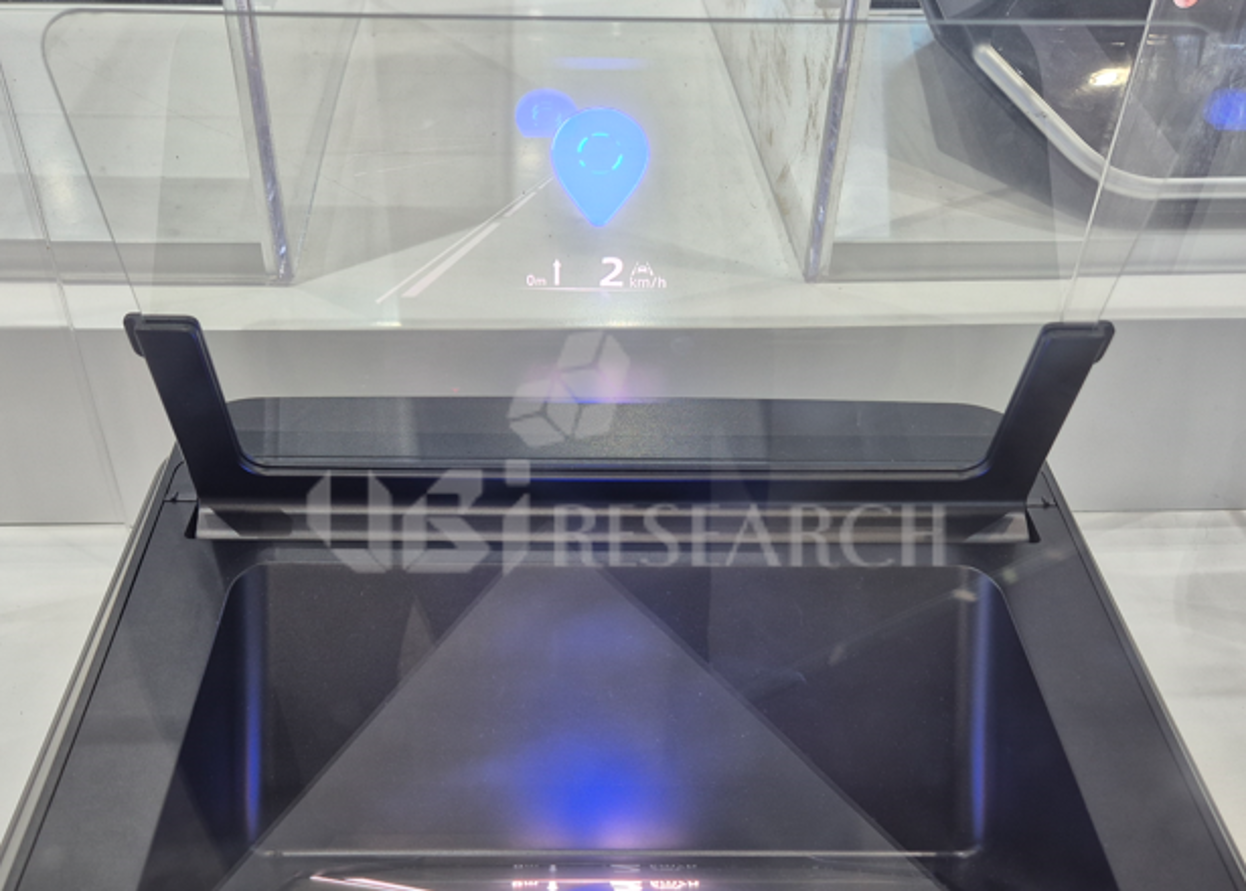

As in-vehicle display technologies continue to evolve rapidly, the head-up display (HUD), which projects various types of information into the driver’s forward field of view, is becoming an essential interface in modern vehicles. Recently, Panoramic HUDs (PHUDs) capable of displaying not only speed and navigation data but also augmented reality (AR) content have emerged, showcasing significant technological advancement. At the core of this evolution is Micro-LED technology, which is gaining traction as the key enabler of PHUDs.

PHUDs project information across the entire or a substantial portion of the windshield, requiring a wide field of view, high resolution, and high brightness. Currently, the most commercially viable implementation is the black strip reflection method. This approach utilizes the lower black band area of the windshield as a reflective surface, allowing for a simpler optical system and lower production costs—making it an attractive option for many automakers. However, to avoid obstructing the driver’s view, the image projection height is limited, typically restricted to a narrow vertical range of approximately 3 to 6 cm.

BMW Panoramic Vision

For a more immersive and premium experience, some high-end vehicles adopt a transparent reflection method. This involves embedding multilayer optical films or applying special structures within the windshield, allowing images to be reflected even in transparent areas without the need for a black band. While this method offers advantages in immersion and design, it poses significant challenges in optical complexity, higher costs, and low reflectivity—necessitating the use of ultra-bright displays.

Micro-LED provides a compelling solution to these structural and technological challenges. Thanks to its self-emissive pixel structure, Micro-LED can achieve brightness levels exceeding 1,000 nits, with ultra-high brightness capabilities reaching 30,000 to 50,000 nits—all while maintaining excellent power efficiency.

At SID 2025, major display companies such as AUO, BOE, and CSOT unveiled a range of Micro-LED-based PHUD prototypes. BOE showcased a 6.2-inch Micro-LED HUD with sub-0.2mm pixel pitch and 30,000 nits peak brightness (15,000 nits perceived brightness). CSOT presented a large 14.3-inch PHUD featuring 45,000 nits peak brightness (12,000 nits perceived brightness) and a wide viewing angle, while AUO demonstrated a 13-inch high-brightness PHUD with 12,000 nits of perceived brightness.

AUO 13” PHUD (12,000nits)

BOE 6.2” PHUD (15,000nits)

TCL CSOT 14.3” PHUD (12,000nits)

Micro-LED is not merely enhancing display performance—it is fundamentally transforming the structure and implementation of Panoramic HUDs. It overcomes the limitations of restricted reflection areas, enables the projection of high-brightness, high-resolution images onto various curved windshields, and meets the demands for transparency and design flexibility. As the commercialization of PHUDs becomes a reality, Micro-LED stands at the center of this transformation. The future of automotive vision and interface will unfold on Micro-LED.

