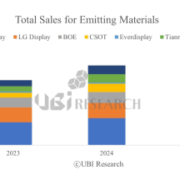

As China’s display industry expands beyond LCD into OLED, Micro-LED, IT, and automotive displays – broadening its presence and influence in the global market – the background behind its growth and its future development direction have been outlined.

On January 23, our publication visited the Beijing office of CODA (China Optics and Optoelectronics Manufactures Association LCB) and met with Xinqing Liang Executive Vice Chairman and Secretary General, Chunming Hu, Executive Vice Secretary General, to discuss the overall state of China’s display industry and the role of CODA. CODA is a national-level industry organization representing the “new-type display” industry, a term that encompasses all flat panel displays developed after CRT, and plays a role spanning industrial policy, technology, markets, and international cooperation.

The CODA office in Beijing, serving as a hub for China’s display industry policy and international cooperation. (Source: CODA)

“China’s Growth: Combined Effects of Objective and Subjective Factors”

Secretary General Liang explained that the current state of China’s new-type display industry is “the result of a combination of objective and subjective factors.” From an objective perspective, he noted that the development of China’s display industry followed the general trend of technology diffusion and industrial value-chain migration observed during the globalization process. From a subjective perspective, Chinese entrepreneurs continuously pursued development strategies centered on investment and innovation, maximizing corporate vitality, which in turn led to the formation of regional industrial clusters and the realization of economies of scale.

“Being No.1 Was Not the Goal, but the Result… The Starting Point Was Resolving the ‘Panel Shortage’”

Liang emphasized that becoming the world’s largest display-producing country was not an initial goal for China’s industry, nor is it a goal in itself going forward. The fundamental reason China began to foster the new-type display industry in earnest was to address the “panel shortage” that emerged during the technological transition from CRT to LCD. After more than 20 years of sustained effort, China not only resolved this issue but also made meaningful contributions to the stable development of the global display industry. As a result, the global new-type display industry has been able to maintain continuous growth.

“In a Reorganization of Globalization, the Next Challenges Are ‘Technology Creation’ and the ‘Supply Chain’”

He pointed out that the global economic structure is currently undergoing a reorganization of globalization, which is also affecting the healthy and sustainable development of the new-type display industry. China’s display industry still has areas that need improvement in terms of technology creation capabilities and the completeness of the supply chain, including core materials and equipment. Strengthening these areas is necessary to secure technological leadership, expand application fields, and build a safer and more efficient industrial ecosystem. He added that China’s future development goal is to play a greater role in elevating the global display industry to a new stage by fostering a sound competitive environment in the global market.

CODA: “Serving Members and Government”… A Bridge for International Exchange Platforms

Regarding CODA’s role, Liang explained that since the establishment of its dedicated secretariat, CODA has consistently adhered to the principle of “serving members and government” as a national-level industry organization. CODA has maintained an approach centered on “product orientation, internationalization, specialization, and market focus,” building various international exchange platforms and serving as a bridge connecting stakeholders inside and outside the industry.

He noted that CODA’s core role has been to comprehensively, timely and profoundly grasp trends and developments across markets, technology, competition, investment, and trade in the new-type display industry. This information has served as important reference material for member companies’ strategic decision-making and for government industrial policy formulation.

“Conditions for Sustainability… Balance across Technology, Market, Competition, Investment, and Trade”

Liang stressed that healthy and sustainable development is a common challenge faced not only by China but by the global new-type display industry as a whole, requiring collective efforts from the global industry. He stated that sound and sustainable development depends on maintaining balance across five dimensions: technology, market, competition, investment, and trade.

From a technological standpoint, China’s industry defines TFT-LCD and AMOLED as the “two mainstream technologies.” Over the next three to five years, TFT-LCD is expected to remain a key technology for absorbing excess capacity and mitigating volatility, while AMOLED will play a central role in reshaping competitive dynamics through technological innovation. He emphasized that new display technologies require repeated and continuous innovation, and that proactive, in-house innovation will determine the industry’s sustainability.

In parallel, China’s industry has identified MLED, microdisplays, e-paper, and laser displays as future-oriented technologies and is promoting industrialization with a five- to ten-year outlook. On the market side, China aims to leverage its large-scale domestic market and infrastructure to expand applications into automotive, industrial control, medical, and public electronics sectors.

From a competition perspective, Liang stressed that fair and orderly competition is inseparable from the industry’s sound and sustainable development, with “fairness, order, openness, and inclusiveness” as core principles. China has already implemented measures to curb redundant investment and disorderly capacity expansion, and plans to further strengthen intellectual property protection while advancing standardization and integration.

From an investment perspective, he explained that China will maintain a “counter-cyclical investment” approach, expanding integrated investments centered on new technologies, new processes, and new materials, while accelerating the commercialization of R&D outcomes. In terms of trade, China emphasizes the global nature of the new-type display industry and intends to expand cooperation with overseas partners.

CODA: “Platform Function”… Addressing Common Challenges and Reflecting Industry Needs

Regarding the role that industry organizations such as CODA can uniquely play in the next stage of China’s display industry, Liang highlighted the importance of the “platform function.” He explained that the core characteristic of such platforms is commonality: resolving common industry problems, recognizing shared challenges, organizing collective experience, clarifying industry trends, and reflecting common demands in policy and the market.

CODA has consistently adhered to the principles of “productization, internationalization, specialization, and marketization,” and believes that recognizing the prosperity of the global industry as its own responsibility is a critical foundation for the healthy and sustainable development of China’s industry.

“Sustained Innovation through Korea–China Cooperation Is Key”… Emphasizing Shared Global Challenges

In closing, Liang delivered a message to global industry stakeholders watching China’s display industry and CODA. He emphasized that the display industry has already formed a massive global market and supplies products that are essential worldwide. The display industry has developed primarily around Northeast Asia, during which China and South Korea have established themselves as the most important production bases. Within this context, it is expected that the roles China and South Korea will play in the global display industry will become even more significant going forward.

He stressed that cooperation between China and Korea – particularly at the corporate level – is critically important going forward. Through cooperation, sustained innovation can be achieved, strengthening industrial competitiveness. Ultimately, he said, joint efforts between the two countries should contribute to making human life more convenient and improving quality of life overall, which he described as a personal vision.

He also referenced his past interactions with LG Display and Samsung, expressing a desire to further expand Korea–China cooperation based on these experiences. At the same time, he acknowledged that China faces challenges such as excess capacity and redundant investment, and emphasized that it is important for both countries to work together to provide high-quality products to the global market, achieve healthy and orderly development, and foster a fair and well-ordered competitive environment.

Changwook Han, Executive Vice President/Analyst at UBI Research (cwhan@ubiresearch.com)

Pre-register for Display Korea 2026

Pre-register for Display Korea 2026

※ This article is produced by UBIResearchNet.

Unauthorized reproduction or citation without source attribution is prohibited.

When quoting, please clearly indicate the source (UBIResearchNet) and provide a link.

China Trends Report Inquiry

China Trends Report Inquiry