Changwook HAN, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report

Galaxy Z Fold7 & Z Flip7 (Source: Samsung Electronics)

Samsung Electronics unveiled the Galaxy Z Fold 7 on July 9, announcing its global launch in late July. The new Z Fold 7 reduces weight to 215 grams and measures just 8.9 mm when folded and 4.2 mm when unfolded, making it the thinnest and lightest Z Fold series yet. Compared to its predecessor, the Fold 6, the Galaxy Z Fold 7 offers noticeable improvements in thickness and weight. When folded, it’s 8.9mm thick, down from 12.1mm, which is about 3.2mm thinner, a reduction of about 26%. When unfolded, the thickness has also been reduced from 5.8 mm to 4.2 mm, which is about 28% thinner. The weight is also 24 grams lighter, from 239 grams to 215 grams. The main display has grown from 7.6 inches to 8.0 inches, and the cover display has widened from 6.3 inches to 6.5 inches. This is designed to improve both portability and visual immersion. The new “Armor Flex Hinge” uses enhanced materials and structural innovations to achieve a durable and thin design.

The 2025 foldable cell phone market is facing an intensifying race to slim down, and in addition to Samsung, other major manufacturers such as Vivo, Oppo, and Honor are launching a series of products in the 9mm or smaller class. The thinnest major foldable smartphone currently on the market is Honor Magic V5 White, which measures 8.8mm when folded and 4.1mm when unfolded. The lightest is the Galaxy Z Fold 7, which weighs just 215g, making it extremely portable. In terms of battery capacity, the Vivo X-Fold 5 has the largest at 6,000 mAh, which gives it an advantage for extended use. In terms of camera resolution, the Galaxy Z Fold 7 has a 200MP main camera, which offers top-notch shooting performance. Meanwhile, the OPPO Find N5 has the largest main display size at 8.12 inches, which is favorable for content viewing and multitasking.

Apple is currently working on its first foldable iPhone, which is expected to be released as early as the second half of 2026. Apple is preparing a book-type form factor with a 7.8-inch internal display and a 5.5-inch external display supplied by Samsung Display, and it is expected to be the thinnest device ever made by Apple, with a thickness of approximately 4.5 millimeters when unfolded and 9 to 9.5 millimeters when folded. The foldable iPhone will be powered by the next-generation A20 or A21 Pro chipset and will feature an iOS custom UI optimized for foldable experience. Foxconn plans to begin mass production of foldable iPhone around September or October 2025, and the product is expected to cost about twice as much as the iPhone 16 Pro Max. Meanwhile, Apple’s entry into the foldable market is expected to have a major impact on the entire foldable phone market, and competition among global manufacturers is expected to be in full swing between 2025 and 2027. In particular, the points of competition in the foldable market are becoming increasingly clear.

Ultra-slim design is not just a design innovation but also requires lightweight and slimmer technologies for core components and materials such as ultra-thin glass (UTG), hinge structures, battery packs, and highly integrated FPCBs. Therefore, the future foldable competition is expected to be characterized not only by device perfection, but also by securing technology at the component and material level as a key differentiator. Battery performance is also an important competitive factor, with the Vivo X-Fold 5 featuring a large 6,000mAh battery for long-lasting use, while the OPPO Find N5 supports 80W wired charging and 50W wireless fast charging. In terms of camera performance, Samsung’s Fold 7 has the highest image quality among foldable phones, with a 200-megapixel (200MP) main camera. In terms of software and AI optimization, Samsung is actively applying Google Gemini-based Galaxy AI, while Apple is preparing a multi-screen iOS for foldable displays. Finally, durability and waterproofing and high prices remain the biggest weaknesses of foldable phones and will likely be the key to product differentiation in the future.

In the end, the market for foldable phones will evolve toward “thinner, lighter, and smarter,” with design sophistication, software integration, battery life, and AI utilization emerging as key competitive factors. Apple’s entry is likely to accelerate all these competitive points.

Changho Noh, Analyst at UBI Research (chnoh@ubiresearch.com)

Samsung Display held its first employee communication event, Detox (D- Talks), since President Lee Chung took office. At this event, President Lee clarified the future strategic direction of Samsung Display and expressed his strong will to sustainably expand global competitiveness through securing ultra-differentiated technologies. In particular, he emphasized the need for business diversification beyond the conventional OLED-centered structure in a situation where the display industry is rapidly undergoing a transition, and clearly mentioned the technological advancement and product expansion in the Micro LED field as part of such diversification.

President Lee Chung’s statement is more than a simple statement of direction; it can be taken as a declaration that Samsung Display will secure a competitive advantage in panels, materials, and processes in general, rather than simply supplying backplanes for the Micro LED business. This is interpreted as a signal that the Micro LED TV business, which has been led by Samsung Electronics, may break away from its focus on set manufacturing and expand into the overall display sector.

Samsung Electronics has been leading the Micro LED industry ecosystem domestically, but in terms of actual device supply and panel production, it has had to work with partner companies in Taiwan and China. (Taiwan) and Sanan Optoelectronics (China), and backplane drive technology cooperation with AUO (Taiwan) and BOE (China), reflecting the situation where Korea’s core components and materials ecosystem has not been fully internalized. While such cooperation has the advantage of global technology integration, it has been a disappointing structure in terms of technological independence of the domestic Micro LED industry and the establishment of an independent ecosystem.

With Samsung Display’s full-scale expansion of technology investment and clarification of its position on applying ultra-differentiated technology to Micro LEDs, the Korean ecosystem is expected to reach a qualitatively different turning point. Samsung Display already possesses the world’s best TFE (thin film encapsulation), LTPO, low power design, and backplane drive technologies for OLEDs, and these technologies can be applied to driving high resolution, improving yield, and ensuring transfer accuracy of Micro LED devices. In particular, highly integrated drive circuit design, ensuring low current drive characteristics, and process automation are areas of relative advantage for Samsung Display, which is based on OLED technology.

Beyond simple technological sophistication, Samsung Display’s participation may serve as a signal to promote stronger cooperation with Korean material, component, and equipment manufacturers. This could serve as a foundation for Samsung Electronics to simultaneously strengthen its internal technological capabilities and promote domestic production of its supply chain in core areas such as chip supply and demand, company-wide equipment, and process equipment, on which it has long relied externally, and in the long run could serve as a catalyst for the formation of a domestic Micro LED cluster.

President Lee’s comments can be interpreted as a strategic declaration to redefine the next-generation technology initiative in the display industry within the domestic ecosystem, beyond simply strengthening the development of Micro LED technology. In that Samsung Display has begun to seriously nurture a new axis of Micro LED in preparation for OLED and beyond, the time has come when new opportunities may open up not only for changes in the industrial foundation but also for small and medium-sized Korean partners and investors in the future.

Joohan Kim, Analyst at UBI Research (joohanus@ubiresearch.com)

BOE Chairman Chen Yanshun met with senior executives from Samsung Electronics’ Video Display (VD) division on June 30, according to industry sources. The meeting was attended by Chen and other top BOE executives, and was reportedly held to explore ways to improve relations and seek potential strategic cooperation between the two companies.

BOE is China’s largest display manufacturer, producing large-size LCD and OLED panels. The company maintains a strong presence in the domestic TV and IT display markets and supplies products to global clients. Samsung Electronics’ VD division, which oversees its TV business, has maintained the No.1 position in the global TV market for several years, making stable panel procurement a key strategic focus.

The meeting was part of a formal consultation between the two companies and is seen as a move to reset relations that have been relatively distant in recent years. Specific details or outcomes of the discussion were not disclosed.

Industry observers note that the direct involvement of Chairman Chen highlights BOE’s strong interest in restoring its business ties with Samsung Electronics. With Samsung also reviewing and restructuring its display supply chain, this meeting could mark an inflection point in the relationship between the two firms.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

As displays have become a core interface that influences the overall user experience beyond a component of the vehicle interior, technological evolution is also reaching a new turning point. The technology at the center of this is ‘Stretchable Micro LED’. This display, which can be freely applied to curved surfaces as well as implemented with elasticity and three-dimensional physical manipulation, is drawing attention as the future of digital interfaces, especially in the automobile industry.

Initially, stretchable OLED based on organic materials was studied as a promising technology candidate. OLED has strengths in thin film and self-luminous structure, and is also relatively advanced in terms of yield. However, OLED has a structure that is vulnerable to moisture and oxygen, so TFE (Thin Film Encapsulation) is essential, and it is difficult for this encapsulation layer to secure both flexibility and stretchability. In particular, in an environment where the display is stretched, the encapsulation layer may crack or it is difficult to maintain uniformity, so the actual stretch ratio of OLED that can be stretched is limited to 10% or less. Accordingly, the industry has recently shifted its focus back to Micro LED, as research on stretchable displays that was once conducted based on OLED.

Stretchable OLED & Micro-LED

Micro LEDs are composed of inorganic-based components, so they can operate stably even in harsh environments inside a vehicle, such as high temperatures, vibrations, and ultraviolet rays. In fact, in 2023, Samsung Display unveiled an 11-inch stretchable micro LED prototype and demonstrated a stretch ratio of 25%.

However, stretchable micro LEDs are not yet technically complete. The most important challenge is productivity. Micro LED chips must be accurately transferred in millions of units, but if the substrate is a stretchable soft material, it is very difficult to secure transfer precision. Another challenge is cover fusion technology for implementing touch and operability. Since stretchable displays are implemented on soft substrates such as silicone rubber, they are fundamentally limited in terms of touch sensitivity and durability. In particular, to implement precise touch recognition or physical operability, a hard cover layer like glass is required. Accordingly, the industry is focusing on developing hybrid cover materials that can simultaneously satisfy flexibility and rigidity, and high-elasticity hard polymers and film-glass composite structures are being considered as viable alternatives.

A representative example that showed the practical possibility of stretchable displays is LG Display’s ‘3D interface type stretchable display’ unveiled at SID 2025. This technology has a structure in which the surface rises in response to the user’s movements, and has garnered attention as an HMI that can provide not only visual information but also physical feedback. Also, at CES 2025, AUO unveiled a ‘3D stretchable display’ with a similar concept. This display is composed of stretchable micro LEDs, and when the user touches or raises their hand, the display locally rises, allowing it to be operated like an actual button.

LGD 12-inch Stretchable Micro-LED@SID 2025

AUO 14.3-inch Stretchable Micro-LED @CES2025

Automotive interiors are gradually evolving into ‘digital sculptures’, and displays are playing a central role in delivering real-time responsiveness and emotional experiences. Stretchable micro LEDs are not simply displays that can be stretched, but are evolving into ‘three-dimensional interfaces’ that can organically connect the entire physical space of a car. Although there are still technical challenges to be solved, if cover substrates, touch integration, and large-area precision transfer technologies are completed, this technology will become an essential core axis in future vehicle interior UX design.

Changwook HAN, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report

Plans for 8.6G OLED Line Construction by Panel Makers

Monthly Production Capacity of 45K; Equipment Installation Targeted for End of 2026

According to UBI Research’s China Market Trend Report, Chinese display company TCL CSOT (China Star Optoelectronics Technology) is planning to construct a new 8.6-generation (2290x2620mm) OLED line at the T8 site near its existing T9 OLED line in Guangzhou. This investment will be based on inkjet printing technology, with a Step 1 investment fund scale of approximately RMB 20 billion (approximately KRW 3.8 trillion).

The T8 site was initially intended to be converted for a solar project, but that plan has been put on hold, and the site will now be used for its originally planned OLED production line. The T8 project is designed to consist of two 8.6G OLED lines with a total monthly production capacity of 45,000 substrates (45K), and the initial investment will be made for one line.

The investment schedule for the T8 line includes an official announcement in July 2025, groundbreaking in October, and the start of equipment installation by the end of 2026. The general manager of the project has been appointed as Linpei (林佩), and the core inkjet process technology is being led by a Korean expert.

Inkjet printing technology is known for its approximately 30% lower equipment investment cost compared to the traditional mask-based deposition method. For example, Samsung Display is investing around KRW 4 trillion to build an 8.6-generation OLED line for IT applications (15K per month) at its A6 site in Asan, Chungcheongnam-do, based on the conventional deposition process. In contrast, TCL CSOT plans to adopt inkjet printing technology to secure a monthly production capacity of 45K at the 8.6-generation level, with an initial investment of RMB 20 billion.

Han Changwook, Executive Vice President of UBI Research, commented, “Inkjet OLED still faces technological challenges in brightness, lifespan, large-area uniformity, and yield. Nevertheless, China is positioning this differentiated technology from traditional deposition as a next-generation growth driver and, under strategic government support, is preparing for full-scale mass production. Through investments in inkjet technology by TCL CSOT and ViP (Visionox intelligent Pixelization) by Visionox, China is pushing ahead with the first mass production of large-area OLEDs, aiming to secure technological leadership.”

As demand for IT displays is expected to grow, it remains to be seen whether the commercialization of inkjet technology in large-area OLEDs will determine future market leadership.

Changwook HAN, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

As AI technology advances, the XR market is heating up again, evolving from a simple wearable device to a personalized digital assistant. Global big tech companies such as Google, Meta, Apple, and others are taking the lead in the market with their respective ecosystems, and Samsung Electronics is also joining the trend with aggressive investments and product strategies.

Recent XR devices have gone beyond basic functions such as music listening, camera shooting, and voice control to include advanced AI functions such as real-time translation, object recognition, and personalized information at their core. This is greatly increasing their utility in everyday life and evolving the way they interact with users.

For example, Meta has sold over 1 million units of AI smart glasses in collaboration with Ray-Ban and is leading the democratization of AI glasses with real-time content generation and Q&A capabilities. Google is building a smart glasses ecosystem that combines its Gemini AI with the Android XR SDK, and a joint development project with Samsung is well underway.

Apple is expected to launch a Vision Pro M5 version in Q3 2025, followed by the lighter Vision Air in 2027 and a display-less Ray-Ban-style smart glasses in 2028. In the second half of 2028, the second generation of Vision Pro with an all-new design and XR glasses with a color display are planned for mass production. Vision Air and Vision Pro Gen 2 are expected to be lighter and more affordable with a new design. Apple’s Vision Pro launched in 2024, was priced at $3,499, which was considered too high for consumer expectations and a product that was technologically advanced but disconnected from the market and consumer reality. The Apple Vision Pro’s 1.42-inch, 3391 PPI high-resolution display was a major contributor to its high cost. Apple’s development plan shows Apple’s long-term vision to enter the mass smart glasses market and build an ecosystem while maintaining the premium XR headset market.

Samsung Electronics will officially launch its next premium XR device, Moohan, in the second half of this year. The product will provide new XR experience through the convergence of AI and display technology and will signal Samsung’s entry into the XR ecosystem. The device will feature a 1.3-inch, 2000 PPI OLED-on-Silicon (OLEDoS) display developed by Samsung Display, which is expected to offer light weight, excellent battery efficiency, and a price below $2,000. Samsung initially looked at Sony’s 1.3-inch, 3800 PPI OLEDoS. It remains to be seen whether Samsung will split the product into premium and entry-level variants for price competitiveness or release it as a single product.

Starting with Project Moohan, Samsung plans to launch an integrated strategy that encompasses XR hardware, software, content, and platforms. To this end, Samsung is strengthening its collaboration with big global tech companies such as Google and Qualcomm and is simultaneously promoting ‘Project Hyean’ to maximize connectivity with the entire Galaxy ecosystem, including smartphones, watches, and rings.

Changho Noh, Analyst at UBI Research (chnoh@ubiresearch.com)

BOE’s OLED Panel Production Complex (Source: BOE)

Concerns Rise That B9 Funds May Be Diverted to Visionox’s FMM-Based Line Following ViP Investments

BOE is strongly opposing the Hefei local government’s move to withdraw its stake in the B9 OLED plant. The Hefei government is reportedly seeking to divest its shares worth around 20 billion yuan, and there are growing concerns that the funds could be redirected to Visionox’s V5 line—a direct competitor. BOE is closely monitoring the direction of this potential fund reallocation.

Currently, Visionox is investing in a 7.5K production capacity line at the V5 plant, implementing its proprietary ViP (Visionox intelligent Pixelization) technology. Visionox initially planned to build a 15K production capacity line using a ViP + FMM (Fine Metal Mask) hybrid method. However, due to financial constraints, the FMM portion of the investment was put on hold. If the capital withdrawn from B9 is allocated to Visionox, the company could not only complete the ViP line but also proceed with the additional 7.5K FMM-based investment. This would pose a direct long-term threat to BOE’s market share and competitiveness.

For this reason, BOE is opposing the Hefei government’s withdrawal and aims to maintain its leadership in OLED investments in the Hefei region. BOE is also internally reviewing plans to reinvest the B9 equity into new production lines or expand existing ones. Meanwhile, the Hefei municipal government is reportedly considering new investment strategies to restructure the region’s display industry.

This issue of divestment and fund reallocation by the Hefei government signals more than just a financial adjustment—it indicates a potential realignment of technology, capital, and production capabilities within China’s OLED industry. The rivalry between BOE and Visionox is expected to intensify, possibly escalating into a broader strategic competition for OLED market leadership.

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

As AI technology continues to mature, the AI era is upon us. Following last year’s trend, 2025 is expected to see the release of even more AI-powered eyewear products. The integration of AI and AR technologies, which began last year, is set to flourish further by 2025. There are also rumors that Apple’s smart glasses will be released by the end of 2027. The competition among big tech companies to emerge victorious in the AI war is intensifying.

“AI” was a highlight of CES 2025, and AI smart glasses were one of the focal points of attention. Companies such as Vuzix, Rokid, Goertek, and RayNeo unveiled new AI glasses incorporating micro-LED technology. The TCL RayNeo X3 Pro model was announced to enter mass production in the second quarter.

On June 26, Xiaomi held a new product launch event in Beijing. The announcement of Xiaomi’s new AI smart glasses is sure to have sent shockwaves through Ray-Ban Meta.

Xiaomi AI Glasses (Source: Xiaomi)

Xiaomi’s AI glasses are a product aimed at becoming “the next generation of personal smart devices.” They are smart glasses that do not include a display and are operated by voice and touch, supporting voice calls, photo shooting, and video recording. The basic model starts at $280 (1,999 yuan), and the high-end photochromic model is priced at up to $420 (2,999 yuan). The directly competing product, Ray-Ban Meta AI glasses, starts at $299.

Compared to Meta glasses, Xiaomi glasses are superior in terms of hardware specifications, such as the camera sensor (equipped with a 12-megapixel IMX681 sensor), and the frame weighs only 40 grams, which is lighter than Meta’s 48 grams. The battery life is also longer, with Xiaomi offering 8 hours, which is twice as long as Meta’s. However, a weakness lies in the lack of an application ecosystem for connecting and sharing with social content platforms like Facebook or Instagram. Nevertheless, Chinese companies are expected to address these technical and functional shortcomings, and competition in the AI glasses global market is likely to intensify further.

Namdeog Kim, Senior Analyst at UBI Research(ndkim@ubiresearch.com)

Samsung Display researchers revealed it in a recent paper published in J. Soc. Info. Display, the official journal of the Society for Information Display (SID), that they have developed a next-generation OLED-on-Silicon (OLEDoS) microdisplay with 4032 PPI (pixels per inch). This technology is optimized for the next generation of XR devices, including virtual reality (VR), mixed reality (MR), and augmented reality (AR), with panels that dramatically reduce system power consumption and crosstalk while maintaining high resolution and image quality.

This 1.3-inch panel has an ultra-high resolution of 4032PPI, delivering images so precise that pixels are indistinguishable to the naked eye. This minimizes the screen door effect in VR and AR glasses, enabling an immersive content experience. The display of the Apple Vision Pro, released in 2024, features a high-resolution display with a size of 1.42 inches and 3,391 PPI.

In this paper, a pixel compensation circuit structure with 7T1C (7 transistors and 1 capacitor) structure was introduced for high-resolution implementation, which complemented the shortcomings of the previous generation, 6T2C structure, and realized a design that was strong against voltage deviation.

Existing 6T2C pixel structures have caused problems with threshold voltage (Vth) deviations and image distortion between small transistors when implemented in high resolution. Accordingly, Samsung Display’s newly devised 7T1C structure provides the following major advantages.

In addition, improvements have been made in the way data is driven. The existing 6T2C circuit consumes a lot of power because it has to charge and discharge a data line every frame, but the 7T1C greatly reduced power consumption by a single charging method. For example, in the same full gray pattern, the power consumption of the source IC decreased from 120 mW to 0.1 mW.

In addition, while lowering the operating voltage through the 8V CMOS-based design, it secured more than 50% of the power efficiency compared to the previous one.

Samsung Display officially announced its dual-track strategy to develop RGB OLEDoS and white-based OLEDoS simultaneously last year, and this 4032PPI panel is considered the result of that technological achievement. Although the mass production date for this newly developed product has not been announced, this technology is expected to serve as an important step in accelerating the development of the next-generation XR device market.

About the paper: J Soc Inf Display, 1–9(2025).

SID 2025 Digest 1424 (P-8)

4032-PPI 1.3-inch OLEDoS Reference Image

4032-PPI 1.3-inch OLEDoS Reference Image and Specifications

Changho Noh, Analyst at UBI Research (chnoh@ubiresearch.com)

The application areas of transparent displays applicable to automobiles are diversifying along with technological advancements, and currently, the feasibility of four major areas is being discussed. First, a windshield transparent display that directly integrates the display into the windshield of a vehicle; second, a front combiner-type transparent display installed within the driver’s field of vision; third, a rear-seat side transparent display applied to the rear-seat side window; and fourth, a transparent partition display that separates the driver’s seat and the rear seat. Each display has different transmittance and technical requirements depending on the characteristics of the application area and legal standards. A windshield transparent display is a technology that projects vehicle driving information directly onto the windshield, allowing the driver to recognize various information without taking their eyes off the road. However, the windshield is legally required to have a visible light transmittance (VLT) of 70% or higher, and the current transparent OLED (approximately 45%) and Micro LED (approximately 55%) technologies do not meet this requirement. Therefore, directly inserting a display into the windshield is still realistically difficult not only due to technical limitations but also from a regulatory perspective.

The front combiner type transparent display is a method of installing a separate transparent display panel on the instrument panel or near the windshield, and requires a transmittance of VLT 70% or higher. Therefore, even in this area, OLED or Micro LED technology currently has limitations in meeting regulations in terms of transmittance, and some pilot products are being developed in a way that circumvents regulatory standards by limiting the size and installation location.

The rear seat side transparent display can be used for entertainment, information provision, advertising, etc., and most countries have no or relaxed regulations on transmittance for rear seat side windows, so commercialization is highly likely. OLED and Micro LED technologies with transmittances of 45-55% can also be sufficiently applied, and there have been cases where they have been used as advertising-type transparent displays because visibility is secured from outside the vehicle. In particular, Micro LED is evaluated more favorably than OLED in terms of commercialization due to its high brightness, durability, and strong resistance to external temperature changes.

The transparent partition display is a new area that can separate the driver’s seat and the rear seat space in a vehicle as autonomous driving becomes more advanced, while simultaneously performing privacy protection and information transmission functions. Since the relevant area is located in the interior of the vehicle, legal regulations on transmittance do not apply, and both OLED and Micro LED can be freely used.

The biggest limitation of current automotive transparent display technology is low transmittance. Transparent OLED has a VLT of about 45%, and Micro LED has a VLT of about 55%, so a transmittance of at least 70%, and ideally 75% or more, is essential for application to the windshield or front combiner area. To achieve this, various technological advances are necessary, such as improving the pixel transparency, minimizing the light-emitting area, developing high-transparency electrodes, and optimizing the optical structure. In particular, Micro LED is a structure that can theoretically increase transmittance by expanding the non-occupied area between pixels, so it is attracting attention as a technology with a higher possibility of meeting future regulations.

In conclusion, the applicability and required transmittance of vehicle transparent displays differ depending on the area, and with the current level of technology, it can be applied primarily to areas such as the rear seat side and interior partition. In order to apply it to the windshield and direct view area, two tasks must be solved simultaneously: improving technical transmittance and meeting legal standards. The transmittance required at this time should be at least 70%, and ideally 75% or more for actual use. When technology that satisfies these conditions is developed, a truly transparent display-based smart car environment can be realized.

Required Transmittance for Automotive Transparent Displays

Windshield Transparent Display

Combiner Transparent Display (Source: AUO)

Partition Transparent Display

Rear Side Window Display (Source: LG display)

Changwook HAN, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

2025 Automotive Display Technology and Industry Trends Analysis Report

BOE’s panel shipments for iPhone

According to UBI Research’s China Industry Trends Report, BOE has established an annual production capacity of up to 100 million OLED panels for iPhones, primarily through its B11 line.

BOE currently operates 26 Apple-dedicated module lines, of which 11 lines are in mass production and 3 lines are being used for development purposes. With a tact time reduced to 5.5 seconds, each line can produce up to 350,000 modules per month, resulting in a total monthly capacity of around 8 million iPhone modules. If the B11 line is fully dedicated to iPhone production, BOE can produce 8–9 million panels per month, or approximately 100 million panels annually, based on a 90% utilization rate and 85% yield.

Despite this significant production capacity, BOE’s actual panel shipments remain well below this level. In the first half of 2025, BOE shipped approximately 21 million iPhone panels, marking a 13% increase compared to 18.6 million units during the same period in the previous year. The company is expected to ship 24 million units in the second half of 2025, with total annual shipments projected at 45 million units. Should BOE succeed in supplying panels for the iPhone 17 series, shipments could increase further. However, as with the iPhone 16, BOE is likely to face difficulties in the early phase of new model production.

Although BOE still lags behind Samsung Display and LG Display in terms of technology, industry analysts note that it is rapidly narrowing the gap.

UBI Research’s Analyst Junho Kim commented, “As BOE’s share of iPhone panel supply continues to grow, this is expected to put increasing pressure on Samsung Display and LG Display during pricing negotiations with Apple. With BOE aggressively catching up, it will be critical to see how the Korean companies maintain their technological lead and strategic partnership with Apple.”

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

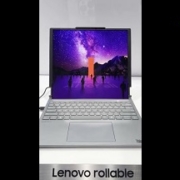

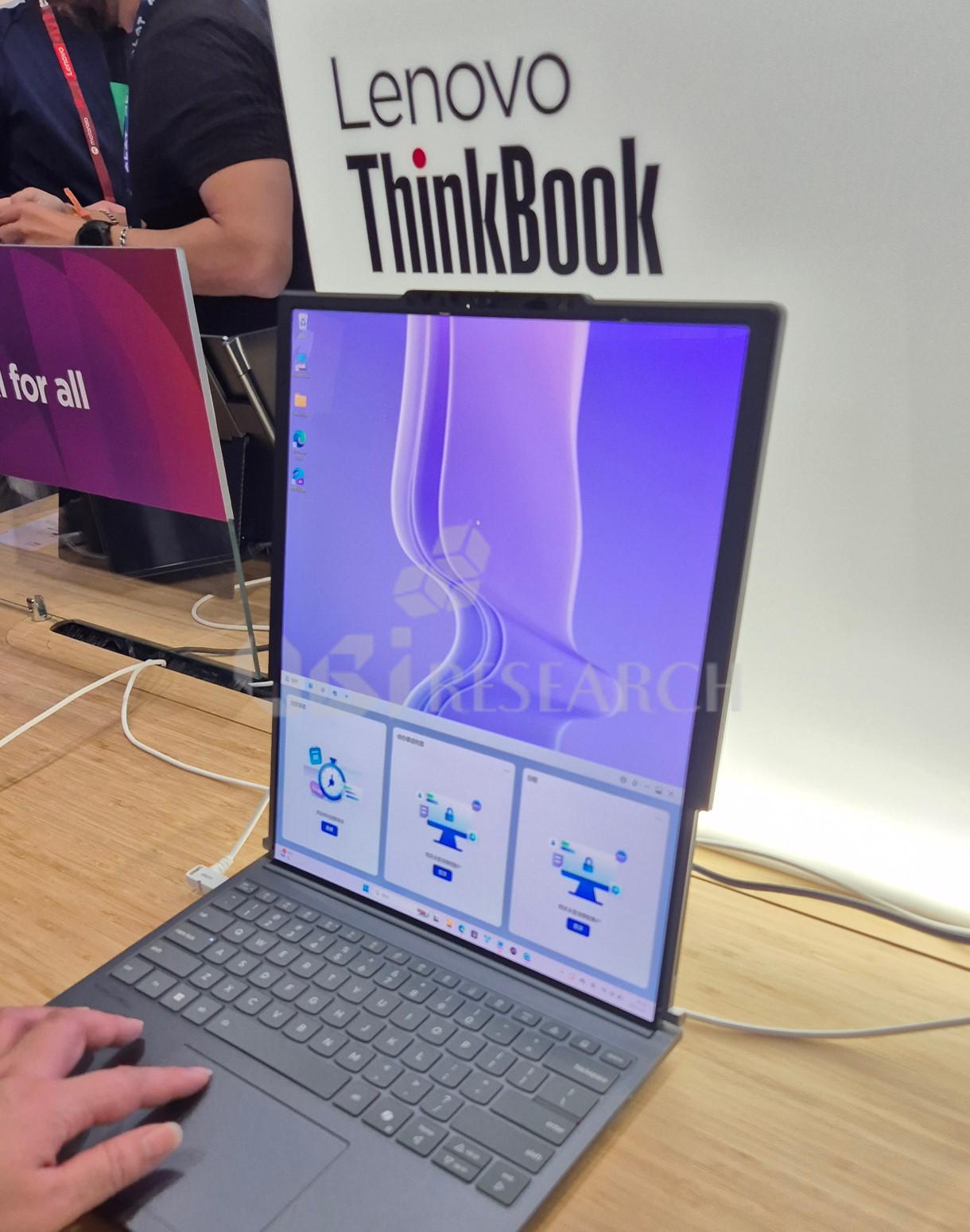

Lenovo’s ThinkBook Plus Gen 6 with Samsung Display’s 16.7-inch Slidable Flex Solo

“SID Display Week 2025,” the world’s largest display technology event held in San Jose, USA, in May 2025, was a stage where you can directly see the evolution of next-generation form factor technology. In particular, rollable and slidable displays are no longer concepts, but have become technologies that are about to be commercialized as actual products. At the same time, Samsung Display has significantly improved its technological completeness by announcing material technology innovations to solve the structural problems of rollable displays.

Rollable displays have been gaining attention as next-generation displays that simultaneously provide portability and large-screen experiences, with a structure that expands as if the screen is rolled up. At SID 2025 and CES 2025, major global companies drew attention by implementing these into actual products.

Lenovo’s ThinkBook Plus Gen 6 Slidable AI PC, which was commercialized in the first quarter of 2025, is equipped with Samsung Display’s slidable OLED and extends from 14 inches to a maximum of 16.7 inches and has passed durability tests more than 30,000 times.

At CES 2025, Samsung Display unveiled a prototype of its vertically expanded “Slidable Flex Vertical” smartphone. It is evaluated as a new method that simultaneously provides portability and a large screen experience by sliding vertically from the basic 5.1-inch screen size to a 6.7-inch large screen. There is also interest in whether Samsung will commercialize a Galaxy Rollable Phone based on its own slidable OLED technology in the future.

At SID 2025, BOE unveiled a rollable OLED prototype that extends from 12.3 inches to 17.3 inches. The product is characterized by an expansion ratio of 4 mm and 3.2:1 in roll radius and has been introduced to have a flexural durability of more than 100,000 times.

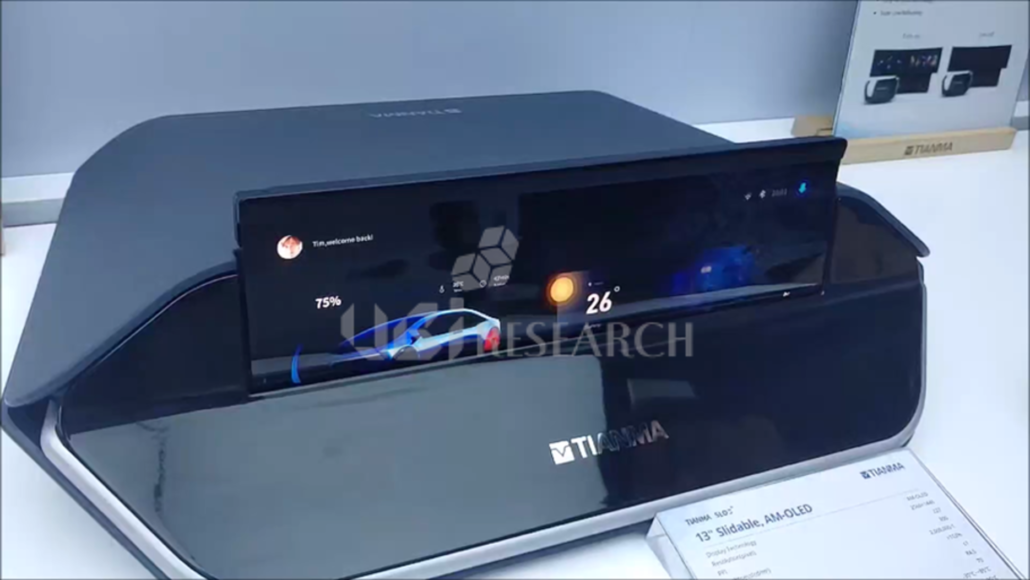

Tianma entered the advanced form factor competition by introducing a 13-inch sliding AMOLED prototype. It was designed with a radius of curvature (R) of 5 mm, the screen can move 70 mm, and it was reported that there was little change in thickness and flatness before and after the slide.

Rollable and sliderable displays still face technical challenges such as durability, uniform resilience, and reliability of the drive mechanism, but structural design and material innovation are emerging as the key to solving these issues.

Samsung Display emphasized the importance of material development, a core technology of rollable displays, by publishing a paper titled “Highly Reversible and Robust Rollable AMOLED Display with Smart Elastomer Materials” at SID 2025. The paper was chosen as the Distinguished Paper for Display Week 2025.

Samsung Display has greatly increased the durability and resilience of rollable displays with its two-layered smart elastomer structure, which is highly elastic and low elastic. Thanks to the new structure, the deformation of the edge of the panel has been significantly reduced even after the pen drop test and repeated rolling. The elastomer layer significantly reduces deformation compared to conventional polyimide and showed excellent recovery even in repeated rolling. Anti-static treatment was added to effectively suppress panel image damage due to repetitive friction and charging.

Rollable and slidable OLED technologies are now entering various product markets such as smartphones, laptops, and vehicle displays beyond the technology demonstration stage. At the same time, the mechanical stress, durability, external impact and electrostatic accumulation problems they experience cannot be solved without high-performance material technology. The smart elastomer-based double-layer design proposed by Samsung Display presents an answer to these problems, potentially giving the company a technological edge in the premium mobile device and automotive large-format display markets. The next initiative in the display industry will be completed through integrated technology that synergistically combines materials, structures, and processes for design innovation.

Changho Noh, Analyst at UBI Research (chnoh@ubiresearch.com)

Monthly Smartphone & Foldable Phone OLED Display Market Tracker

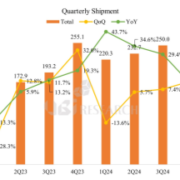

According to the Monthly Smartphone & Foldable Phone OLED Display Market Tracker published by UBI Research, a market research firm, Samsung Display’s shipments of foldable OLED panels surged starting in May, securing the top market share in the second quarter of 2025.

In the first quarter of 2025, Samsung Display shipped approximately 250,000 foldable OLED panels, trailing behind major Chinese panel makers such as BOE, CSOT, and Visionox. However, beginning in May, the company significantly ramped up mass production of panels for the upcoming Galaxy Z Flip/Fold 7 series, driving a sharp increase in shipments.

Samsung Display shipped 1.78 million units in May and 1.53 million units in June, accounting for 52% of total foldable OLED shipments in the second quarter, ranking first in the market. Following Samsung Display, BOE recorded shipments of 1.8 million units in the second quarter, CSOT 900,000 units, and Visionox 500,000 units.

Samsung Display is expected to maintain the top share in the third quarter as well. Furthermore, with its exclusive early supply of panels for Apple’s foldable iPhone in 2026, Samsung Display is projected to sustain its dominance in the foldable OLED market.

The global foldable OLED panel market continues to expand. Annual shipments grew from 15 million units in 2022 to 21.8 million in 2023, reaching 25 million units in 2024. The figure is forecasted to grow to 30.8 million in 2025. With Apple’s anticipated entry into the foldable phone market and the increasing number of foldable models launched by Chinese smartphone brands, annual shipments are expected to surpass 50 million units by 2029.

UBI Research Executive Vice President Chang Wook Han stated, “Thanks to the full-scale mass production of the Galaxy Flip/Fold 7 series, Samsung Display is expected to maintain the highest shipment volume in the third quarter,” and added, “The overall foldable phone market is likely to remain at a similar level to last year in 2025, but will begin significant expansion from 2026 with the anticipated release of Apple’s foldable phone.”

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Monthly Smartphone & Foldable Phone OLED Display Market Tracker

LG Display has embarked on a major initiative to strengthen its OLED business. On June 17, the company announced that its board of directors had approved a large-scale facility investment plan worth KRW 1.26 trillion (approx. USD 900 million), aimed at enhancing next-generation OLED technologies at its production bases in Paju, South Korea, and Vietnam.

The core of this investment is focused on the Paju plant in Gyeonggi Province and the company’s module plant in Vietnam.

Approximately KRW 700 billion will be invested in Paju, covering upgrades such as LTPO 3.0 technology for smartphones and IT devices, COE (Color on Encapsulation) implementation, enhancements to the RGB 2-stack tandem OLED structure, and additional chamber installations for 4-stack WOLED production.

The Vietnam module facility will receive about KRW 560 billion, primarily to improve module process efficiency and automation capabilities.

As LG Display transitions its Paju panel production lines to LTPO, the company expects a temporary reduction in production capacity. To mitigate this, it will also optimize overall production facilities.

With this facility upgrade, LG Display aims to secure a competitive edge in next-generation IT OLED panels and strengthen its responsiveness to premium mobile and tablet markets.

The investment will be funded through capital raised from the sale of the company’s LCD plant in Guangzhou, China, in 2023 (approx. KRW 2.2466 trillion). LG Display is also registered with the Ministry of Trade, Industry and Energy as a reshoring company, making it eligible for subsidies worth around KRW 50 billion.

An LG Display representative stated, “This investment is not just about expanding facilities but is a strategic move to shift toward high-value OLED products. We aim to strengthen both our technological capabilities and profitability, laying a solid foundation for a return to profitability in 2025.”

Junho Kim, Analyst at UBI Research (alertriot@ubiresearch.com)

LightBundle™ — Using microLEDs to “move data” (Source: Avicena)

The performance of an interconnect (Source: Avicena)

Micro LED, which has been attracting attention as a next-generation display technology, is finding commercialization possibilities in new applications. Although its entry into the display market has been delayed due to low yields and complex manufacturing processes, the practicality of Micro LED is drawing attention again as demand for high-speed optical communication (Co-Packaged Optics, CPO) between AI semiconductors has recently increased. The CPO field is a field that matches well with the characteristics of Micro LED, which are small, high-speed, and low-power, and commercialization in this market is likely to act as a turning point that can accelerate its entry into the display market.

Micro LED is a display technology that combines the advantages of OLED and LCD to provide high brightness, long lifespan, no burn-in characteristics, and excellent color reproducibility. However, there are technical, manufacturing, and economic challenges that must be resolved for full-scale market expansion.

Technologically, millions of RGB chips of several μm in size must be precisely arranged and bonded, and the mass transfer process for this still has room for improvement in terms of speed, precision, and yield. In the bonding process, precision control technologies such as thermal stress and alignment errors need to be continuously advanced.

The manufacturing process also requires optimization. Since more than one pixel can affect the overall screen quality, high-precision inspection and advanced correction technologies are essential, and the current yield remains at around 10-30% based on the pilot line. The level of automation and the precision of inspection equipment are also major improvement tasks for securing future productivity.

In terms of economic feasibility, efficiency in yield and process cost structure is required. For example, Samsung Electronics’ 110-inch Micro-LED TV ‘The Wall’ is currently sold at around $150,000, and the material and equipment ecosystem also needs additional expansion to establish a full-scale mass production system.

Currently, Micro-LED is being introduced to the premium market centered on ultra-high-end TVs and large commercial signage, and expansion to various product groups such as AR and IT devices is expected in the future. Process standardization and supply chain establishment are gradually progressing across the industry, and this trend is expected to lead to a practical foundation for market expansion. Although various technology and process-related challenges still exist, they are recognized as step-by-step tasks that can be solved through improvement and evolution. In particular, the expansion of technology application in the non-display field is acting as a positive opportunity to verify the practicality and reliability of Micro-LED. AI servers and high-performance semiconductor systems require a high-speed, low-power optical communication environment, which is exactly aligned with the technical characteristics of Micro-LED. Existing electrical-based interconnects show limitations such as heat generation and bandwidth bottlenecks, and CPO technology, an optical signal-based communication structure, is being rapidly adopted to solve these problems.

Avicena, a US startup, is a leading company pioneering this field, and is implementing high-speed, low-power interconnects suitable for AI and HPC systems through its LightBundle™ solution, an optical communication technology based on Micro-LED. Avicena drives thousands of Micro-LED arrays in parallel to realize transmission speeds of tens to hundreds of Gbps, and demonstrates technological advantages in terms of low heat generation, low operating voltage, miniaturization, and parallelization compared to existing VCSELs. In addition, since it can be manufactured based on a CMOS process, it is also advantageous for integration with semiconductor packages.

Micro-LEDs for optical communication have simpler implementation conditions than those for displays. Since multi-color elements or high resolution are not required and the number of chips is limited to the thousands to tens of thousands, productization is possible even with a somewhat low yield. In fact, some companies including Avicena are entering the AI server market with Micro-LED-based optical communication solutions, and in this market, actual communication performance and long-term reliability are key competitive factors rather than yield.

The expansion of demand in the AI optical communication market is becoming an important catalyst for strengthening the mass production base of Micro-LED. Increased production, equipment investment, and expansion of the material supply chain can also lead to a virtuous cycle of yield improvement, process automation, and cost reduction in the display market. In fact, some equipment companies are developing integrated equipment that can simultaneously handle display and optical communication processes, and this is working as a positive signal for the entire industrial ecosystem.